A Primer on Real Estate Investment Trusts, Business Trusts and Stapled Trusts in Singapore

Client Alert | September 2, 2021

|

1. |

INTRODUCTION |

|

1.1 |

Singapore has become an increasingly popular destination for trust listings in the recent years. Real estate investment trusts (“REITs”), business trusts (“BTs”) and stapled trusts are some of the more popular vehicles that property players opt for to tap capital on Singapore Exchange Securities Trading Limited (the “SGX-ST”). |

|

1.2 |

This primer provides an overview of the structure of such vehicles, the main regulations regulating them, the process to getting listed on the SGX-ST as well as the various ways of acquiring control of these vehicles post-listing. This primer also explores the lessons to be learnt from the controversy surrounding Eagle Hospitality Trust (“EHT”) and the failed merger between ESR REIT and Sabana REIT. |

|

2. |

STRUCTURE |

|

2.1 |

REIT |

|

2.1.1 |

A REIT may generally be described as a trust that invests primarily in real estate and real estate-related assets with the view to generating income for its unitholders. | |||||||||

|

2.1.2 |

It is constituted pursuant to a trust deed entered into between the REIT manager and the REIT trustee. | |||||||||

|

2.1.3 |

The REIT manager manages the assets of the REIT while the REIT trustee holds the assets on behalf of the unitholders and generally helps to safeguard the interests of the unitholders. | |||||||||

|

2.1.4 |

REITs are popular with investors as the income from the assets (after deducting trust expenses) is distributed to the unitholders at regular intervals. A REIT which distributes at least 90% of its taxable income to its unitholders in the same year in which the income is derived can enjoy tax transparency treatment under the Income Tax Act, Chapter 134 of Singapore. It is also not uncommon for REITs to pledge to distribute the entire of its annual distributable income in the initial period post-listing. | |||||||||

|

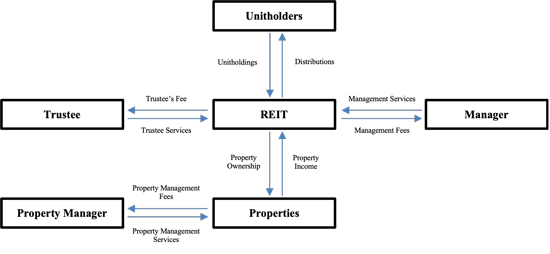

2.1.5 |

The typical roles in a REIT structure are as follows: | |||||||||

|

| |

|

Typical REIT Structure |

|

2.1.6 |

SGX-ST-listed REITs typically adopt an external management model where the REIT manager is owned by the sponsor of the REIT. This is in contrast to an internal management model (adopted by a majority of REITs in the United States of America) where the REIT manager is instead owned by the REIT itself. Proponents of an internal management model in Singapore argue that an internal management model avoids conflicts of interest and lowers the fees payable to the REIT manager (which ultimately translates to better returns for unitholders). The success of the Hong Kong-listed internally managed Link REIT, Asia’s largest REIT in terms of market capitalization, may bear testament to this. However, whether an internal management model takes off in Singapore remains to be seen. Singapore investors could well prefer sponsor participation due to the various advantages that a sponsor can bring, such as marketability, expertise, support and pipeline of assets. |

|

2.2 |

BT |

|

2.2.1 |

A BT is a trust that can generally engage in any type of business activity, including the management of real estate assets or the management or operation of a business. | |||||||

|

2.2.2 |

It is constituted pursuant to a trust deed entered into by the trustee-manager, a single entity that has the dual responsibility of safeguarding the interests of the unitholders of the BT and managing the business conducted by the BT. | |||||||

|

2.2.3 |

BTs, unlike companies, can make distributions out of operating cash flows (instead of profits). They suit businesses which involve high initial capital expenditures with stable operating cash flows, such as real estate assets. | |||||||

|

2.2.4 |

Compared to REITs, BTs are also more lightly regulated and may therefore be preferred for their flexibility. Property BTs often also pledge to provide REIT-like distributions to the unitholders. | |||||||

|

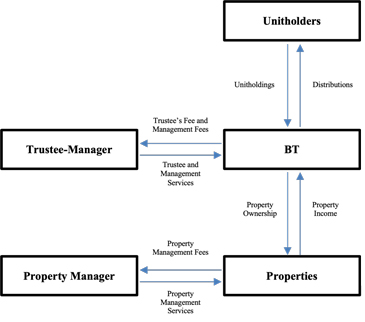

2.2.5 |

The typical roles in a BT structure are as follows: | |||||||

|

| |

|

Typical Property BT Structure |

|

2.3 |

Stapled Trust |

|

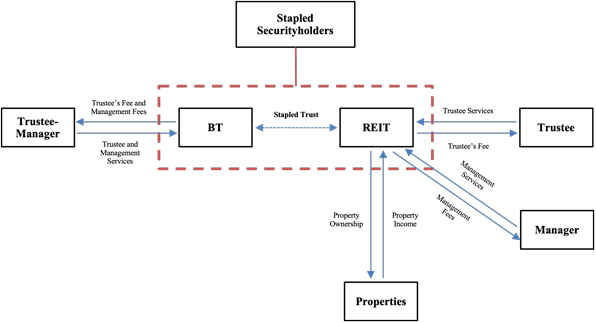

2.3.1 |

A stapled trust on the SGX-ST typically comprises a REIT and a BT. Pursuant to a stapling deed, units of the REIT and units of the BT are stapled together and cannot be traded separately. The REIT and the BT would continue to exist as separate structures, but the stapled securities would trade as one counter and share the same investor base. | |

|

2.3.2 |

A stapled trust structure may be preferred when an issuer wishes to bundle two distinct (but related) businesses into a single tradeable counter. Such stapled trust structure is commonly adopted for hospitality assets which provide both a passive (through the receipt of rental income from the lease of such assets) and an active (through the management and operation of such assets) income stream. | |

|

2.3.3 |

In such cases, the REIT will be constituted to hold the income-producing real estate assets and the BT will be constituted to either (a) be the master lessee of the real estate assets who will manage and operate these assets or (b) remain dormant and only step in as a “master lessee of last resort” to manage and operate these assets when there are no other suitable master lessees to be found. The presence of a BT also offers flexibility for the stapled trust to undertake certain hospitality and hospitality-related development projects, acquisitions and investments which may not be suitable for the REIT. | |

|

2.3.4 |

Investors who value the business and income diversification may therefore find such a model attractive. | |

|

2.3.5 |

The typical roles in a REIT and a BT have been discussed above. |

| |

|

Typical Stapled Trust Structure |

|

3. |

REGULATIONS | ||||||||||||||||||||||||

|

3.1 |

REIT | ||||||||||||||||||||||||

|

|

3.2 |

BT | ||||||||||||||||||||

|

|

3.3 |

Stapled Trust | ||||

|

|

4. |

LISTING | ||||||||||||||||||||||||||||||||||||||||||||||||||||

|

4.1 |

Due Diligence | ||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

4.2 |

Listing Process | ||||||||||||||||||||||||||

|

|

4.3 |

Prospectus | ||||||||||||||||||||||||||||||||||||||||||||||||

|

|

4.4 |

Continuing Listing Obligations | ||||||||||||||||||||||||||||||||||||||||||||

|

Post-listing, REITs, BTs and stapled trusts are subject to continuing listing obligations under the Listing Manual, such as the requirement to announce specific and material information, requirements relating to secondary offerings, interested person transactions and significant transactions, as well as requirements relating to circulars and annual reports. | |||||||||||||||||||||||||||||||||||||||||||||

|

4.5 |

Case Study of EHT | ||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||

|

5. |

Acquiring Control of a REIT, BT or Stapled Trust | ||||||||||||||||||||||||||||||||||||||||||||

|

5.1 |

An acquisition of all the units of a REIT or BT or all the stapled securities of a stapled trust listed on the SGX-ST (“Target Entity”) may be effected in various ways, such as a take-over offer, a trust scheme of arrangement (“Trust Scheme”) and a reverse take-over (“RTO”). | ||||||||||||||||||||||||||||||||||||||||||||

|

5.2 |

Any merger or acquisition involving a Target Entity would be subject to the Listing Manual, the CIS Code (in the case of a REIT) and the Singapore Code on Take-overs and Mergers (the “Take-over Code”). The Take-over Code is enforced by the Securities Industries Council (the “SIC”), which is part of the MAS. | ||||||||||||||||||||||||||||||||||||||||||||

|

5.3 |

Take-over Offer | ||||||||||||||||||||||||||||||||||||||||||||

|

|

5.4 |

Trust Scheme | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

5.5 |

RTO | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

5.6 |

Which method to adopt? | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding these issues. Please feel free to contact the Gibson Dunn lawyer with whom you usually work, or the authors of this primer in the firm’s Singapore office:

Robson Lee (+65.6507.3684, RLee@gibsondunn.com)

Kai Wen Chua (+65.6507.3658, KChua@gibsondunn.com)

Zan Wong (+65.6507.3657, ZWong@gibsondunn.com)

© 2021 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.