This Client Alert provides an update on shareholder activism activity involving NYSE- and Nasdaq-listed companies with equity market capitalizations in excess of $1 billion and below $100 billion (as of the last date of trading in 2021) during 2021.

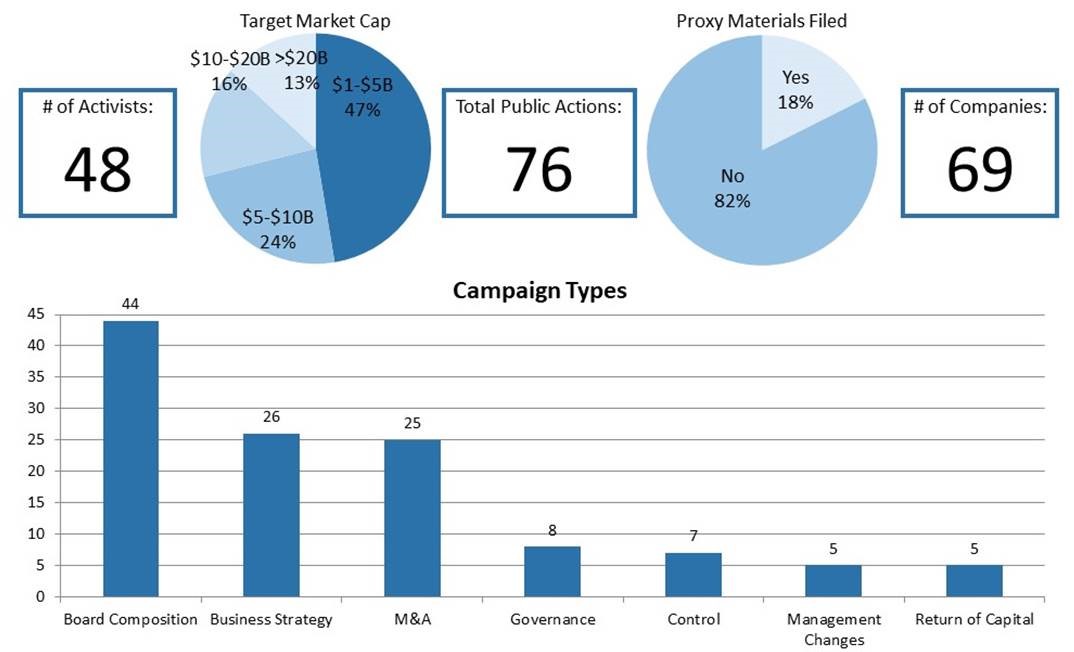

Announced shareholder activist activity increased relative to 2020. The number of public activist actions (76 vs. 63), activist investors taking actions (48 vs. 41), and companies targeted by such actions (69 vs. 55) each increased. Such levels of activism are comparable to those found prior to the market disruption caused by the COVID-19 pandemic, as reflected in public activist actions in 2019 (76 vs. 75), activist investors taking actions (48 vs. 49), and companies targeted by such actions (69 vs. 64). The period spanning January 1, 2021 to December 31, 2021 also saw several campaigns by multiple activists targeting a single company, such as the campaigns involving Kohl’s Corporation that included activity by 4010 Partners, Macellum Advisors, Ancora Advisors and Legion Partners Asset Management; Adtalem Global Education that included activity by Engine Capital and Hawk Ridge Capital; and Bottomline Technologies that included activity by Clearfield Capital Management and Sachem Head Capital Management. In addition, certain activists launched multiple campaigns during 2021, including Carl Icahn, Elliott Investment Management, JANA Partners, Land & Buildings and Starboard Value. Indeed, each of these investors launched four or more campaigns in 2021 and collectively accounted for 20 out of the 76 activist actions reviewed, or 26% in total. Proxy solicitation occurred in 18% of campaigns in 2021, relative to 17% in 2020. These figures represent modest declines relative to 2019, in which proxy materials were filed in approximately 30% of activist campaigns for the entire year.

By the Numbers—2021 Public Activism Trends

*Study covers selected activist campaigns involving NYSE- and Nasdaq-traded companies with equity market capitalizations of greater than $1 billion as of December 31, 2021 (unless company is no longer listed).

Additional statistical analyses may be found in the complete Activism Update linked below.

Notwithstanding the increase in activism levels, the rationales for activist campaigns during 2021 were generally consistent with those undertaken in 2020. Over both periods, board composition and business strategy represented leading rationales animating shareholder activism campaigns, representing 58% of rationales in 2021 and 51% of rationales in 2020. M&A (which includes advocacy for or against spin-offs, acquisitions and sales) remained important as well; the frequency with which M&A animated activist campaigns was 19% in both 2021 and 2020. At the opposite end of the spectrum, management changes, return of capital and control remained the most infrequently cited rationales for activist campaigns, as was also the case in 2020. (Note that the above-referenced percentages total over 100%, as certain activist campaigns had multiple rationales.)

Seventeen settlement agreements pertaining to shareholder activism activity were filed during 2021, which is consistent with pre-pandemic levels of similar activity (22 agreements filed in 2019 and 30 agreements filed in 2018, as compared to eight agreements filed in 2020). Those settlement agreements that were filed had many of the same features noted in prior reviews, including voting agreements and standstill periods as well as non-disparagement covenants and minimum- and/or maximum-share ownership covenants. Expense reimbursement provisions were included in half of those agreements reviewed, which is consistent with historical trends. We delve further into the data and the details in the latter half of this Client Alert.

We hope you find Gibson Dunn’s 2021 Annual Activism Update informative. If you have any questions, please reach out to a member of your Gibson Dunn team.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding the issues discussed in this publication. For further information, please contact the Gibson Dunn lawyer with whom you usually work, or any of the following practice leaders, members, or authors:

Barbara L. Becker (+1 212.351.4062, bbecker@gibsondunn.com)

Dennis J. Friedman (+1 212.351.3900, dfriedman@gibsondunn.com)

Richard J. Birns (+1 212.351.4032, rbirns@gibsondunn.com)

Andrew Kaplan (+1 212.351.4064, akaplan@gibsondunn.com)

Daniel S. Alterbaum (+1 212.351.4084, dalterbaum@gibsondunn.com)

Joey Herman (+1 212.351.2402, jherman@gibsondunn.com)Mergers and Acquisitions Group:

Robert B. Little – Dallas (+1 214-698-3260, rlittle@gibsondunn.com)

Saee Muzumdar – New York (+1 212-351-3966, smuzumdar@gibsondunn.com)Securities Regulation and Corporate Governance Group:

Elizabeth Ising – Washington, D.C. (+1 202.955.8287, eising@gibsondunn.com)

Brian J. Lane – Washington, D.C. (+1 202.887.3646, blane@gibsondunn.com)

James J. Moloney – Orange County, CA (+1 949.451.4343, jmoloney@gibsondunn.com)

Ronald O. Mueller – Washington, D.C. (+1 202.955.8671, rmueller@gibsondunn.com)

Lori Zyskowski – New York (+1 212.351.2309, lzyskowski@gibsondunn.com)© 2022 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.

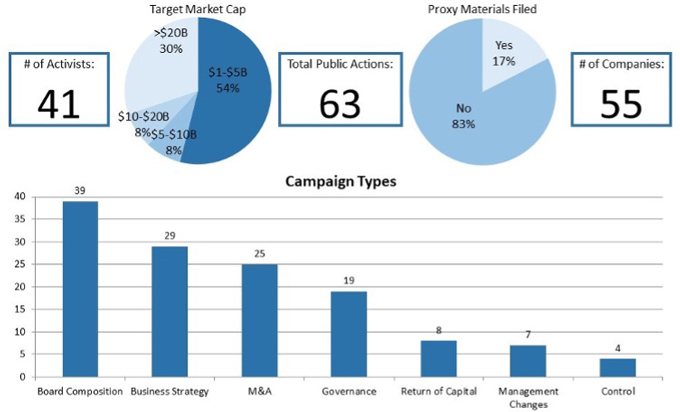

This Client Alert provides an update on shareholder activism activity involving NYSE- and Nasdaq-listed companies with equity market capitalizations in excess of $1 billion and below $100 billion (as of the last date of trading in 2020) during the second half of 2020. Announced shareholder activist activity increased relative to the second half of 2019. The number of public activist actions (35 vs. 24), activist investors taking actions (31 vs. 17) and companies targeted by such actions (33 vs. 23) each increased substantially. On a full-year basis, however, owing to the market disruption caused by the COVID-19 pandemic, 2020 represented a modest slowdown in activism versus 2019, as reflected in the number of public activist actions (63 vs. 75), activist investors taking actions (41 vs. 49) and companies targeted by such actions (55 vs. 64). During the period spanning July 1, 2020 to December 31, 2020, two of the 39 companies targeted by activists—CoreLogic, Inc. and Monmouth Real Estate Investment Corporation—were the subject of multiple campaigns. CoreLogic, Inc. was the subject of an activist campaign led by Cannae Holdings and Senator Investment Group; their efforts, in turn, ultimately drew the support of Pentwater Capital Management LP. In addition, certain activists launched multiple campaigns during the second half of 2020: Elliott Management, NorthStar Asset Management and Starboard Value. These three activists represented 23% of the total public activist actions that began during the second half of 2020.

*Study covers selected activist campaigns involving NYSE- and Nasdaq-traded companies with equity market capitalizations of greater than $1 billion as of December 31, 2020 (unless company is no longer listed).

**All data is derived from the data compiled from the campaigns studied for the 2020 Year-End Activism Update.

Additional statistical analyses may be found in the complete Activism Update linked below.

The rationales for activist campaigns during the second half of 2020 changed in certain respects relative to the first half of 2020. Over both periods, board composition and business strategy represented leading rationales animating shareholder activism campaigns, representing 55% of rationales in the first half of 2020 and 49% of rationales in the second half of 2020. M&A (which includes advocacy for or against spin-offs, acquisitions and sales) took on increased importance; the frequency with which M&A animated activist campaigns rose from 9% in the first half of 2020 to 19% in the second half of 2020. At the opposite end of the spectrum, management changes, return of capital and control remained the most infrequently cited rationale for activist campaigns. (Note that the above-referenced percentages total over 100%, as certain activist campaigns had multiple rationales.) These themes are all broadly consistent with those observed in 2019. Proxy solicitation occurred in 14% of campaigns for the second half of 2020 and for 17% of campaigns in 2020 overall. These figures represent modest declines relative to 2019, in which proxy materials were filed in approximately 30% of activist campaigns for the entire year.

Eight settlement agreements pertaining to shareholder activism activity were filed during the second half of 2020 and only 17 were filed for the entire year, which continues a trend of diminution (relative to 22 agreements filed in 2019 and 30 agreements filed in 2018). Those settlement agreements that were filed had many of the same features noted in prior reviews, however, including voting agreements and standstill periods as well as non-disparagement covenants and minimum and/or maximum share ownership covenants. Expense reimbursement provisions were included in half of those agreements reviewed, which is consistent with historical trends. We delve further into the data and the details in the latter half of this Client Alert. We hope you find Gibson Dunn’s 2020 Year-End Activism Update informative. If you have any questions, please reach out to a member of your Gibson Dunn team.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding the issues discussed in this publication. For further information, please contact the Gibson Dunn lawyer with whom you usually work, or any of the following authors in the firm’s New York office:

Barbara L. Becker (+1 212.351.4062, bbecker@gibsondunn.com)

Dennis J. Friedman (+1 212.351.3900, dfriedman@gibsondunn.com)

Richard J. Birns (+1 212.351.4032, rbirns@gibsondunn.com)

Eduardo Gallardo (+1 212.351.3847, egallardo@gibsondunn.com)

Andrew Kaplan (+1 212.351.4064, akaplan@gibsondunn.com)

Saee Muzumdar (+1 212.351.3966, smuzumdar@gibsondunn.com)

Daniel S. Alterbaum (+1 212.351.4084, dalterbaum@gibsondunn.com)

Lisa Phua (+1 212.351.2327, lphua@gibsondunn.com)

Please also feel free to contact any of the following practice group leaders and members:

Mergers and Acquisitions Group:

Jeffrey A. Chapman – Dallas (+1 214.698.3120, jchapman@gibsondunn.com)

Stephen I. Glover – Washington, D.C. (+1 202.955.8593, siglover@gibsondunn.com)

Jonathan K. Layne – Los Angeles (+1 310.552.8641, jlayne@gibsondunn.com)

Securities Regulation and Corporate Governance Group:

Brian J. Lane – Washington, D.C. (+1 202.887.3646, blane@gibsondunn.com)

Ronald O. Mueller – Washington, D.C. (+1 202.955.8671, rmueller@gibsondunn.com)

James J. Moloney – Orange County, CA (+1 949.451.4343, jmoloney@gibsondunn.com)

Elizabeth Ising – Washington, D.C. (+1 202.955.8287, eising@gibsondunn.com)

Lori Zyskowski – New York (+1 212.351.2309, lzyskowski@gibsondunn.com)

© 2021 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.