July 14, 2015

The first half of 2015 has proved yet another eventful period in securities litigation. Chief among significant developments in the first half of the year is the U.S. Supreme Court’s highly anticipated decision in Omnicare, Inc. v. Laborers District Council Construction Industry Pension Fund, 575 U.S. __, 135 S. Ct. 1318 (2015), concerning the scope of liability under Section 11 for false statements of opinion. As noted below, lower courts have already begun wrestling with the false statement and omission standards of liability for statements of opinion espoused in Omnicare. Courts also continue to grapple with the U.S. Supreme Court’s landmark decisions in Halliburton II and Morrison. Several courts are currently interpreting and applying Halliburton II, including the question of what securities class action defendants must do to demonstrate the absence of price impact at class certification. Its interest in the federal securities laws apparently unabated, practitioners can expect the Supreme Court to issue yet another important ruling on the scope of the federal securities laws and federal court jurisdiction: the Court granted a petition for certiorari in Manning v. Merrill Lynch to resolve a circuit split over the "exclusive jurisdiction" conferred by Section 27 to the federal courts over actions brought to enforce any liability or duty created by the Exchange Act.

The past six months have also yielded significant developments from the Delaware courts, the Delaware legislature, and for derivative actions and shareholder proposal litigation. In a highly anticipated move, Delaware enacted legislation that prohibits fee-shifting provisions and authorizes Delaware forum selection clauses. Additionally, recent decisions in Delaware and the Second Circuit confirm that the business judgment rule protects boards of directors that refuse shareholder demands to bring litigation on behalf of the corporation. But the developments don’t stop there: appraisal actions, protections for independent directors, advancement obligations, and creditor standing are just a few of the important topics explored below. These and other notable developments in shareholder litigation are discussed in our 2015 Mid-Year Securities Litigation Update below.

I. Filing and Settlement Trends

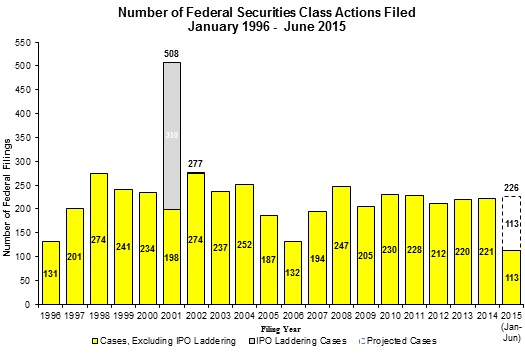

Filing and settlement trends in the first half of 2015 continue to reflect a "steady state" of several hundred cases a year, notwithstanding the virtual disappearance of credit crisis class actions filed in federal court. According to a recent study by NERA Economic Consulting ("NERA"), the rate of new class actions filed in the first half of 2015 annualizes at 226 cases, slightly higher than the five-year average of 222 cases and higher than the number of suits filed annually in the last three years. In most respects, the mix of those cases has not changed significantly from the pattern in 2014. The number of "merger objection" cases filed so far this year represents about 20% of total cases filed in the federal courts, on a pace to meet or exceed last year’s level. However, cases naming financial institutions as the primary defendants are at the lowest level in this decade–only 10% of new cases filed, compared to the high-water mark of 2008, at the onset of the credit crisis, where almost 40% of all new cases named a financial institution as the primary defendant.

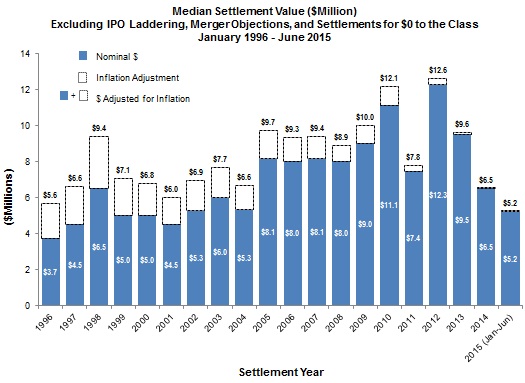

In the first six months of 2015, median settlement values are less than half of the level of just three years ago: $5.2 million in the first half of 2015 versus $12.3 million in 2012. Despite this trend, average settlement amounts increased dramatically in the first six months of 2015, from $34 million in 2014 to $64 million in the first half of 2015, fueled by two very large settlements. That said, the stratification of 2015 settlements reveals that over 60% of those settlements were under $10 million, while roughly 20% were over $50 million.

Finally, median settlement amounts as a percentage of investor losses in the first half of 2015 continue to reflect a pattern that has persisted for decades. Overall, in the last ten years investor losses have never exceeded about 3%. In the first half of 2015, the percentage was only 1.3%.

As discussed in later sections of this Mid-Year Report, the Supreme Court’s decision in Halliburton II may affect filing and settlement trends in the future, but the early returns do not allow any such conclusion. Although Halliburton II allows defendants to defeat class certification by showing that allegedly misleading statements did not cause any "price impact," only a handful of district courts have taken up this issue, and most of those cases have certified the class. Perhaps additional class certification rulings in the next year will establish a discernible trend as to whether the "price impact" test will have a material effect on class action filings or settlements.

A. Class Action Case Filing Trends

Overall filing rates are reflected in Figure 1 below (all charts courtesy of NERA). One hundred thirteen cases were filed in the period January through June 2015, which annualizes to 226 cases for the full year. This figure does not include the many such class suits filed in state courts or the increasing number of state court derivative suits, including many such suits filed in the Delaware Court of Chancery. Those state court cases, however, represent a "force multiplier" of sorts in the dynamics of securities litigation in the United States today.

Figure 1:

B. Mix of Cases Filed in First Half of 2015

1. Merger Cases

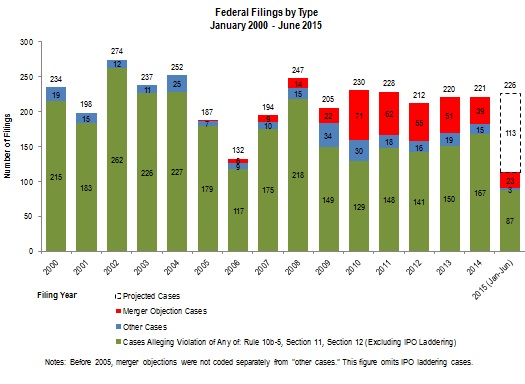

As shown in Figure 2, "merger objection" cases represent a significant percentage of new federal court securities class action filings in 2014 and 2015. NERA reports that in 2014, there were 39 merger-related cases. Twenty-three merger objection cases have been filed so far in 2015, more than half of the 2014 total. As discussed below in our discussion of "Merger & Acquisition and Proxy Disclosure Litigation Trends," the exposure of corporations to M&A litigation spans a range of subject matters, with sometimes unpredictable results. In the state court arena, the Delaware Court of Chancery continues to express deep skepticism about these cases, which are almost invariably filed within days of the announcement of a major M&A transaction.

2. "Credit Crisis" or Other Cases Filed Against Financial Institutions

Continuing the trend from 2014, very few federal court class actions were filed against financial institutions in the first six months of 2015, reflecting the dramatic decline of "credit crisis" class actions since 2008. That said, while credit crisis class actions are on the wane, a new generation of cases have replaced them: single-plaintiff suits by government agencies (such as the Federal Housing Finance Agency on behalf of Fannie Mae and Freddie Mac), monoline insurers (such as MBIA), and institutional and pension fund investors. A few of these single-plaintiff suits have resulted in massive settlements well in excess of $100 million.

Figure 2:

3. Filings By Industry Sector

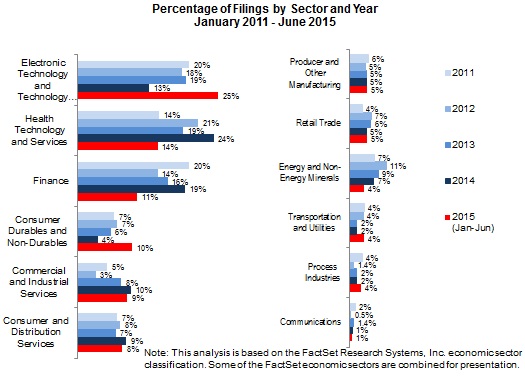

New case filings in 2015 reflect a significant percentage increase in cases against companies in the technology sector, which led the pack at 25% of all new cases filed, compared to 13% in 2014. The healthcare sector came in second with 14% of all cases, while the finance sector placed third with 11% of all new cases. Cases against defendants in the healthcare and finance sectors actually dropped, however, compared to 2014. The biggest jump in new case filings in 2015 on a percentage basis compared to 2014 was in the consumer sector, where new filings more than doubled from their 2014 levels. See Figure 3 below.

Figure 3:

C. Class Action Settlements

As Figure 4 shows, the median settlement amount of $5.2 million in 2015 to date was significantly lower than in 2014, and did represent the lowest level in the last decade. One can speculate about what may account for this downward trend. In any given year, of course, the statistics can mask a number of important factors that contribute to settlement value, such as (i) the amount of D&O insurance; (ii) the presence of parallel proceedings, including government investigations and enforcement actions; (iii) the nature of the events that triggered the suit, such as the announcement of a major restatement; (iv) the range of provable damages in the case; and (v) whether the suit is brought under Section 10(b) of the Exchange Act or Section 11 of the Securities Act.

Figure 4:

A significant driver of the lower median settlement amounts in 2015 year-to-date may be the number of settled cases that were "small" cases to begin with. Whatever the variables, median settlement amounts over the last decade should not necessarily be viewed as a barometer of a long-term decline in settlement values. Back in 2004, the median settlement amount was roughly the same as this year–yet median settlement amounts jumped the next year, from $5.3 million to $8.1 million.

II. Omnicare: U.S. Supreme Court Decides Pivotal Case Regarding False Statements of Opinion Under Section 11

On March 24, 2015, the United States Supreme Court issued its long-awaited decision in Omnicare, Inc. v. Laborers District Council Construction Industry Pension Fund,

575 U.S. __, 135 S. Ct. 1318 (2015). As discussed in our previous client alert on the decision, the Court resolved a circuit split regarding the scope of liability under Section 11 of the Securities Act of 1933 for false statements of opinion. Section 11 provides purchasers of securities a right of action against the issuer and others where the registration statement "contained an untrue statement of material fact" or "omitted to state a material fact . . . necessary to make the statements therein not misleading." 15 U.S.C. § 77k(a). As the Court explained, "Section 11 thus creates two ways to hold issuers liable for the contents of a registration statement–one focusing on what the statement says and the other on what it leaves out." 135 S. Ct. at 1323.

A. The Court’s Opinion

The Supreme Court ultimately addressed two issues: (1) "when an opinion itself constitutes a factual misstatement," and (2) "when an opinion may be rendered misleading by the omission of discrete factual representations." Id. at 1325. With respect to the first issue, the Court held that statements of opinion are not actionable under Section 11 unless the speaker either subjectively believes the opinion to be untrue or the statement of opinion includes a statement regarding an underlying fact that is untrue. Id. at 1326-27. A statement of a genuinely held opinion, regardless of whether it can ultimately be proved wrong, is not necessarily an "untrue statement of material fact" under Section 11. Section 11 is not, as the Court put it, "an invitation to Monday morning quarterback an issuer’s opinions." Id. at 1327.

On the second issue, the Court stated that the inquiry into whether an omission renders a statement misleading is objective and "depends on the perspective of a reasonable investor." Id. While "a statement of opinion is not misleading just because external facts show the opinion to be incorrect . . . a reasonable investor may, depending on the circumstances, understand an opinion statement to convey facts about how the speaker has formed the opinion–or, otherwise put, about the speaker’s basis for holding that view." Id. at 1328. In such a case, the opinion statement could mislead if the "real facts are otherwise, but not provided." Id. The Court explained that this inquiry will depend on the full context in which the opinion statement was made. It also made clear that an investor must plead more than conclusory assertions to adequately state such an omission claim: "The investor must identify particular (and material) facts going to the basis for the issuer’s opinion–facts about the inquiry the issuer did or did not conduct or the knowledge it did or did not have–whose omission makes the opinion statement at issue misleading to a reasonable person reading the statement fairly and in context." Id. at 1332.

B. Post-Omnicare Rulings

While too early to gauge the decision’s full impact on future litigation, lower courts have already begun interpreting the decision and applying its reasoning to claims brought under Section 11 as well as other provisions of the securities laws containing similar language, such as Section 12(a)(2) of the Securities Act of 1933 and SEC Rule 10b-5, promulgated pursuant to Section 10(b) of the Securities Exchange Act of 1934. See, e.g., In re Merck & Co., Inc. Sec., Derivative & "ERISA" Litig., Nos. 05-1141 (SRC), 05-2367 (SRC), 2015 WL 2250472, at *11 n.7 (D.N.J. May 13, 2015) (stating Omnicare was "not directly applicable" to a Section 10(b) claim and its scienter requirement, but still finding the decision’s analysis of allegedly misleading opinions "instructive on the viability of Plaintiffs’ claim"); In re Genworth Fin. Inc. Sec. Litig.,

No. 3:14-CV-682, 2015 WL 2061989, at *15 (E.D. Va. May 1, 2015) ("Omnicare’s holding is applicable and relevant to the instant case as the standard defined in Section 11 of the Securities Act is nearly identical to the [Section 10(b)/Rule 10b-5] standard at issue here.").

For example, in Nakkhumpun v. Taylor, 782 F.3d 1142 (10th Cir. 2015), the Tenth Circuit addressed a Section 10(b) claim concerning statements of opinion made by a company president regarding the company’s financial situation. Id. at 1159-60. Following Omnicare, the Tenth Circuit stated that "[a]n opinion is considered false if the speaker does not actually or reasonably hold that opinion." Id. In affirming the district court’s dismissal of the claim for failure to adequately allege falsity, the court found that the plaintiff had failed to allege "any facts that would cast doubt on the sincerity or reasonableness of [the President’s] statement of his opinion." Id. at 1159. See also In re Amarin Corp. PLC, Sec. Litig., No. 13-CV-6663 (FLW)(TJB), 2015 WL 3954190, at *7 & n.14 (D.N.J. June 26, 2015) (finding plaintiffs failed to sufficiently allege a material omission even assuming, without deciding, that Omnicare applies to a Section 10(b) claim).

Plaintiffs fared better in two recent cases in the United States District Court for the Southern District of New York. In In re BioScrip, Inc. Securities Litigation, No. 13-cv-6922 (AJN), 2015 WL 1501620 (S.D.N.Y. Mar. 31, 2015), plaintiffs alleged that BioScrip had made false and misleading statements about its compliance with the False Claims Act and covered up an investigation into a kickback scheme. In particular, plaintiffs challenged a statement that the company believed itself to be in "substantial compliance with all laws, rules and regulations." The court found that, among other things, the fact that the company had already received a civil investigative demand ("CID") at the time of the alleged misstatement, "allow[ed] for the inference that BioScrip could not have believed the veracity of its legal compliance statements." Id. at *12. Relying on Omnicare, the court found that "[r]egardless of whether BioScrip reasonably believed the CID was a minor issue or not, Plaintiffs adequately alleged that a reasonable investor would feel entitled to an explanation as to how the broad legal compliance statement ‘align[ed] with the information’ in BioScrip’s possession at the time." Id. at *13. The court held that plaintiffs had stated a claim under Sections 11 and 12(a)(2) of the Securities Act and Section 10(b) of the Exchange Act. Id. at *15, 26.

In the second action, the Federal Housing Finance Agency ("FHFA") sued Nomura Holdings Inc. under Sections 12(a)(2) and 15 of the Securities Act of 1933 for alleged misrepresentations in offering documents for residential mortgage-backed securities sold to Fannie Mae and Freddie Mac. FHFA v. Nomura Holding America, Inc., No. 11cv6201 (DLC), 2015 WL 2183875 (S.D.N.Y. May 11, 2015). Following a bench trial, the court ruled in favor of the FHFA and found, among other things, that statements pertaining to the "belief" by the depositor that certain underwriting guidelines for the mortgages were followed implied that defendants knew sufficient facts to justify that opinion. Because the evidence showed that defendants were aware of information contradicting their representations, the court found that the FHFA had established defendants’ misstatement liability as they "lacked the basis for making those statements that a reasonable investor would expect." Id. at *103 (quoting Omnicare, 135 S. Ct. at 1333). The court also found that the FHFA had established that statements concerning appraisal values and loan-to-value ratios were false, because they were subjectively disbelieved. Id. at *104.

III. Class Actions Post-Halliburton II: Early Returns on Whether the Supreme Court’s "Price Impact" Test for Class Certification Is Making a Difference

The federal appellate and district courts continue to wade through issues left open by the Supreme Court’s landmark decision in Halliburton Co. v. Erica P. John Fund, Inc., 134 S. Ct. 2398 (2014) ("Halliburton II"). Principal among these issues is the question of what securities class action defendants must do to demonstrate the absence of price impact (and thereby rebut the fraud-on-the-market presumption) at class certification. The courts continue to grapple with several aspects of the price impact analysis, including whether defendants may show lack of impact by focusing solely on the stock price movement at the time of the alleged misrepresentation and the role that price declines following an alleged corrective disclosure should have in the price impact analysis, if any. The U.S. District Court for the Northern District of Texas’s impending ruling on class certification on remand from Halliburton II is expected to be an important early decision that may influence how other courts approach this critical class certification-stage issue. The district court entertained arguments on the issue in December 2014 but has yet to rule. Minute Entry, Erica P. John Fund, Inc. v. Halliburton Co., No. 02-cv-1152-M (N.D. Tex. Dec. 1, 2014). All deadlines in the action have been stayed pending the district court’s much-anticipated class certification decision, which we expect will issue before year’s end. Order, Erica P. John Fund, Inc. v. Halliburton Co., No. 02-cv-1152-M (N.D. Tex. April 14, 2015).

Of course, as reported in our year-end report, the Eleventh Circuit has already weighed in. In remanding a class certification decision to the lower court, the court stated that the district court’s task on remand would "be limited in scope" as Halliburton II "only said that defendants ‘may seek to defeat the Basic presumption’ with evidence that the misrepresentations did not impact the price. Halliburton II by no means holds that in every case in which such evidence is presented, the presumption will always be defeated." Local 703, I.B. of T. Grocery & Food Emps. Welfare Fund v. Regions Fin. Corp., 762 F.3d 1248, 1259 (11th Cir. 2014) (emphasis in original) (internal citation omitted). On remand, the district court still certified the class. Local 703, I.B. of T. Grocery & Food Emps. Welfare Fund v. Regions Fin. Corp., No. 10-cv-2847-IPJ, 2014 WL 6661918 (N.D. Ala. Nov. 19, 2014).

The Eighth Circuit is now set to weigh in and issue a ruling addressing the contours of the price impact inquiry at class certification under Halliburton II in the coming months in the interlocutory appeal from IBEW Local 98 Pension Fund v. Best Buy Co., No. 11-cv-429-DWF, 2014 WL 4746195 (D. Minn. Aug. 6, 2014), discussed in our year-end Client Alert. In Best Buy, the Eighth Circuit has been asked to resolve, among other things: (1) whether the district court improperly conflated price impact with loss causation when it considered evidence of back-end price reaction following a disclosure that plaintiffs argued was "corrective," as well as (2) whether the district court misapplied Halliburton II by failing to place the ultimate burden of persuasion on the issue of reliance on the plaintiffs after defendants rebutted the presumption. See Brief of Defendants-Appellants, IBEW Local 98 Pension Fund v. Best Buy Co., No. 14-3178 (8th Cir. Dec. 4, 2014). Both the Securities Industry and Financial Markets Association and the Chamber of Commerce for the United States of America filed amicus briefs in support of the defendants-appellants. Amicus Brief, IBEW Local 98 Pension Fund v. Best Buy Co., No. 14-3178 (8th Cir. Dec. 11, 2014); Amicus Brief, IBEW Local 98 Pension Fund v. Best Buy Co., No. 14-3178 (8th Cir. Dec. 12, 2014). The Eighth Circuit is likely to hold oral argument in fall 2015.

Halliburton and Best Buy are expected to provide helpful, if still preliminary, insight into both the manner in which district courts should apply Halliburton II‘s mandate and the tools defendants should employ to exercise their right to rebut the fraud on the market presumption at class certification with evidence of lack of price impact.

Also still pending is the merits-level appeal of the Southern District of New York’s nearly $50 million jury verdict against the defendant in In re Vivendi Universal, S.A. Securities Litigation, No. 02-cv-5571-SAS (S.D.N.Y. Dec. 22, 2014). Among other issues, the Second Circuit has been asked to examine the methodology of plaintiff’s expert in demonstrating loss causation at trial–an inquiry which is likely to illuminate the parameters of plaintiff’s burden to prove price impact for purposes of establishing loss causation at the merits stage of litigation. See Principal Brief for Vivendi, In re Vivendi Universal, S.A. Securities Litigation, No. 15-180 (2d Cir. Feb. 20, 2015). Oral argument is likely to occur in late fall or early winter 2015.

IV. U.S. Supreme Court to Decide Circuit Split Over Whether Federal Courts Have Jurisdiction Over State Law Claims Related to "Naked" Short Sales and Other Suits Brought in State Court

In continuing what has become a trend of taking up important securities law issues, the Supreme Court announced on June 30 that it will consider an appeal from several financial institutions relating to shareholders’ claims that these entities engaged in illegal "naked" short selling. Shareholders of Escala Group Inc. sued several financial institutions in New Jersey state court in 2012, claiming that they engaged in short selling of shares of Escala that they did not own or borrow, or ever intend to own or borrow. Plaintiffs allege that the practice artificially lowered the shares’ value, enabling defendants to repurchase shares at a lower price for return to the lender and to profit on the difference. The shareholders asserted claims under New Jersey’s Racketeer Influenced and Corrupt Organizations Act and Uniform Securities Law.

Defendants removed the case to federal court, and plaintiffs challenged the change of jurisdiction. Defendants argued that Regulation SHO, the SEC’s rule on short sales, and Section 27 of the Securities Exchange Act, provided a basis for federal court jurisdiction. Their motion was denied and then appealed to the Third Circuit. Manning v. Merrill Lynch, 772 F.3d 158 (3d Cir. 2014). The Third Circuit held that none of the causes of action pleaded in the amended complaint were predicated on a violation of Regulation SHO, and that even if the claims had been partially predicated on Regulation SHO, federal law would still not necessarily be implicated. The court reasoned that the question of whether the naked short-selling at issue violated state law could be answered without reference to Regulation SHO. The court explained that "[w]here plaintiffs’ state-law RICO claims allege both federal and state predicate acts, no federal question is necessarily raised because a plaintiff could prevail upon their New Jersey RICO claims or any of their other state-law claims without any need to prove or establish a violation of federal law." Id. at 164.

The defendants petitioned the Supreme Court for certiorari, arguing that the case is the "ideal vehicle" for resolving a split over the proper interpretation of Section 27. Petition for Writ of Certiorari, Merrill Lynch, et al. v. Manning, 2015 WL 1223714 (2015) (No. 14-1132). Section 27 holds that federal courts "shall have exclusive jurisdiction of violations" of the law and "of all suits in equity and actions at law brought to enforce any liability or duty created by" it. The Fifth and Ninth Circuits have held that Section 27 confers federal jurisdiction over state-law claims seeking to establish liability or enforce duties created by the Exchange Act or its regulations, while the Second Circuit, now joined by the Third Circuit, has held that it does not. In their petition for certiorari, the defendants argued that, were the Second and Third Circuits’ interpretation to stand, "the standards and duties prescribed by Regulation SHO" would be "subject to interpretation by a state-court judge, enforce[d] by a state-court jury, and review[ed] by a state court of appeals formally bound only by state-court precedents on Regulation SHO (of which there are none of course)." Id. at *3. Defendants argue that any such result contravenes Section 27’s essential objective, "effectively empowering fifty-one different state-court systems to enforce the act’s standards and duties." Id. The Supreme Court will now decide the issue.

V. SLUSA After Troice: The Second Circuit Further Limits the Scope of SLUSA Preemption of State Law Claims

In our February 28, 2014 alert, we discussed the Supreme Court’s decision in Chadbourne & Parke LLP v. Troice, 134 S. Ct. 1058 (2014), which clarified the standard for the application of the Securities Litigation Uniform Securities Act ("SLUSA"). SLUSA bars state law claims based on "a misrepresentation or omission of a material fact in connection with the purchase or sale of a covered security." 15 U.S.C. § 78bb(f)(1) (emphasis added). In Troice, the Court held that the phrase "in connection with" required that the misrepresentation or omission must be "material to a decision by one or more individuals (other than the fraudster) to buy or sell a ‘covered security.’" 134 S. Ct. at 1066. While Troice has yet to be broadly applied by lower federal courts, the Second Circuit recently narrowed the scope of SLUSA preemption even further.

In In re Kingate Management Limited Litigation, the Second Circuit considered a challenge to state law class action claims brought by investors in offshore feeder funds that allegedly were part of the Madoff Ponzi scheme. 784 F.3d 128 (2d Cir. 2015). The defendants moved to dismiss on the ground that the investors’ claims–a variety of state law claims–were precluded by SLUSA, and the district court granted the motion. The Second Circuit noted several ambiguities relating to the scope of SLUSA’s prohibitions, including the relationship of the alleged false conduct to the state law theory of liability and the relationship of the defendant to the alleged false conduct. Id. at 132. Significantly, the court applied a "necessary component" test for preemption, which "requires courts to inquire whether the allegation [of misrepresentation or omission] is necessary to or extraneous to liability under the state laws." The Second Circuit concluded that "state law claims that do not depend on the false conduct are not within the scope of SLUSA," even if the complaint includes peripheral, inessential mentions of false conduct. Id. The court further decided that plaintiffs must allege the defendant’s complicity in the false conduct giving rise to liability in order for the claim to be precluded by SLUSA. Id. Accordingly, because the district court did not consider whether the state law claims depended on false conduct committed by the defendants, the Second Circuit vacated the district court’s dismissal of the plaintiffs’ claims. Id. at 150.

VI. Restricting Extraterritorial Suits: Third Circuit Narrows Morrison’s First Prong

In 2010, the Supreme Court held that the anti-fraud provisions of the Exchange Act have no extraterritorial reach. Morrison v. National Australia Bank Ltd., 561 U.S. 247 (2010). Rather, Section 10(b) could only apply to transactions in securities listed on domestic exchanges (prong one), and "domestic" transactions in other securities (prong two). Id. at 249. The Morrison court used the term "domestic exchanges" interchangeably with the terms "national securities exchanges" and "American stock exchange." Id. at 266-67, 273. Since Morrison, courts have mainly focused on the test’s second prong, grappling with the question of what constitutes a "domestic" transaction such that U.S. securities laws would apply to transactions involving extraterritorial elements.

In United States v. Georgiou, 777 F.3d 125 (3d Cir. 2015), the Third Circuit further clarified Morrison‘s first prong. Id. at 134-37. The defendant was convicted of securities fraud for his participation in the manipulation of four publicly traded stocks from 2004 through 2008. Id. at 130-31. During this period, all four stocks were quoted on and traded through the over-the-counter Bulletin Board (OTCBB) and Pink Sheets markets, and were issued by U.S. companies. Id. at 130, 135. The defendant and his co-conspirators opened brokerage accounts in several foreign countries and traded the relevant stocks between their various accounts, creating the false impression that there was an active market for these stocks and artificially inflating the stocks’ prices. Id. at 130-31. At least some of these manipulative trades were transacted through market makers located in the United States, and defendant occasionally met with his co-conspirators in the United States to discuss these schemes. Id. at 131. The defendant profited from selling shares at these artificially inflated prices and using them as collateral to borrow millions of dollars. Id.

The Third Circuit held that the defendant’s transactions were not covered under the first prong of the Morrison test because OTCBB and the Pink Sheets markets did not qualify as "national securities exchange[s]." Id. at 134. But see United States v. Isaacson, 752 F.3d 1291, 1299 (11th Cir. 2014) (securities traded on the OTCBB or Pink Sheets meet Morrison‘s requirement for a U.S. nexus). The court reasoned that the SEC recognized only eighteen national securities exchanges, and the OTCBB and the Pink Sheets were not among them. Georgiou, 777 F.3d at 134. Further, the court noted that the stated purpose of the Exchange Act referred to "securities exchanges" and "over-the-counter markets" separately, suggesting that they are different from one another. Id. at 134-35. Therefore, in the Third Circuit, U.S. securities laws only apply to securities listed on specified "national securities exchanges," not on any domestic exchange. See id.

Although the defendant survived Morrison‘s first prong, the court held that he was subject to U.S. securities laws because he engaged in "domestic" transactions in other securities. Id. at 135-37. The transactions in this case were domestic, unlike those in Morrison, because "(1) the transactions in this case involve[d] stocks of U.S. companies, (2) that were executed through American market makers." Id. at 135. Consistent with the Absolute Activist reasoning, the court reasoned that the defendant incurred irrevocable liability in the United States when he committed to buying or selling securities in the United States through U.S. market makers. Id. at 136-37; see Absolute Activist Value Master Fund Ltd. v. Ficeto, 677 F.3d 60, 69 (2d Cir. 2012) ("[A] securities transaction is domestic when the parties incur irrevocable liability to carry out the transaction within the United States or when title is passed within the United States."). The court held that the "purchases and sales of securities issued by U.S. companies through U.S. market makers acting as intermediaries for foreign entities constitute ‘domestic transactions’ under Morrison." Georgiou, 777 F.3d at 130.

VII. A Busy First Half of 2015 for Delaware and Derivative Litigation

The year 2015 has already been an eventful one for Delaware courts, the state legislature, and derivative litigation generally. While some important legal developments have strengthened the defenses corporations and their directors have to breach of fiduciary duty claims, others have eroded them. On the one hand, courts reaffirmed the deference due to boards that reject shareholder demand letters and bolstered the protection provided by exculpatory charter provisions. On the other hand, the Delaware Court of Chancery held that compensation awards granted to directors can be subject to searching "entire fairness" review even if they are granted under a compensation plan that has been approved by the company’s stockholders. Further evidencing a pro-investor tilt in Delaware, the state legislature has enacted legislation forbidding stock corporations from adopting bylaw provisions designed to shift litigation expenses (including attorneys’ fees) to the non-prevailing party in certain types of shareholder suits.

The first half of this year has also seen several significant rulings concerning the standing of creditors to pursue derivative claims; director and officer advancement rights; and the ability to settle shareholder derivative claims by paying a special dividend to shareholders. As well, Delaware corporations are experiencing a new wave of shareholder "inspection demands" over so-called "dead hand proxy puts." Finally, yet another important ruling concerning secondary liability for breach of fiduciary duty is expected in the months to come.

A. Amendments to DGCL Endorse Exclusive Forum Clauses and Prohibit Fee-Shifting Provisions

In a highly anticipated move, Delaware Governor Jack Markell signed a bill on June 24, 2015 containing several important amendments to the General Corporation Law of the State of Delaware (the "DGCL"). Among other things, the legislation prohibits fee-shifting provisions and authorizes Delaware forum selection clauses. These changes to the DGCL will become effective on August 1, 2015.

Under the anti-fee-shifting provisions, Delaware stock corporations are prohibited from adopting bylaws that force shareholders to pay legal fees if they do not prevail in lawsuits asserting internal corporate claims against the corporation. Del. Code tit. 8, § 102(f). The legislation creates a new Section 115 in the DGCL, which defines "internal corporate claims" as claims "(i) that are based upon a violation of a duty by a current or former director or officer or stockholder in such capacity, or (ii) as to which the title confers jurisdiction upon the Court of Chancery." This provision had been hotly debated since May 2014, when the Supreme Court of Delaware held in ATP Tour, Inc. v. Deutcher Tennis Bund that "fee-shifting provisions in a non-stock corporation’s bylaws can be valid and enforceable under Delaware law." 91 A.3d 554, 555 (Del. 2014). Since this provision only applies to Delaware stock corporations, it does not invalidate the ATP Tour decision.

The new law also permits Delaware corporations to designate Delaware, but not any other state, as the exclusive forum for internal corporate claims. Provisions of the certificate of incorporation or bylaws that select a forum other than Delaware for intra-corporate claims are not expressly authorized under the new law, but neither are they prohibited. The law does, however, invalidate any such provision selecting courts outside of Delaware, or any arbitral forum, to the extent that the bylaw would prohibit litigation of intra-corporate claims in Delaware courts. As a result, the legislation impacts two recent Delaware Court of Chancery decisions. It affirms the Chancery Court’s decision in Boilermakers Local 154 Retirement Fund v. Chevron Corp., 73 A.3d 934 (Del. Ch. 2013), which upheld the statutory and contractual validity of bylaws selecting Delaware as the exclusive forum for intra-corporate disputes. At the same time, the new law invalidates the Court of Chancery’s decision in City of Providence v. First Citizens BancShares, Inc., which upheld a bylaw that designated an exclusive forum other than Delaware for intra-corporate disputes. 99 A.3d 229, 234 (Del. Ch. 2014).

For more information on the impact of the legislative changes, please read our Client Alert.

B. Confirmation that the Business Judgment Rule Protects Director Decisions to Reject Shareholder Demands to Investigate and Sue the Company’s Own Directors and Officers

During the first six months of the year, both the Delaware Court of Chancery and the Second Circuit have forcefully reaffirmed the deference due to boards of directors that refuse shareholder demands after becoming adequately informed and considering the relevant facts.

1. The DuPont Case

On May 8, the Delaware Court of Chancery reaffirmed that the business judgment rule is the standard of review applicable to a board’s decision to refuse a stockholder demand to bring litigation on behalf of the corporation. In Ironworkers District Council of Philadelphia & Vicinity Retirement & Pension Plan v. Andreotti, C.A. No. 9714-VCG (Del. Ch. May 8, 2015), the court granted a motion to dismiss a stockholder complaint alleging that the board of DuPont wrongfully refused a stockholder demand to sue certain DuPont officers and directors for breaches of fiduciary duties related to the company’s dispute with Monsanto. In 2009, Monsanto sued DuPont in federal district court alleging breach of a licensing agreement and patent infringement claims. In 2012, a jury found in favor of Monsanto, awarding damages in the amount of $1.2 billion and also awarding attorneys’ fees as part of a sanctions order against DuPont. The parties settled in 2013, with DuPont agreeing to pay Monsanto $1.75 billion over ten years.

Following the litigation, DuPont stockholders made demands on DuPont’s board of directors to bring suit against several officers and directors for alleged breaches of fiduciary duties related to the Monsanto lawsuit. In response, the board formed a special committee, comprised of directors who had joined the board after the relevant timeframe at issue. The committee retained outside counsel, conducted a nine-month-long investigation (as set forth in a 179-page report), and ultimately recommended to the board that the demands be rejected because a suit against officers and directors was not in the best interest of DuPont. The full board adopted the committee’s recommendation. The plaintiffs filed suit, claiming that the board wrongfully refused the demands.

The Delaware Court of Chancery dismissed the case, deferring to the board’s decision. The court emphasized that by choosing to make a demand on the board to bring the claims, a plaintiff "tacitly concedes the independence of a majority of the board to respond," the effect of which is that the "demand is treated as any other disinterested and independent decision of the board–it is subject to the business judgment rule." Id. at *66. Thus, the court explained that to survive a motion to dismiss, a stockholder claiming wrongful refusal of a demand has two pleading burdens: "[f]irst, she must allege facts which, if true, are sufficient to state a claim against the defendants"; and second, "she must allege with particularity facts that raise a reasonable doubt that in refusing the demand the directors complied with their fiduciary duties." Id. at *72. In turn, to raise a reasonable doubt that the directors upheld their duties in refusing a demand, the plaintiff must plead "particularized facts that reasonably imply" either (1) "gross negligence, in that the board acted in an uni[n]formed manner by failing either to investigate the demand at all or in pursuing such an inadequate investigation, in light of the seriousness of the demand, that a court may reasonably infer a breach of the duty of care"; or (2) "despite the facial independence of the board, [its decision was] so inexplicable that a court may reasonably infer that the directors must have been acting for a purpose unaligned with the best interest of the corporation; that is, in bad faith." Id.

2. The "London Whale" Case

In another recent "wrongful refusal" case, the Second Circuit affirmed the dismissal of claims against the board of JPMorgan Chase & Co. ("JPMorgan") regarding the "London Whale" trading losses in 2012. See Espinoza v. Dimon, No. 14-1745, 2015 WL 3684972 (2d Cir. June 16, 2015). Lead plaintiff Espinoza served JPMorgan’s board of directors with a pre-suit demand letter requesting that the Board investigate and take action based on two related aspects of the London Whale trades: (1) the underlying trading losses, and (2) the alleged dissemination of misleading statements by JPMorgan CEO Dimon and others. Id. at *6. Espinoza conceded that the board adequately investigated the underlying trading losses but argued that the duly-appointed Review Committee failed to adequately investigate certain public statements that plaintiffs alleged served to understate the scale of the London Whale losses. Id. Applying an abuse of discretion standard of review, the Second Circuit disagreed. Writing for the appellate panel, Chief Judge Katzmann explained that "[i]n light of the ‘presumption that in making a business decision the directors of a corporation acted on an informed basis, in good faith and in the honest belief that the action taken was in the best interests of the company,’ the district court could reasonably conclude that the Board’s decision to focus on the crux of Espinoza’s demand–even at the expense of covering every topic raised in the demand letter–did not rise to the level of gross negligence." Id. at *8.

Although affirming the district court’s order of dismissal, the panel opinion questioned the continuing vitality of the Second Circuit’s otherwise controlling precedents applying the abuse-of-discretion standard in connection with appeals of judgments dismissing derivative complaints. The panel opinion observed that "the time is at hand for the abuse-of discretion standard to be retired, and for us to apply the same de novo standard to the Rule 23.1 context that we apply when reviewing all other dismissals." Id. at *5. The opinion recommended that the Second Circuit follow the approach of the Delaware Supreme Court and the First and Seventh Circuits, which have adopted de novo review of dismissals of derivative actions. Id. at *4. Following the panel’s comments, on June 30, 2015 plaintiffs-appellants filed their petition for rehearing en banc. As of the date of this Mid-Year Report, the Second Circuit had yet to rule on whether to accept plaintiffs’ petition for rehearing.

3. The Orbitz Case

On July 13, 2015, Chancellor Bouchard granted a motion to dismiss a complaint filed by an Orbitz Worldwide, Inc. ("Orbitz") stockholder in the Delaware Court of Chancery challenging the fairness of the terms of a five-year services agreement Orbitz entered into with Travelport Limited ("Travelport"). Order, Teamsters Union 25 Health Services & Insurance Plan v. Orbitz Worldwide, Inc., C.A. No. 9503-CB (Del. Ch. July 13, 2015). The plaintiff claimed that Travelport (which the plaintiff asserted controlled Orbitz through its 48% share ownership) breached its fiduciary duty as a controlling stockholder and that Orbitz’s directors breached their fiduciary duties by approving the agreement. The plaintiff also asserted related derivative claims for unjust enrichment and aiding and abetting.

The defendants moved to dismiss the plaintiff’s claims for failure to make a demand or to adequately plead demand is excused, and the court granted the motion. The court held that, as the plaintiff did not make a demand on Orbitz’s board before initiating the derivative action, the plaintiff was required to "allege with particularity that its failure to make such a demand should be excused." Id. at *19. Additionally, the plaintiff was required to "plead facts specific to each director, demonstrating that at least half of them could not have exercised disinterested business judgment in responding to a demand." Id. at *23. The court held: (1) that the plaintiff did not raise a reasonable doubt as to the impartiality of a majority of the demand board; (2) that the plaintiff did not raise a reasonable doubt that the agreement was approved in bad faith; and (3) that the demand should not be excused simply because the challenged transaction involved an alleged controlling stockholder. Id. at *24-36. As a result, the court concluded that the plaintiff failed to raise a reasonable doubt "as to the ability of a majority of the Demand Board to have impartially considered a demand" relating to the plaintiff’s claims, and granted the motion to dismiss. Id. at *42.

C. Delaware Chancery Court Examines MLP Conflicts Committee Requirements to Act in Subjective Good Faith

On April 20, 2015, in In re El Paso Pipeline Partners, L.P., Vice Chancellor Laster offered important insight into what it means to act in subjective good faith under Delaware law. C.A. No. 7141-VCL (Del. Ch. June 12, 2014). While this case is most relevant in the alternate entity context, specifically master limited partnerships ("MLP") where fiduciary duties may be waived, the court identified the overlap between a contractual obligation to act in good faith and the concept of good faith that arises in the fiduciary context. More broadly, the case is a reminder of the close attention Delaware courts will pay to "process" issues in transactions and potential financial advisor conflicts.

The case arose from a series of "dropdown" transactions through which El Paso Pipeline Partners, L.P. ("El Paso MLP"), purchased certain assets from its controlling sponsor, El Paso Corporation ("Parent"). Because dropdowns will typically be controlling party transactions subject to strict judicial review, El Paso MLP’s limited partnership agreement contained provisions that eliminated "all common law duties that the General Partner and [its board] might otherwise owe to El Paso MLP and its limited partners, including fiduciary duties." In lieu of fiduciary duties, El Paso MLP’s partnership agreement established certain contractual requirements applicable to various transactions. Controlling party transactions such as dropdowns were to be approved by one of four methods, including approval by the members of a "Conflicts Committee," to be composed solely of independent members of the board, "acting in good faith." Id. at *2.

Originally, plaintiffs challenged two of these dropdown transactions–the "Spring Dropdown" and the "Fall Dropdown." The court granted defendants’ motion for summary judgment as to the Spring Dropdown but partially denied their motion for summary judgment as to the Fall Dropdown. The court found questions of fact remained as to whether the members of the Conflicts Committee abided by their contractual duties of good faith in connection with the Fall Dropdown. After trial, despite testimony to the contrary, the court determined that the Conflicts Committee could not make such a showing. Id. at *3.

The Chancery Court found that the Conflicts Committee failed to comply with its obligation to act in good faith when it approved a transaction without first determining it to be in the best interest of the MLP. Specifically, the court found that the members of the committee "failed to form a subjective belief that the Fall Dropdown was in the best interests of El Paso MLP." Id. The court focused on the Conflicts Committee’s failure to engage in any meaningful negotiations, disregard of their "independent and well-considered views about value," fixation solely on accretion in valuing the transaction, failure to consider information in their possession that would affect the transaction’s price, and reliance on reports from their advisor notwithstanding what the court deemed to be obvious flaws in the advisor’s methodology. Id. at *46. While none of these deficiencies standing alone would have shown a lack of subjective good faith, when considered in totality, the court concluded that they tipped the balance toward a finding that the committee did not believe that the transaction was in the best interest of the MLP.

For more information on the important takeaways from the El Paso decision, please read our Client Alert.

D. Delaware Chancery Court Clarifies Director and Officer

Advancement Rights

On May 28, 2015, in Blankenship v. Alpha Appalachia Holdings, Inc., Chancellor Bouchard of the Delaware Court of Chancery issued an opinion clarifying and strengthening the rights of a former director and officer to receive mandatory advancement under a corporation’s charter. C.A. No. 10610-CB (Del. Ch. May 28, 2015). This decision reaffirms the strong protection of director and officer indemnification and advancement rights under Delaware law, "which supports resolving ambiguity in favor of indemnification and advancement." Id. at *41.

The Blankenship case concerned the right to indemnification and advancement by Donald Blankenship, the former CEO and Chairman of Massey Energy Company ("Massey"), a coal mining business. In April 2010, 29 miners were killed in an explosion at one of Massey’s mines. In 2011, after Mr. Blankenship retired, Massey entered into a merger agreement with Alpha Natural Resources, Inc. ("Alpha"). After the merger, Massey sent a letter to Mr. Blankenship stating that Massey remained committed to providing "appropriate assistance with the legal defense" of its employees in connection with investigations into the 2010 explosion, and requesting that he sign a new undertaking (the "Undertaking") that would clarify the relationship. The Undertaking stated that Massey’s advancement of expenses to Mr. Blankenship was contingent upon him making certain representations, including a representation that he "had no reasonable cause to believe that his conduct was ever unlawful." Id. at 3.

Alpha’s acquisition of Massey was completed in June 2011. Mr. Blankenship incurred legal expenses arising out of the government’s investigation of the 2010 mine explosion, which Massey paid. The investigation led to a 2014 criminal indictment against Mr. Blankenship. After the indictment, Massey and Alpha determined that Mr. Blankenship had breached his representation in the Undertaking and ceased advancing the costs of his defense.

The Court of Chancery held that, while the Undertaking required Mr. Blankenship to make certain factual representations before advancement could begin, it could not provide a basis for Massey to terminate its obligations to advance his legal costs. Massey’s charter required it to advance costs to the maximum extent provided by Delaware law. The Court of Chancery noted that when a Delaware corporation adopts charter provisions requiring broad, mandatory advancement, it cannot condition its advancement obligation on anything other than an undertaking to repay the expenses if it is later determined that indemnification is not available because an individual has not met the Delaware law standard of conduct. The representations in the Undertaking, such as Mr. Blankenship’s good faith and reasonable belief that his conduct was not unlawful, merely served to provide reassurance to Massey before it commenced advancing funds. Those representations could not serve as a justification for terminating advancement while Mr. Blankenship was in the middle of his defense.

E. Delaware Supreme Court Affirms That Corporate Directors May Be Protected Against Claims for Money Damages under "Exculpation"

Provisions Adopted by the Corporation

On May 14, 2015, in In re Cornerstone Therapeutics Inc. Stockholder Litigation, the Delaware Supreme Court issued important guidance regarding the pleading requirements to overcome an exculpatory charter provision, such as those authorized under Section 102(b)(7) of the Delaware General Corporation Law. Nos. 564, 2014 & 706, 2014 (Del. May 14, 2015). The court held that in order for a plaintiff to survive a motion to dismiss in a claim for monetary damages against a director protected by an exculpatory charter provision, the plaintiff must plead duty of loyalty/bad faith claims regardless of the underlying standard of review for the board’s conduct–be it Revlon, Unocal, the entire fairness standard, or the business judgment rule. Id. at *1. The Delaware Supreme Court thus reinforced that independent directors of Delaware corporations with standard exculpation provisions should be protected from litigation exposure when they pursue "potentially value-maximizing business decisions." Id. at *15.

As noted in our Client Alert, Section 102(b)(7) authorizes stockholders of a Delaware corporation to adopt a charter provision exculpating directors from paying monetary damages that are attributable solely to a violation of the duty of care (as opposed to violations of the duty of loyalty and/or acts of bad faith). However, based on the Delaware Supreme Court’s decision in Emerald Partners v. Berlin, 787 A.2d 85 (Del. 2001), some Court of Chancery decisions had declined to apply the exculpation clause with respect to independent directors at the pleadings stage in transactions involving interested directors, including controlling stockholders, where the standard of review for such transactions is entire fairness.

In Cornerstone, an opinion authored by Chief Justice Strine, the Supreme Court reversed two recent Court of Chancery rulings that had declined to apply the exculpatory provision at the pleadings phase, holding that "[w]hen the independent directors are protected by an exculpatory charter provision and the plaintiffs are unable to plead a non-exculpated claim against them, those directors are entitled to have the claims against them dismissed." Id. at *2. Specifically, if a director is protected by an exculpatory charter provision, such as Section 102(b)(7) of the Delaware General Corporation Law, in order to survive a motion to dismiss a plaintiff must plead facts "supporting a rational inference that the director harbored self-interest adverse to the stockholders’ interest, acted to advance the self-interest of an interested party from whom [the director] could not be presumed to act independently, or acted in bad faith." Id. at *8.

The Supreme Court’s holding has important implications for directors of Delaware corporations. First, the Supreme Court emphasized that independent directors are entitled to the presumption that they are motivated to do their duty with fidelity and thus are not assumed to be disloyal. Id. at *12-13. Second, under the decision, independent directors are entitled to the full protections of an exculpatory clause adopted by a corporation pursuant to Section 102(b)(7). Id. at *15-16. Accordingly, exculpated independent directors approving a transaction involving a controlling stockholder have a potent weapon in defending against shareholder lawsuits.

F. Delaware Chancery Court Sends Mixed Signals on Determining

a Fair Price in Appraisal Actions

Stockholder appraisal litigation continued at a robust pace in the first half of 2015, with the Chancery Court issuing a number of decisions that provide guidance for future appraisal actions, where the sole question concerns the "fair value" of a stockholder’s shares following a corporate sale. In several recent decisions, the Chancery Court has concluded that the "fair value" for the appraisal shares is the transaction price per share–dealing significant blows to appraisal petitioners.

For example, in February, the Delaware Supreme Court affirmed in full Vice Chancellor Glasscock’s decision in Huff Fund Investment Partnership v. CKx, Inc., No. 348, 2014, 2015 WL 631586 (Del. Feb. 12, 2015). The Court of Chancery’s decision in this appraisal action held that the merger price was the best indicator of fair value for the common stock of CKx, Inc. ("CKx"). See Huff Fund Investment Partnership v. CKx, Inc., C.A. No. 6844-VCG, 2014 WL 2042797, at *1 (Del. Ch. May 19, 2014). After trial, Vice Chancellor Glasscock concluded that while neither party presented a reliable valuation analysis, the transaction price was the best indicator of fair value because the company had run an auction process that was thorough, effective, and free of self-interest or disloyalty.

Two subsequent Court of Chancery decisions–Merlin Partners LP v. AutoInfo Inc, C.A. No. 8509-VCN (Del. Ch. Apr. 30, 2015) and Longpath Capital LLC v. Ramtron Int’l, C.A. No. 8094-VCP (Del. Ch. June 30, 2015)–reached similar conclusions. In both cases, the court rejected both management and expert cash-flow projections as unreliable, and relied on the merger price itself to determine fair value. One recent case, however, bucked that trend. In Owen v. Cannon, C.A. No. 8860-CB (Del. Ch. June 17, 2015), a case that did not involve a public company, Chancellor Bouchard issued an opinion ordering defendants to pay the plaintiff-shareholder $15.9 million more than the merger price per share. The court found the pre-merger management projections to be reliable because they were the product of a deliberate and iterative process, prepared by the current president of the company who was extremely well-informed about the company and its potential growth, and had been provided to lenders before the merger. The court utilized the preferred discounted cash flow valuation analysis to determine the fair value of plaintiff’s shares.

These cases instruct that Delaware courts will continue to closely scrutinize all inputs into the various valuation analyses advanced in appraisal actions. If these inputs (and most importantly, financial projections) are reliable, the court will not hesitate to calculate the value of shares under the discounted cash flow or other valuation analysis. If the inputs are unreliable, the Court of Chancery is much more likely to land on the merger price as the "fair" price of appraised shares.

G. Investor Activists and Appraisal Arbitrage

The marked increase in Delaware appraisal actions is fueled at least in part by "appraisal arbitrage," a practice in which hedge funds and stockholder activists purchase shares after the announcement of a merger and assert appraisal rights. On January 5, 2015, the Delaware Court of Chancery issued a pair of memorandum decisions reinforcing the ability to pursue appraisal arbitrage. In Merion Capital LP v. BMC Software, Inc., No. CV 8900-VCG, 2015 WL 67586, at *6, 8 (Del. Ch. Jan. 5, 2015) and In re Ancestry.Com, Inc., No. CV 8173-VCG, 2015 WL 66825, at *1 (Del. Ch. Jan. 5, 2015), Vice Chancellor Glasscock analyzed the standing requirements under Section 262 of the Delaware General Corporation Law for Merion Capital LP, which purchased shares of BMC Software and Ancestry.com after the record date of a take-private merger and an acquisition, respectively. Applying the reasoning of the 2007 case In Re Appraisal of Transkaryotic Therapies, Inc., Vice Chancellor Glasscock found that a record holder is "required to show that it held a quantity of shares it had not voted in favor of the merger equal to or greater than the quantity of shares for which it sought appraisal," and is not required to show that any previous owner did not vote in favor of the merger. Merion Capital LP, 2015 WL 67586, at *6, 8 (applying the reasoning in Transkaryotic, No. Civ. A. 1554-CC, 2007 WL 1378345, at *3 (Del. Ch. May 2, 2007)).

According to the Wall Street Journal, thirty-three public company appraisal rights actions were filed in Delaware in 2014, and the trend has continued in 2015. Facing this sharp increase in appraisal rights actions, some companies and private equity firms are pushing back against the practice of appraisal arbitrage. On March 6, 2015, the Council of Corporate Law Section of the Delaware State Bar Association (the "Council") released proposed amendments to the Delaware General Corporation Law that would diminish the economic incentives for appraisal arbitrage, but not deny appraisal rights to those purchasing shares after the announcement of a transaction. The Council published an accompanying paper, stating it did not "believe appraisal arbitrage upsets a proper balance between the ability of corporations to engage in value enhancing transactions and the ability of dissenting shareholders to receive fair value for their holdings." The proposed amendments would deny appraisal rights for de minimis claims with respect to shares listed on a national exchange, permitting dismissal of appraisal petitions by stockholders holding one percent or less of the outstanding stock of a public company or if the value of the merger consideration applicable to their shares is $1 million or less, regardless of whether the shareholder purchased the shares before the announcement of the transaction. The de minimis thresholds would not apply to appraisals arising from short-form mergers. The proposed amendments would also allow companies to limit the statutory interest that accrues from the effective date of the merger until judgment on the appraisal claim by paying a discretionary amount at any time prior to judgment. Any additional interest would be charged only if the amount of the adjudicated share price were higher than the amount the company paid and would be charged only on the difference between those two amounts. The proposed amendments require approval by, among others, the Delaware legislature and the Delaware Governor, and would not take effect until August 1, 2015.

H. Delaware Court Clarifies When Creditors Have Standing to

Bring Derivative Claims

On May 4, 2015, Vice Chancellor Laster clarified when a creditor of an insolvent corporation has standing to bring derivative claims. In Quadrant Structured Products Company, Ltd. v. Vertin, C.A. No. 6990-VCL, 2015 WL 2062115 (Del. Ch. May 4, 2015), the latest in a series of important decisions arising out of the same dispute, the court considered a question of first impression under Delaware law: whether that law imposes a continuous insolvency requirement for creditors to maintain standing to bring derivative claims against a corporation. The defendants contended that the corporation was currently solvent and argued that for a creditor to have standing to proceed with a derivative litigation against corporate fiduciaries, the corporation on whose behalf the creditor sues must be insolvent not only at the time of commencement of litigation but also continuously thereafter. Analyzing the equitable reasons for granting derivative standing, the court rejected the continuous insolvency requirement and held that, to have standing, the creditor must make its claim while the corporation is insolvent and continuously hold a debt claim against the corporation. The court reasoned that "whether the corporation is solvent or insolvent is not a bright-line inquiry and often is determined definitively only after the fact, in litigation, with the benefit of hindsight." Id. at *11. Furthermore, the insolvency is not a "transformational point" when the creditors gain an interest in the financial condition of a corporation; rather, even solvent entities pose risks to the ability of a creditor to recover on its debt.

The court acknowledged the possibility that "during the course of a derivative action, both stockholders and creditors could gain standing to sue." Id. at *12. A conflict could arise between these groups, "with creditors suing derivatively and alleging that the directors should pay damages for failing to chart a more conservative course that preserved the firm’s assets, while . . . stockholders were suing derivatively and alleging that the same directors should pay damages for failing to chart a sufficiently aggressive course." Id. However, the court noted that "creditors of an insolvent firm have no greater right to challenge a disinterested, good faith business decision than the stockholders of that firm" because the "the business judgment rule protects the directors of solvent, barely solvent, and insolvent corporations." Id. at *13 (quoting N. Am. Catholic Educ. Programming Found., Inc. v. Gheewalla, 930 A.2d 92, 101 (Del. 2007) (internal marks omitted).

I. Merger Settlement Produces Rare Special Dividend to Shareholders

On April 7, 2015, the Delaware Court of Chancery approved a combined $153.75 million settlement in In re Freeport-McMoRan Copper & Gold Inc. Derivative Litigation, No. 8145-VCN (Del. Ch.), a derivative suit over Freeport-McMoRan Copper & Gold Inc.’s ("Freeport") acquisition of two energy exploration firms: Plains Exploration & Production Co. and McMoRan Exploration Co., a company that Freeport had spun off in 1994. Freeport stockholders claimed that the company’s directors breached their fiduciary duties by paying too high a price to rescue the struggling McMoRan, in which Freeport, its board members and key executives owned shares. The plaintiffs also noted that six Freeport directors sat on McMoRan’s board, including James Moffett who served both as Freeport’s board chairman and McMoRan’s CEO.

After discovery, the plaintiffs and the individual defendants reached a settlement. Freeport agreed to pay a special dividend of $137.5 million, minus attorneys’ fees, to Freeport shareholders. In addition, Freeport’s financial advisor for the acquisitions, a unit of Credit Suisse Group AG, agreed to pay $16 million to Freeport shareholders to settle claims that it played a role in Freeport’s overpayment for the acquisition of the two targets. Freeport’s share of the settlement will be funded by $115 million from Freeport’s directors and officers insurance and $22.5 million from Freeport.

In addition to ranking among the largest derivative action settlements to date, the form of the settlement is highly unusual. In a typical derivative lawsuit, any recovery is paid back to the company itself. In the Freeport litigation, however, the settlement proceeds will be distributed directly to shareholders in the form of a special dividend. The plaintiffs argued that because corporate insiders benefited from the overpayment for McMoRan and Plains Exploration, the settlement proceeds should be paid directly to shareholders. The special dividend is expected to exceed 10 cents per share after legal fees and other costs.

J. Stockholders Challenge "Dead Hand Proxy Puts" in Credit Agreements

"Dead hand proxy puts" garnered increased stockholder attention during the first half of 2015, as the plaintiffs’ bar has sought to exploit a recent Delaware Court of Chancery bench ruling on the subject. See Pontiac General Employees Retirement System v. Healthways, Inc., C.A. No. 9789-VCL (Del. Ch. Oct. 14, 2014) (transcript ruling). Proxy puts are provisions in credit agreements that give a lender the power to accelerate a borrowing corporation’s debt obligations if a majority of its board is replaced by "non-continuing directors." Under a basic proxy put, "continuing directors" are either directors who were on the board when the debt contract was entered into or replacement directors who were approved by a majority of those initial directors (or their approved replacements); "non-continuing directors" are generally directors who were neither on the board when the agreement was executed nor approved by a qualified majority of the board thereafter. Because basic proxy puts define a "continuing director" to include those whose election or nomination was "approved" by the incumbent directors, the incumbent board can–and generally must–avoid acceleration of the corporation’s debt obligations by approving a dissident slate of incoming directors.

A "dead hand" provision, however, eliminates that possibility by providing that any director elected as a result of an actual or threatened proxy contest will be considered a non-continuing director for purposes of the proxy put, irrespective of whether the new director is approved by the incumbent board. Thus, adding a dead hand provision to a proxy put renders the borrowing corporation’s board powerless to approve a dissident slate to avoid acceleration of the company’s debt. Dead hand proxy put provisions have been criticized for their potential to entrench incumbent directors and to increase costs insofar as they might require a corporation to renegotiate its debt obligations on less favorable terms.

In Healthways, Vice Chancellor Laster denied a motion to dismiss fiduciary duty claims against the directors of Healthways, Inc. and an aiding and abetting claim against its lender, SunTrust Bank, for entering into a credit agreement containing a dead hand proxy put provision. The court held that the complaint had adequately alleged facts showing that the corporation’s stockholders may presently be "suffering a distinct injury" from the deterrent effect of the dead hand proxy put, even where the acceleration of the corporation’s debt under the provision was not imminent. This "Sword of Damocles," the court observed, "necessarily has an effect on people’s decision-making" regarding a proxy contest or negotiating for board representation. The court also reasoned that the claim was ripe in part because the board could not at a later time avert the financial harm that would be caused if the dead hand provision caused the company’s debt obligations to be accelerated.

At a settlement hearing on May 8, 2015, Vice Chancellor Laster clarified that the bench ruling had been based on the narrow facts known at the pleading stage of the case, including that the company was under pressure from stockholders and facing a potential proxy contest. Beyond the specific facts of the Healthways case, the ruling left undefined the exact circumstances needed to state a ripe "dead hand proxy put" claim.

Stockholders have reacted to the ruling by serving "inspection demands" for corporate books and records on Delaware corporations that have entered into credit agreements containing such provisions. These inspection demands theorize that directors breached their fiduciary duties by approving credit agreements containing "dead hand" provisions, knowing that they would be a deterrent against shareholder activism or proxy activity. The plaintiffs’ recent salvo of "cookie cutter" inspection demands has prompted a wholesale rethinking by Delaware corporations of the need for such "dead hand" provisions, and many companies have chosen to simply eliminate these provisions altogether. The second half of 2015 may tell us whether the controversy over "dead hand proxy puts" will be more than a passing fancy.

K. Delaware Supreme Court to Consider Financial Advisor’s Liability

In the coming months, the Delaware Supreme Court is expected to hear and resolve an appeal in In re Rural Metro Corp. Stockholders Litigation, a groundbreaking case that could have a major impact on liability for aiding and abetting breaches of fiduciary duty. As discussed in our 2014 mid-year update, this case highlights Delaware courts’ increasing focus on the role of a financial advisor in the sales process, and the potential conflicts that can arise from a financial advisor’s working with both the target and acquiring companies. On March 7, 2014, the Delaware Court of Chancery issued its order finding a financial advisor liable for aiding and abetting breaches of fiduciary duty by the board of Rural/Metro Corporation ("Rural") in connection with a going-private transaction. See In re Rural Metro Corp. Stockholders Litigation, 88 A.3d 54 (Del. Ch. 2014). On February 12, 2015, the Chancery Court awarded attorneys’ fees in the case, clearing the way for the Delaware Supreme Court to consider the case on appeal. On March 20, 2015, the financial advisor filed its notice of appeal, and as of the date of this Mid-Year Report, briefing is underway. A ruling is expected by the end of 2015. The Delaware Supreme Court’s upcoming decision could have significant implications for investment bankers providing financial advice to different parties to a transaction.

VIII. Shareholder Proposal/Proxy Disclosure Litigation Trends

A. Shareholder Proposals

1. Proxy Access

Proxy access continues to demand significant issuer attention. More than 100 proxy access shareholder proposals were submitted to companies for 2015 annual shareholder meetings. Additionally, according to Institutional Shareholder Services ("ISS"), by May 29, 2015, 84 proxy access proposals had appeared on ballots–more than four times the number appearing on ballots in 2014. Contributing to the volume of proxy access proposals was the Boardroom Accountability Project, a campaign launched in November 2014 by New York City Comptroller Scott Stringer and New York City pension funds, which submitted identical proxy access proposals to 75 companies. The proposals called for boards to adopt and present for stockholder approval a bylaw that would require the company to include in its proxy materials director nominees of up to 25 percent of the board by any stockholder owning three percent or more of the company’s outstanding common stock continuously for three years ("3%/3-year").

Several large institutional investors, including Vanguard Group and TIAA-CREF publicly support proxy access. Vanguard has indicated it prefers proxy access provisions that permit stockholders owning five percent of a company’s outstanding shares for three years the ability to nominate directors for up to 20 percent of the seats on the board. TIAA-CREF wrote a letter dated February 10, 2015 to the largest 100 companies in which it invests and urged the companies to adopt proxy access provisions for 3%/3-year shareholders. Several public pension funds, including the California Public Employees’ Retirement System, have also indicated support for varying formulations of proxy access provisions.

Adding to the prominence of proxy access proposals in 2015, companies also lost the ability to rely on SEC no-action relief to exclude stockholder proposals that conflict with managements’ proposals. On January 16, 2015, SEC Chair Mary Jo White released a statement saying that, "due to questions that have arisen about the proper scope and application of Rule 14a-8(i)(9)," she had directed SEC staff to review and report on the rule, which allows companies to exclude from its proxy materials shareholder proposals that directly conflict with a management proposal. SEC Public Statement, Statement from Chair White Directing Staff to Review Commission Rule for Excluding Conflicting Proxy Proposals, (Jan. 16, 2015), available at http://www.sec.gov/news/statement/statement-on-conflicting-proxy-proposals.html. The Division of Corporation Finance immediately announced that it would not express any views on the application of Rule 14a8-(i)(9) during the 2015 proxy season. SEC Public Statement, Announcement of the Division of Corporation Finance Related to Exchange Act Rule 14a-8(i)(9) for Current Proxy Season, (Jan. 16, 2015), available at http://www.sec.gov/news/statement /statement-on-conflicting-proxy-proposals.html.

The SEC’s statements came after the Division of Corporation Finance received a letter from the Council for Institutional Investors, in which it urged the SEC to reconsider its interpretation of Rule 14a-8(i)(9) in the no-action letter that SEC staff had issued to Whole Foods. Whole Foods sought to exclude a proposal that called for the company’s governing documents to be amended to permit 3%/3-year shareholders to include in the company’s annual proxy statement nominees for up to 20 percent of the company’s directors. Whole Foods decided to submit to shareholders a competing proposal, which provided stockholders holding nine percent of the company’s stock for a period of five years the right to include nominees for the greater of one director or ten percent of the board. Following the SEC’s December 1, 2014 no-action letter to Whole Foods, on January 9, 2015, the Council for Institutional Investors wrote a letter to the Division of Corporation Finance requesting that the Division alter its "interpretation of the ‘counterproposals’ basis for exclusion in the Commission’s Rule 14a-8," and arguing that the exclusion of the stockholder proposal does not allow stockholders "to express a preference on the formulation" of the stockholder proposal.

The voting results on proxy access at this point in the season reflect varying responses from both companies and stockholders. Monsanto held the first proxy access vote on January 30, 2015, and stockholders adopted a 3%/3-year proxy access proposal that the board opposed. According to Proxy Monitor, "[o]f the six [proxy access] proposals opposed by the company’s board and coming to a vote by April 28 . . . three won the support of a majority of shareholders and three did not." A news release issued by New York City Comptroller on April 17, 2015, indicated that by that date, "six of the original 75 companies at which proxy access resolutions were filed have agreed to implement meaningful reform: Abercrombie & Fitch, Big Lots, Inc., Splunk Inc., Staples, Inc., United Therapeutics Corporation, and Whiting Petroleum–and a seventh company, Apache Corporation, has agreed to support the resolution." The news release further indicated that "at least sixteen companies, including Bank of America, Citigroup, GE, Prudential Financial and Yum! Brands have taken similar steps to implement meaningful proxy access since November in response to requests by the New York City Pension Funds or other investors." And according to ISS, as of May 29, 2015, of the 32 companies with available results, proxy access proposals following the 3%/3-year formulation have received 54.9 percent stockholder support.

2. Trinity Wall Street v. Wal-Mart

As discussed in our 2014 year end update, the case to watch in the shareholder proposal litigation arena is Trinity Wall Street v. Wal-Mart Stores, Inc., in which the U.S. District Court for the District of Delaware granted summary judgment in favor of a stockholder challenging Wal-Mart’s decision to exclude under SEC Rule 14a-8 the stockholder’s proposal from its 2014 proxy materials. No. 14-405-LPS, 2014 WL 6790928, at *1-2 (D. Del. Nov. 26, 2014). On April 14, 2015, the Third Circuit reversed the district court’s judgment, and on July 6, 2015, it issued its opinion. Trinity Wall St. v. Wal-Mart Stores, Inc., No. 14-4764, 2015 WL 4069291, at *17 (3d Cir. July 6, 2015). The Third Circuit panel unanimously agreed that the proposal was excludable under Rule 14a-8(i)(7), although a concurring opinion applied a different analysis than the majority opinion, and two of the judges also concluded that the proposal was excludable under Rule 14a-8(i)(3) as being vague and indefinite. The opinion will be discussed in our forthcoming Client Alert.

B. Executive and Director Compensation

1. SEC Proposes Pay-Versus-Performance Disclosure

Rules