Life Sciences 2023 Year End Review / 2024 Outlook

Overview

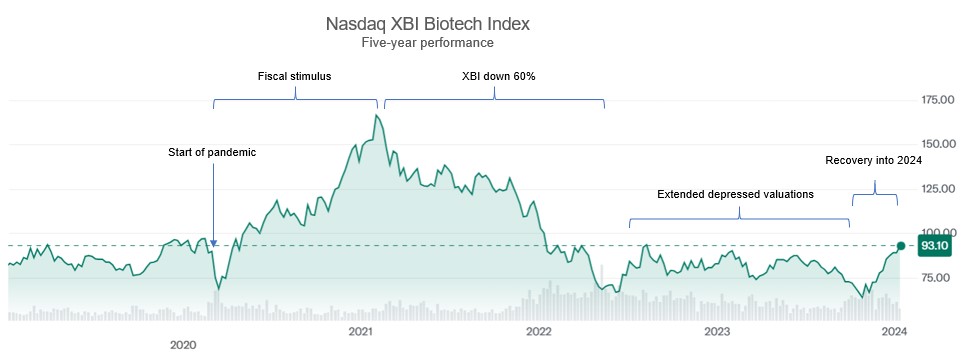

The past five years have been particularly tumultuous in the biopharma sector. Strong capital markets and M&A activity into early 2020 were whipsawed during the pandemic, with equity valuations climbing significantly through early 2021 before dropping dramatically through the fourth quarter of 2023. While dedicated healthcare funds have remained in the market during this time, generalist funds pulled back significantly in 2022 and 2023, leaving the sector with insufficient capital on the whole to support the number of public (and aspiring to be public) biopharma companies. This was reflected in the fact that over 200 Nasdaq-listed biopharma companies were trading below their cash balances as of Q3 2023. As a result, many biopharma companies sought less dilutive sources of capital, including royalty-based financing and third-party funding of clinical trials, while others explored sales, reverse mergers and liquidations. At the same time, a select group of companies with particularly attractive assets (either de-risked or in a therapeutic space with high investor interest) were still able to raise capital on favorable terms. Starting in the fourth quarter of 2023, we saw the XBI rally with the broader market, which seemed to signal a bottoming out of the market and an ability more broadly to access capital. Also during this time, large pharma has amassed substantial cash balances coming out of the pandemic and from the sale of blockbuster GLP-1 drugs. This led to a strong year in 2023 for larger M&A transactions (over $1 billion), albeit with the sense that it was a buyer’s market taking advantage of the lower equity valuations of the target companies. Looking ahead, we expect a more stable capital environment in 2024, which will support capital formation and continued M&A activity, although uncertainty remains with increased geopolitical tensions, a pending presidential election in the United States and continued economic uncertainty globally.

Below, we have provided a recap of 2023 highlights for capital markets, M&A activity, royalty finance transactions and clinical funding arrangements, along with expectations for 2024. As we enter this new year, we are cautiously optimistic that the coming year will provide a favorable deal environment for the biopharma sector and represent a return to a more balanced environment.

Practice Area Highlights

Capital Markets | Year in Review

Summary

Through much of 2023, the capital raising environment for biopharma companies continued to be very challenging, which continued a downward trend on equity valuations that started with the decline of the Nasdaq XBI biotech index starting in February 2021 (representing a peak-to-trough decline of 61% through 2023). The decline appears to have bottomed out in late 2023, with the XBI recovering 39% in the fourth quarter of 2023 and ending the year up 7%. Over the course of 2022 and 2023, many public companies experienced stock price declines even on the announcement of positive data, as material news would catalyze higher trading volumes and allow institutional investors the opportunity to further unwind their positions, even if at a loss. For the small subset of public and private companies raising capital that happened to be in high demand (e.g., attractive therapeutic space, de-risked programs, etc.), these companies had no apparent difficulty accessing capital markets at reasonable valuations. But for the majority of the public and private biopharma companies, 2023 continued to be a challenging year to raise capital, with a glimmer of hope coming at the end of 2023 that the coming year will represent a return to a more balanced market environment.

Private Capital Markets

The number of “first financings” (a metric that reflects biotech company creation) continued to trend downward in 2023, after peaking on a quarterly basis in Q1 of 2021 (161). As a broader trend, venture capital has continued to fund outstanding new ideas, but has demonstrated more selectivity, as reflected in the 56 “first financings” completed in Q3 of 2023. Healthcare-focused funds continued to lead this effort, with generalist funds largely sitting on the sidelines or temporarily leaving the sector. The frequency of larger venture rounds tracked a similar decline with $100mm+ rounds declining from 37 to 18 over the same period. Overall, quarterly VC funding has largely stabilized at ~$5B per quarter, which is roughly only one half of the highest quarterly fundraising totals of 2020 and 2021, but is nonetheless higher than any quarter between 2010 and late 2017. Mimicking the IPO market (more below), crossover rounds by the top public biotech funds have also decreased to a range of roughly 10 to 20 per quarter (as compared to nearly 60 in Q1 of 2021).

Public Capital Markets

The 12 biotech IPOs completed in 2023 barely eclipsed the 11 completed in 2022, with many issuers opting to continue lurking in the private markets or choosing to go public via reverse merger. Accordingly, the backlog of late-stage private companies doubled between Q2 of 2021 (65) and the end of 2023 (130+), suggesting a potential traffic jam on the public company offramp in 2024 and 2025 as many companies compete for capital. Whether this will translate into an influx of IPOs or continue to contribute to the validation of reverse mergers as a “going public” option, remains to be seen. With the continued glut of fallen angels trading below cash, the reverse merger opportunity is likely to remain viable for at least another year or six quarters.

As companies continued to reach data-driven catalysts, the follow-on public offering market maintained its strength in 2023 with approximately 30-40 transactions per quarter for total gross proceeds between $5 and $7B. Follow-on offerings, including PIPEs, reached a 2023 volume peak in Q2 with 47 deals grossing $20mm or more. Many companies, however, discovered that only exceptional data generate the desired pre-financing market reaction and companies with merely “good” data received a flat or negative reaction, as data releases would catalyze higher trading volumes, which would frequently provide an opportunity to liquidate existing positions without regard to price or valuation. In contrast, the 2024 biotech new issue market appears to be off to a promising start prior to the JP Morgan Healthcare Conference, with eight follow-on offerings and one convert completed in the first week of January with aggregate gross proceeds of $1.9B, versus ten follow-on offerings completed in all of January 2023 with aggregate gross proceeds of $1.3B.

Representative Capital Markets Transactions

Consistent with the theme from 2023 of high quality companies being able to raise capital despite an overall challenging macro environment, three biopharma IPOs stand out (Acelryin, Apogee Therapeutics and RayzeBio), each having raised over $300 million in their IPOs.[1] Among these, the Apogee IPO is distinguished as having a particularly strong performance post-IPO and an accelerated timeline from initial formation in February 2022, a $169 million Series B crossover round in November 2022 and an IPO in July 2023. The accelerated funding pathway for Apogee and strong performance post-IPO was due to investor interest in the inflammatory and immunology space, a strong management team and a blue chip investor base since formation. This combination made Apogee a strong candidate for private and public capital markets and made Apogee one of the best performing biopharma IPOs in 2023.

The Apogee IPO also is notable as certain pre-IPO investors elected to receive shares of non-voting common stock in lieu of common stock upon conversion of the preferred stock at the time of the IPO. Non-voting stock is used in this context to keep beneficial ownership of the voting stock below certain thresholds for SEC reporting and compliance purposes. The non-voting stock issued in this context is similar to the issuance of pre-funded warrants or “toothless” preferred stock, each of which are frequently used by other issuers in follow-on offerings. However, the use of non-voting common stock, if authorized in an issuer’s charter (such as at the time of an IPO), offers certain advantages over the use of pre-funded warrants or toothless preferred stock.

* * *

Note: Gibson Dunn represents Apogee Therapeutics.

Special thanks to Jefferies for contributing data regarding 2023 biotech new issuances.

[1] Additionally, Johnson & Johnson spun out Kenvue, its consumer health business, with a $4.2 billion IPO in 2023.

Mergers and Acquisitions | Year in Review

Summary

Despite a challenging regulatory environment and uncertain economic landscape, 2023 was a strong year for M&A in the biopharma sector, with deal values increasing by 37% from 2022, while deal volumes declined modestly year-over-year by 8%.[1] Large pharma has substantial cash reserves available to deploy and a need to solve for patent expiries and revenue gaps following the pandemic and the passage of the Inflation Reduction Act (IRA). With these trends continuing into 2024 against the backdrop of a more stable capital market environment, M&A activity is expected to remain strong in 2024, particularly in the areas of targeted oncology, immunology and next-generation GLP-1 agonists and similar weight loss and cardiometabolic targets. However, geopolitical instability and the continuing risk of a broader economic slowdown loom as broader risks in the background.

2023 Highlights

The Nasdaq XBI biotech index suffered a 23% decline through the first three quarters of 2023 (and an overall decline of 61% from the peak in February 2021). The fourth quarter of 2023 witnessed some strength, as the index rose 39% in the fourth quarter and ended 2023 up 7% for the year. This very difficult period from February 2021 through the fourth quarter of 2023 saw several hundred Nasdaq-listed biotech companies trading below their cash value, often despite strong clinical results and still-robust pipelines. This post-pandemic bust created a buyer’s market in the M&A space, where bidders with substantial resources could potentially buy assets or entire companies at significant discounts to valuations from a few years’ prior.

At the same time, large pharma had amassed nearly $1.34 trillion of capital to invest, which is close to an all-time high. Much of this came from the pandemic[2] and the boom of GLP-1 weight loss drugs[3]. Taking advantage of distressed valuations and large cash balances, pharma began to more aggressively buy up larger companies in 2023, including:

- Pfizer’s $43.0 billion acquisition of Seagen (the largest biopharma M&A transaction since 2019);

- Merck’s $10.8 billion acquisition of Prometheus;

- Biogen’s $7.3 billion acquisition of Reata;

- Astellas’ $5.9 billion acquisition of Iveric; and

- Sobi’s $1.7 billion acquisition of CTI BioPharma.

This increase in big-ticket M&A occurred in the context of an often challenging macro environment. The FTC has continued its hostility toward business combinations, including acquisitions with little overlap in product portfolios, although these transactions continue to close despite frequently extended review periods. Concerns over a potential hard landing have eased, providing buyers with more certainty around the likely near-term economic cycle, while the IRA and Medicare pricing negotiations have had a mixed effect on M&A. On the one hand, the IRA has created the specter of revenue shortfalls for large pharma as mature drugs become subject to forced Medicare negotiations. On the other hand, the overall market size and corresponding value for biopharma pipeline assets may be trimmed as buyers take into account future IRA price negotiations and/or foregone follow-on indications that could subject a smaller drug to the IRA pricing provisions (either as an orphan drug with a second approved indication or due to increased sales volumes).

2024 Outlook

The drivers of M&A activity in 2023 remain in place: strong balance sheets for large pharma, the need to backfill revenue holes and favorable biopharma valuations relative to 2020 and 2021 levels. At the same time, biopharma equity valuations have stabilized, which may allow targets to better fund development pipelines and increase equity values while forestalling M&A activities. This represents more of a return to normalcy for the biopharma targets and provides greater flexibility in capital planning, allowing for more opportunistic sell-side M&A processes. For this reason, we expect that the deal environment in 2024 will shift from being a buyer’s market to a more neutral stance, with a particular focus on targeted oncology, immunology and cardiometabolic programs, including next-generation GLP-1 agonists.

The same dominant macro environment conditions from 2023 are expected to persist into 2024, coupled with growing geopolitical tensions and a looming U.S. presidential election. Yet, despite these headwinds, we expect that the M&A deal environment will remain strong in 2024.

* * *

Note: Gibson Dunn represents CTI BioPharma

[1] Source: PwC analysis of S&P Capital IQ data for November 12, 2022 through November 15, 2023.

[2] Pfizer sold $37.8 billion of COVID-19 vaccines in 2022 while Moderna sold $18.4 billion in COVID-19 vaccines in the same year.

[3] Novo Nordisk’s GLP-1 drug Ozempic is expected to have sold $12.4 billion in 2023.

Royalty Financings | Year in Review

Summary

Against the backdrop of depressed equity valuations since February 2021, many biopharma companies were actively seeking to fund operations through less dilutive means. At the same time, institutional investors have increasingly been looking for investment returns in a volatile market that are uncorrelated with the overall stock market and broader economic cycles. These two objectives have aligned in recent years to drive an increase in royalty financing transactions in the life sciences, including both traditional royalty monetizations (the sale of a future royalty stream from an existing license agreement) and synthetic royalty transactions (borrowing against or selling a portion of future revenues from sales of a drug that has not been licensed to a third party). We expect these trends to continue to drive more royalty financing transactions in 2024, despite a higher interest rate environment and anticipated greater stability in equity valuations.

2023 Year in Review

We saw a significant increase in both the number of transactions and overall deal size for royalty financing transactions, in general, and for synthetic royalty financings during the pandemic and continuing through 2023.[1] Starting in 2020, the number and overall deal size of synthetic royalty transactions and royalty financing transactions overall completed by the top royalty funds in the life sciences space increased by approximately 350% and 25% (number), and 450% and 30% (overall deal size), respectively, from 2019 and earlier periods, while remaining high through 2023, despite the Federal Reserve raising interest rates.

Highlights of deal terms from recent royalty financings include the following trends:

- The average upfront payment was approximately $140 million, with an average upfront of approximately $215 million for royalty monetizations and $80 million for synthetic royalty transactions (either structured as a royalty-backed loan or a sale of a portion of future revenues). The average upfront payment for royalty monetizations and synthetic royalty transactions dropped in value 2021 and 2022, respectively, but increased in value in 2022 (continuing through 2023) and 2023, respectively.

- Of the 89 royalty financing transactions reviewed during this period, 56 did not have a cap on the investor’s return of capital, of which 44 were royalty monetizations and 12 were synthetic royalty transactions; The percentage of deals without caps remained steady throughout the time period reviewed.

- 23 of the royalty financing transactions included liens (or restrictions on liens in the form of negative covenants) with respect to product-related assets, of which 7 transactions were royalty monetizations (including royalty-backed notes) and 16 were synthetic transactions. The percentage of royalty financing transactions that included liens on product-related assets remained steady throughout the time period.

These economic trends reflected the overall market dynamics of a royalty monetization (and true sale of part (or all) of the economic interests from the license agreement) versus a synthetic royalty financing, which is more bespoke and may be structured as a true sale or as a debt-like royalty-backed financing that is often (but not always) non-recourse.

Representative Royalty Monetization Transaction

While many royalty monetization transactions are uncapped sales of a royalty entitlement, these transactions can also be consummated as loans, which may have tax advantages over an outright sale and which provide for a capped return to the investor. In these structures, the excess value of the royalty stream after the repayment of the loan is returned to the seller while the lender’s recourse is limited to the royalty entitlement.

The recent non-recourse $140 million royalty-backed loan from Blue Owl Capital to XOMA Corporation is an example of one such arrangement. In this facility, XOMA contributed its rights to receive royalties on sales of VABYSMO (faricimab) to a newly formed subsidiary, which then borrowed $130 million (with a potential $10 million draw later) against this royalty stream. The subsidiary is obligated to make semi-annual payments at a fixed rate of 9.875% per year until the loan is repaid, at which time the royalty payments will revert back to XOMA’s subsidiary. The loan is non-recourse to XOMA and repayment is tied to future VABYSMO royalties.[2]

2024 Outlook

The factors driving royalty financings over the last several years are expected to continue through 2024. The continued volatility of the capital markets, high interest rates, pharmaceutical companies’ focus on raising non-dilutive capital, and investors desire for stable investments divorced from the capital markets are expected to continue to drive an increase in these arrangements. Even with a more robust equity capital market environment, we expect that royalty financings will increasingly be considered as a means of providing a substantial portion of the capital needed for a company’s general operations without diluting equity or the inflexible repayment terms of leveraged finance. Whether they continue at the rate seen in 2023 remains to be seen.

* * *

Note: Gibson Dunn represents Xoma Corp.

Special thanks to Cowen for contributing data regarding royalty financing arrangements.

[1] Data was compiled from a Gibson Dunn survey of royalty financings from 2019-June 2023 by Royalty Pharma, DRI Capital, Healthcare Royalty Partners, OMERS, Oberland Capital, CPPIB, and Blackstone.

[2] Additionally, XOMA issued to Blue Owl warrants to purchase an aggregate of up to 120,000 shares of XOMA’s common stock (roughly 1% of the outstanding shares) in three tranches with implied premiums of 122%, 170%, and 217% to the price of XOMA’s common stock at closing.

Clinical Funding Agreements | Year in Review

Summary

Development funding arrangements offer biotechnology companies capital needed to fund costly clinical studies. Investors bear clinical development and regulatory risks, with a return of capital in a positive outcome scenario. Despite the fact that these arrangements have been in existence in one form or another for nearly two decades,[1] development funding had continued to occupy a niche space in the biopharma capital planning toolkit. More recently, the number of capital providers has increased, resulting in more overall available capital and more competitive terms. The growth of this asset class caught a tail wind in 2022 and 2023 as biotech valuations plunged, making it more difficult for clinical-stage companies to raise capital and increasing demand for non-dilutive financing alternatives. At the same time, large pharmaceutical companies looked to these arrangements as a way of defraying R&D costs and improving profit margins. As a result, we have seen a greater number of clinical funding arrangements and a notable increase in the consideration of these arrangements as part of overall capital planning. We expect these trends to continue in 2024 as at least one active investor in this space raises its next fund and overall macro conditions continue to favor non-dilutive sources of capital.

2023 Year in Review

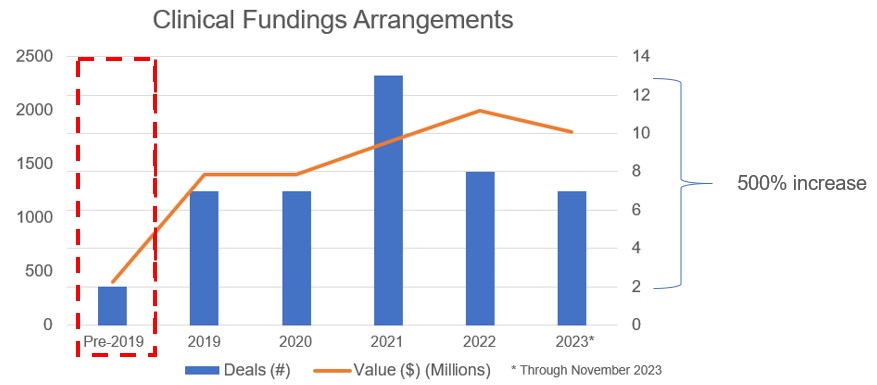

Over the past 5 years, there has been nearly a 5-fold increase in total funding commitments for R&D funding transactions. The following graph illustrates this increase in the overall volume of transactions and capital funding since 2019.

Despite this increase, the total number of clinical funding arrangements remains small in absolute terms. The more active capital providers in this space include the following (in alphabetical order):

- Abingworth

- Avillion[2]

- Blackstone Life Sciences

- NovaQuest Capital Management

- Royalty Pharma

- SFJ Pharmaceuticals

More of these programs are entered into by large pharma partners looking to defray clinical development costs and manage expenses and earnings than biotechnology companies. As a result, these programs often go unreported in SEC filings, as they are not sufficiently material to require separate disclosure. However, typical indicative terms include the following features:

- upfront funding of capital in support of a stage-stage clinical program (typically a Phase 3 program, with some Phase 2 programs), with additional funding payments made over time as development costs are incurred;

- milestone payments upon regulatory approval of the program, providing for a return of capital over a period of several years (e.g., 5 – 8 years from approval); and

- sales-based milestone payments and/or royalty payments upon commercialization, providing for a further return on the investment by the capital provider, frequently capped at an overall rate of return (e.g., 300% – 400% of the invested amount).

Representative Funding Arrangement

In 2023, Royalty Pharma entered into a $125 million funding arrangement with Teva Pharmaceuticals to fund Teva’s Phase 3 clinical research program for olanzapine LAI, a once-monthly long-acting injection for the treatment of schizophrenia. Royalty Pharma will provide Teva up to $100 million for Phase 3 development costs, with a mutual option to increase the total funding amount to $125 million. Upon FDA approval, Teva will repay to Royalty Pharma the total amount funded over five years. Upon commercialization, Teva will pay a low-to-mid single-digit royalty on product sales. If Teva chooses not to file a New Drug Application with the FDA following positive Phase 3 study results, Teva will pay Royalty Pharma 125% of the total amount funded.

2024 Outlook

The drivers of increased use of clinical funding arrangements over the last several years are expected to remain into 2024. The continued headwinds in biotech capital markets and pharma’s continued focus on managing earnings are expected to continue to fuel an increase in these arrangements. If market conditions improve and equity capital markets reopen, it is possible that the proliferation of these arrangements will slow. However, even with a more robust equity capital market environment, we expect that these arrangements will increasingly be considered as a means of providing a substantial portion of the capital needed for late-stage clinical programs without dilution or the inflexible repayment terms of leveraged finance.

* Note: Gibson Dunn represents Royalty Pharma and Avillion

Special thanks to Blackstone Life Sciences and Cowen for contributing data regarding clinical funding arrangements.

[1] Celtic Pharma was an early entrant into the clinical funding arrangement space in 2005, albeit with a different structure than the current arrangements that return invested capital via milestones and royalties versus an outright acquisition of late-stage programs that lacked sufficient funding for pivotal trials.

[2] Unlike other clinical funding providers, Avillion will assume responsibility for the conduct of the late-stage trial that is the subject of the funding arrangement.

Click here to download the Gibson Dunn Life Sciences 2024 Outlook (PDF).

This document is for informational purposes only and does not, and is not intended to, constitute legal advice or create an attorney-client relationship. You should contact a Gibson Dunn attorney directly to see if they are able to provide legal advice with respect to a particular legal matter.