On June 8, 2021, in Oakwood Laboratories LLC v. Thanoo, the Third Circuit “endeavored to clarify the requirements for pleading a trade secret misappropriation claim under the Defend Trade Secrets Act” (the “DTSA”).[1] Enacted in 2016, the DTSA for the first time created a federal private cause of action for civil litigants seeking to protect trade secrets, allowing plaintiffs to seek injunctive relief and/or damages in the event of misappropriation. While other federal Courts of Appeal have previously commented on the DTSA’s similarity to various state trade secret laws,[2] as well as differences between the federal statute and certain state regimes,[3] it remains to be seen whether any will adopt Oakwood’s analyses. In the meantime, Oakwood is an important decision in this fast-evolving field of federal law of which those prosecuting and defending DTSA claims should be aware.

I. Background Concerning the Defend Trade Secrets Act

Prior to the relatively recent enactment of the DTSA, parties seeking to protect their trade secrets via civil litigation were limited to rights provided by various state laws. Through the DTSA, which provides that the “owner of a trade secret that is misappropriated may bring a civil action . . . if the trade secret is related to a product or service used in, or intended for use in, interstate or foreign commerce,”[4] Congress sought to create uniform national standards for trade secret misappropriation.

Courts have generally required plaintiffs to allege three elements to bring a claim under the DTSA: (1) the existence of a trade secret, (2) that is related to interstate or foreign commerce, and (3) misappropriation of that trade secret.[5] The DTSA defines “trade secrets” as a wide variety of “information” for which “reasonable measures” have been taken “to keep [the information] secret,” and which “derives independent economic value . . . from not being generally known” nor “readily ascertainable through proper means” to others “who can obtain economic value from [its] disclosure or use.”[6] The statute defines “misappropriation” as the “improper” “acquisition,” “disclosure” or “use” of such a trade secret.[7]

Plaintiffs who prevail on a trade secret misappropriation claim under the DTSA may obtain an injunction against further “actual or threatened misappropriation,” and recover damages calculated based upon (i) the plaintiff’s “actual loss,” (ii) “any unjust enrichment” derived by the defendant, or (iii) “a reasonable royalty” for the misappropriation.[8] If the misappropriation was willful and malicious, plaintiffs may also be entitled to reasonable attorney’s fees and “exemplary damages” of up to twice the damages they could otherwise receive.[9]

II. The Facts of Oakwood

The dispute in Oakwood pits Oakwood Laboratories, a pharmaceutical company, against its former senior scientist, Dr. Bagavathikanun Thanoo, and his new employer, Aurobindo Pharma U.S.A., Inc. After working for Oakwood for nearly twenty years, Dr. Thanoo left to take a new job with Aurobindo. Oakwood alleged that Dr. Thanoo misappropriated trade secrets in his new role regarding its “Microsphere Project,” which focused on a particular pharmaceutical technology.[10] In addition, Oakwood and Aurobindo had previously engaged in ultimately unsuccessful negotiations regarding a possible collaboration on the Microsphere Project, in connection with which Oakwood had shared certain proprietary information with Aurobindo pursuant to a confidentiality agreement.[11]

Oakwood alleged that, over the course of nearly 20 years, a team of 20-40 full-time Oakwood employees spent countless hours and approximately $130 million on the Microsphere Project.[12] Accordingly, Oakwood alleged that “the Microsphere Project is not something that could have been replicated” by Aurobindo in under four years “absent misappropriation of Oakwood’s trade secrets.”[13] Aurobindo nevertheless claimed to have done just that, while Oakwood alleges that Aurobindo’s apparent success necessarily reflects the misappropriation of Oakwood’s trade secrets.

The parties’ dispute reached the Third Circuit following four dismissals of various iterations of Oakwood’s complaint by the district court, with each complaint adding additional details not pleaded in earlier versions. The district court initially found that Oakwood failed to identify a specific trade secret,[14] while it subsequently held that later versions of the complaint sufficiently alleged a trade secret but did not adequately plead misappropriation nor how Oakwood had suffered any harm as a result thereof.[15] Rather than amend its complaint for a fourth time, Oakwood appealed from the dismissal of its third amended complaint.

III. The Third Circuit’s Interpretation of the Defend Trade Secrets Act

The parties in Oakwood primarily disagreed on the meaning and application of the first and third elements of a DTSA claim: identification of a trade secret and misappropriation thereof.[16] Accordingly, the Third Circuit first clarified the level of specificity required to plead a trade secret before discussing the definition of misappropriation under the statute. The Court also addressed the defendants’ argument that Oakwood had alleged only speculative harms because Aurobindo had not yet launched any products based on allegedly misappropriated trade secrets. As to each issue, the Third Circuit disagreed with the district court’s reasoning and held that Oakwood’s third amended complaint was sufficient to state a trade secret claim under federal law.

In addressing the level of specificity required to plead a trade secret, the Third Circuit relied on California state law in explaining that while a “trade secret must be described ‘with sufficient particularity to separate it from matters of general knowledge in the trade or of special knowledge of those persons who are skilled in the trade, and to permit the defendant to ascertain at least the boundaries within which the secret lies,’” plaintiffs nevertheless “need not ‘spell out the details of the trade secret’ to avoid dismissal.”[17] In doing so, the Third Circuit joined its sister circuits in noting that the DTSA is “substantially similar as a whole” to many states’ trade secret statutes,[18] the interpretation of which can inform federal courts’ interpretation of the DTSA.

Next, the Court explained that “[t]here are three ways to establish misappropriation under the DTSA: improper acquisition, disclosure, or use of a trade secret without consent.”[19] Although Oakwood had alleged misappropriation via improper acquisition and disclosure, the Third Circuit limited its analysis to “the ‘use’ of a trade secret” because each of the underlying facts relating to acquisition and disclosure concerned events that took place prior to the DTSA’s effective date of May 11, 2016.[20] In interpreting the term “use,” Oakwood turned to Texas state authority, under which “use” was “broadly defined” to mean “any exploitation of the trade secret that is likely to result in injury to the trade secret owner or enrichment to the defendant,” including “marketing goods that embody the trade secret, employing the trade secret in manufacturing or production, relying on the trade secret to assist or accelerate research or development, or soliciting customers through [its] use.”[21] In other words, the Court deemed a trade secret “used” through any way in which one “take[s] advantage” of it “to obtain an economic benefit, competitive advantage, or other commercial value.”[22] In particular, the Third Circuit rejected the district court’s equating of the term “use” with the term “replicate,” noting that the latter term is used elsewhere in the DTSA and thus the two words could not have been intended as synonyms.[23] The Third Circuit thus held that Oakwood could state a DTSA claim without expressly alleging that Aurobindo had copied its trade secret.

Lastly, the Third Circuit held that a plaintiff need not allege harm separate and apart from misappropriation because “misappropriation is harm.”[24] Trade secrets derive “‘economic value . . . from not being generally known’” or “‘readily ascertainable through proper means,’” such that their “economic value depreciates or is eliminated altogether upon its loss of secrecy when a competitor obtains and uses that information without the owner’s consent.”[25] Accordingly, the Third Circuit in Oakwood reasoned that even where defendants “have not yet launched a competing product, that does not mean that [a plaintiff] is uninjured” so long as it “has lost the exclusive use of trade secret information,” which is a “real and redressable harm,”[26]

Conclusion

The Third Circuit’s interpretation of elements of the DTSA will be instructive for litigants based within that Court’s jurisdiction, and may also have an impact in its sister circuits. Given the differing state trade secret regimes that have developed over many decades, as well as the developing case law regarding the DTSA, parties will be well-served by promptly consulting with experienced trade secret counsel when evaluating actual or potential trade secret claims.

_______________________

[1] 2021 WL 2325127, at *1, — F.3d — (3d Cir. 2021).

[2] See, e.g., InteliClear, LLC v. ETC Glob. Holdings, Inc., 978 F.3d 653, 657 (9th Cir. 2020); Akira Techs., Inc. v. Conceptant, Inc., 773 F. App’x 122, 125 (4th Cir. 2019).

[3] See, e.g., Compulife Software Inc. v. Newman, 959 F.3d 1288, 1311 (11th Cir. 2020) (noting “one important difference” between DTSA’s definitions of “misappropriation” and “improper means” and the definitions under Florida law).

[5] Oakwood, 2021 WL 2325127, at *8.

[10] Oakwood, 2021 WL 2325127, at *2.

[14] Oakwood Labs., LLC v. Thanoo, No. 17 Civ. 5090, 2017 WL 5762393, at *4 (D.N.J. Nov. 28, 2017).

[15] Oakwood Labs., LLC v. Thanoo, No. 17 Civ. 5090, 2019 WL 5420453, at *3–4 (D.N.J. Oct. 23, 2019).

[16] Oakwood, 2021 WL 2325127, at *8.

[17] Id. (quoting Diodes, Inc. v. Franzen, 260 Cal. App. 2d 244, 252-53 (Cal. Ct. App. 1968)).

[18] Oakwood, 2021 WL 2325127, at *8.

[21] Id. at *11 (quoting Gen. Universal Sys., Inc. v. HAL, Inc., 500 F.3d 444, 450-51 (5th Cir. 2007)).

[25] Id. at *15 (quoting 18 U.S.C. § 1839(3)(B)).

The following Gibson Dunn attorneys assisted in preparing this client update: Michael L. Nadler, Brian C. Ascher, Ilissa Samplin, Alexander H. Southwell, and Joshua H. Lerner.

Gibson Dunn lawyers are available to assist in addressing any questions you may have about these developments. Please contact the Gibson Dunn lawyer with whom you usually work, any member of the firm’s Trade Secrets practice group, or any of the following:

Joshua H. Lerner – Chair, Trade Secrets Practice, San Francisco (+1 415-393-8254, jlerner@gibsondunn.com)

Brian C. Ascher – New York (+1 212-351-3989, bascher@gibsondunn.com)

Ilissa Samplin – Los Angeles (+1 213-229-7354, isamplin@gibsondunn.com)

Alexander H. Southwell – New York (+1 212-351-3981, asouthwell@gibsondunn.com)

© 2021 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.

Decided June 23, 2021

Collins v. Yellen, No. 19-422

Yellen v. Collins, No. 19-563

Today, the Supreme Court held 6-3 that the structure of the Federal Housing Finance Agency—led by a single Director, removable only “for cause”—violates the Constitution’s separation of powers, but ruled 8-1 that a remand is necessary to determine the proper scope of relief.

Background:

Congress created the Federal National Mortgage Association (“Fannie Mae”) and the Federal Home Loan Mortgage Corporation (“Freddie Mac”) to provide liquidity and stability to the national mortgage market. In the Housing and Economic Recovery Act of 2008, Congress created the Federal Housing Finance Agency (“FHFA”) to regulate these enterprises. FHFA is headed by a single Director who serves a five-year term and is removable by the President only “for cause.”

In 2008, FHFA placed Fannie Mae and Freddie Mac into conservatorship and secured financing from the Treasury Department—which agreed to infuse hundreds of billions of dollars into the enterprises in exchange for preferred stock, dividends, fees, and the like—to keep them afloat.

In 2012, FHFA (led at the time by an Acting Director) and Treasury amended their financing agreements to require Fannie Mae and Freddie Mac to pay Treasury a quarterly dividend equal to nearly all of their net worth, rather than a dividend tied to Treasury’s capital investment.

Three shareholders challenged the amendment on statutory and constitutional grounds, arguing that FHFA’s single-Director structure independent-agency structure violates the Constitution’s separation of powers. The en banc Fifth Circuit held that FHFA’s structure violated the constitution but that the unconstitutionality could be cured by severing the Director’s “for cause” removal restriction. The Fifth Circuit also held that the Recovery Act forecloses the statutory claims against Treasury but not FHFA.

In January 2021, FHFA and Treasury amended the agreements for a fourth time to eliminate the net-worth-based dividend formula that caused the shareholders’ injuries.

Issues:

(1) Whether FHFA’s structure violates the separation of powers;

(2) If so, whether the fourth amendment (2021) moots the shareholders’ claims;

(3) If FHFA’s structure violates the separation of powers, whether the proper retrospective remedy is to set aside all actions taken by the unconstitutionally structured FHFA (including the 2012 amendment at issue); and

(4) Whether the Recovery Act forecloses the shareholders’ statutory claim.

Court’s Holding:

(1) Yes. FHFA’s structure as an “independent” federal agency headed by a single Director removable by the President only “for cause” violates the Constitution’s separation of powers.

(2) Yes, in part. Shareholders’ claims for prospective relief were rendered moot by the adoption of the fourth amendment in 2021. The retrospective claims were not mooted by the fourth amendment.

(3) No. There is no reason to set aside the third amendment because it was (i) adopted by an Acting Director who was removable at will and (ii) subsequently implemented by confirmed Directors who were appointed in a manner consistent with the constitution and thus possessed lawful executive power (only the statute’s removal provision was unconstitutional). The Court remanded for further proceedings to determine the retrospective relief, if any, to which the shareholders are entitled.

(4) The Recovery Act’s anti-injunction provision bars shareholders’ statutory claim.

What It Means:

- In step with the Court’s decision last term in Seila Law LLC v. CFPB, 140 S. Ct. 2183 (2020), today’s decision again recognizes the significant limitation on Congress’s ability to insulate agencies from presidential control. Agencies that execute federal law and are headed by a single Director, including financial regulators, cannot be “independent” of the President, but instead must be subject to the President’s constitutional duty to control the federal officers who assist the President in executing federal law.

- The Court’s holding that a federal agency headed by a single Director removable by the President only “for cause” is unconstitutional could have ripple effects. For example, the validity of the Social Security Administration’s leadership structure, which has been led by a single commissioner since 1994, may be called into question.

- The Court’s decision that all of FHFA’s actions while unconstitutionally structured need not be set aside could impact other litigation challenging actions that the Consumer Financial Protection Bureau took when it was unconstitutionally structured. But as the Court made clear, plaintiffs are entitled to retrospective relief so long as they can show that the unconstitutional removal provision inflicted compensable harm.

- The Court’s 8-1 decision on standing reiterated that, for traceability purposes, the relevant inquiry turns on whether the injury can be traced to the defendant’s allegedly unlawful conduct—not the provision of law being challenged.

The Court’s opinion is available here.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding developments at the Supreme Court. Please feel free to contact the following practice leaders:

Appellate and Constitutional Law Practice

| Allyson N. Ho +1 214.698.3233 aho@gibsondunn.com | Mark A. Perry +1 202.887.3667 mperry@gibsondunn.com | Lucas C. Townsend +1 202.887.3731 ltownsend@gibsondunn.com |

| Bradley J. Hamburger +1 213.229.7658 bhamburger@gibsondunn.com |

Related Practice: Administrative Law and Regulatory Practice

| Eugene Scalia +1 202.955.8543 escalia@gibsondunn.com | Helgi C. Walker +1 202.887.3599 hwalker@gibsondunn.com |

Overshadowed in the media by the historic judgment of 3 February 2021 by the Administrative Court of Paris in the “Affaire du siècle” (the Case of the century), a ruling by the Versailles Administrative Court of Appeal (the Court) on 29 January 2021 could also result in a historic ruling by the Court of Justice of the European Union (the CJEU). Indeed, upon referral by the Court, the CJEU will be called upon to rule on the existence of a right to breathe clean air and on the liability incurred by the Member States of the European Union in the case of disregard of their obligations in terms of air quality (Case C-61/21).

I. Context of the ruling rendered by the Court

Under Directive 2008/50/EC of 21 May 2008 on “ambient air quality and cleaner air for Europe” (the Directive), Member States must establish zones and agglomerations throughout their territory in which air quality is assessed (Article 4).

Article 13-1 of the Directive requires Member States to ensure that levels of fine particulate matter (PM10), carbon monoxide or nitrogen dioxide (NO2) do not exceed limit values set out in an annex.

Article 23-1 of the Directive provides that where these limit values are exceeded by levels of pollutants in ambient air, Member States must, in the given zone or agglomeration, adopt “air quality plans”. If the limit values are exceeded after the deadline for their application, the air quality plans provide for appropriate measures to ensure that the period of exceedance is as short as possible.

At the end of 2019, following an action for failure to fulfil obligations brought by the European Commission, the Court of Justice of the European Union ruled that France had failed to fulfil its obligations under Articles 13(1) and 23(1) of the Directive with regards to NO2 for several French regions, including the Paris region (CJEU, 24 October 2019, case C-636/18). On 30 October 2020, the European Commission announced that it would bring a new action against France before the CJEU for failure to fulfil obligations , it being specified that the failures this time deal with the excessive level of PM10 in the air.

For its part, the Conseil d’Etat (Council of State, France), the highest administrative court in France, had already ruled in 2017 that, given the persistence of observed exceedance of PM10 and NO2 concentrations in the air, the air quality plans for certain areas, including the Paris region, had to be considered insufficient with respect to the obligations and thresholds set by the Directive. The Conseil d’Etat had then enjoined the State to take the necessary measures to bring PM10 and NO2 concentrations below the limit values (CE, 12 July 2017, No. 394254). In a decision dated 10 July 2020, the Conseil d’Etat considered that the French State had not complied with the injunctions requested in the decision of 12 July 2017, and imposed a €10 million penalty on them if they did not justify having taken the required measures within six months of the decision (CE, ass., 10 July 2020, No. 428409). In light of the publicly available information, the Conseil d’Etat should soon rule on whether the French State has finally fulfilled its obligations.

It is in this context that the Court, sitting in plenary session, was called upon to rule on the action for damages brought by an applicant, resident of the Paris region, who attributed his various allergies to air pollution. The applicant considered that the deterioration of the air quality resulted in particular from the disregard by the French authorities of the obligations set by Articles 13(1) and 23(1) of the Directive.

II. Reasoning steps followed by the Court

It has been consistently held that “the principle of State liability for loss and damage caused to individuals as a result of breaches of [Community] law for which it can be held responsible is inherent in the system of the [Treaty on the Functioning of the European Union]” (CJEU, 5 March 1996, cases C-46/93 and C-48/93).

The CJEU also recalls that a right to reparation is recognized by European law if the following three conditions are met:

- the rule of law infringed must be intended to confer rights on individuals;

- the breach must be sufficiently serious, it being specified that this is the case if the breach has persisted despite a judgment by the CJEU finding the infringement in question to be established;

- there must be a direct causal link between the breach of the obligation resting on the State and the damage sustained by the injured parties.

In the present case, since it was seized of a claim for damages based on the breach of the Directive, i.e. of a norm of European law, the Court had to verify whether the three conditions mentioned above were met.

In order to determine whether the first condition had been met, the Court had first to decide whether Articles 13(1) and 23(1) of the Directive, which the applicant claimed had been disregarded, gave him a “right”. In other words, the Court had to determine whether these Articles conferred a “right to breathe clean air” eligible of giving rise to a compensation claim.

As early as 2014, the CJEU had indicated that Articles 13(1) and 23(1) allowed “persons directly concerned by the limit value being exceeded” to obtain, before the national authorities and courts, the establishment of an air quality plan in accordance with the requirements of Article 23 (CJEU, 19 November 2014, case C-404/13). It is, moreover, this right that was implemented by the Conseil d’Etat in the 2017 and 2020 decisions outlined above.

The Court probably considered that the right thus available to individuals to compel Member States to implement the obligations laid down by the Directive did not necessarily imply the recognition for their benefit of a “right to breathe clean air”, the disregard of which is likely to give rise to an action for damages.

Since the answer was uncertain and the issue was related to the scope of a European norm, the Court chose to refer two questions to the CJEU for a preliminary ruling on Articles 13(1) and 23(1) of the Directive in order to obtain the appropriate interpretation of these Articles.

The first question is relative to whether Articles 13(1) and 23(1) of the Directive give individuals, in the event of a sufficiently serious breach by a Member State of the European Union of the obligations arising therefrom, a right to obtain from the Member State in question, compensation for damage to their health which has a direct and certain causal link with the deterioration of air quality.

If the answer to the first question is affirmative, the Court then asked the CJEU to specify the conditions for the opening of this right, in particular with regards to the date on which the existence of the breach attributable to the Member State in question must be assessed.

III. Possible consequences of the Court’s ruling

If the CJEU were to answer the first of the questions asked by the Court in the affirmative, it would then be for the Court to determine whether the other two conditions for the French State’s liability to be characterized are met.

Insofar as France has already been subject of a breach judgment for failure to comply with its obligations with respect to NO2 (CJEU, 24 October 2019, cited above), the condition relating to the sufficiently serious breach of a right conferred on individuals does not seem to pose any particular difficulty.

It will then be up to the Court to assess whether there is a direct causal link between the violation and the damage claimed by the applicant, it being specified that this demonstration will depend on the answer given by the CJEU to the second question, namely from what date the existence of the violation attributable to the Member State in question must be assessed, and will probably require recourse to a medical expert opinion.

The recognition of a right to breathe clean air likely to be subject of an action for compensation would very probably constitute a strong constraint weighing on the Member States of the European Union. In this respect, it should be emphasized that France is far from being the only country in the European Union to have been condemned for failure to comply with the obligations set out in Articles 13(1) and 23 of the Directive: Italy has been condemned for systematic and persistent exceeding of the PM 10 limit values (CJEU, 10 November 2020, case C-644/18), the United Kingdom and Germany have been condemned in the same way, but for N02 (CJEU, 4 March 2021, case C-664/18 and CJEU, 3 June 2021, case C-635/18). The question of a possible compensation claim based on the disregard of the right to breathe clean air could thus have a repercussion in all of the European Union States.

The following Gibson Dunn attorneys assisted in preparing this client update: Nicolas Autet and Grégory Marson.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding these developments. Please contact the Gibson Dunn lawyer with whom you usually work, the authors, or any of the following lawyers in Paris by phone (+33 1 56 43 13 00) or by email:

Nicolas Autet (nautet@gibsondunn.com)

Grégory Marson (gmarson@gibsondunn.com)

Nicolas Baverez (nbaverez@gibsondunn.com)

Maïwenn Béas (mbeas@gibsondunn.com)

© 2021 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.

On June 11, 2021, New York Governor Andrew M. Cuomo signed into law a Uniform Foreign Country Money Judgments Act (the “2021 Recognition Act”), amending New York’s Uniform Foreign Country Money-Judgments Recognition Act of 1970 (the “1970 Recognition Act”).[1] The bill was designed to update and bring New York’s existing legislation in line with the revisions proposed by the Uniform Law Commission in 2005.[2] With this enactment, New York follows a growing number of U.S. states that have modernized their recognition acts over the last decade.

As detailed herein, the 2021 Recognition Act both clarifies the procedural mechanisms and substantive arguments that litigants can invoke in a proceeding to recognize foreign country money judgments (“foreign judgments”), while also significantly expanding the defenses to recognition and enforcement of foreign judgments available to defendants in New York. In particular, the substantive changes seek to ensure that the New York courts only recognize foreign judgments that have been procured through a fair and impartial process.

I. Overview of Recognition of Foreign Judgments in the United States

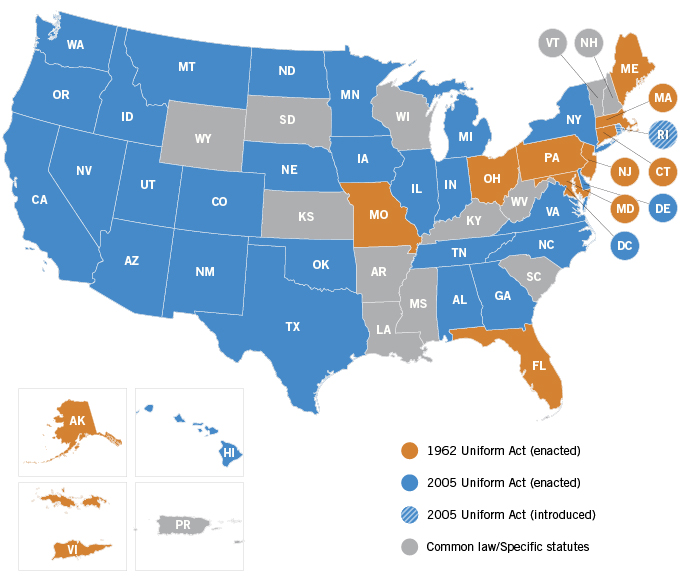

There is no federal law governing recognition of foreign judgments in the United States. However, the rules are broadly similar across all 50 U.S. states and the District of Columbia, providing for recognition of foreign judgments that are final, conclusive, and enforceable where rendered. Over the last 60 years, a majority of U.S. states have codified their rules on recognition, following initially the Uniform Foreign Money Judgments Recognition Act of 1962 (the “1962 Uniform Act”) or now increasingly the Uniform Foreign-Country Money Judgments Recognition Act of 2005 (the “2005 Uniform Act”).

The 1962 Uniform Act was designed to increase the predictability and stability in this area of the law, facilitate international commercial transactions, and encourage foreign courts to recognize U.S. judgments.[3] Notably, the 1962 Uniform Act did not prescribe any enforcement procedure, providing instead that a foreign judgment, once domesticated, is enforceable in the same manner as the judgment of a court of a sister U.S. state, which is entitled to full faith and credit. That is still the prevailing rule today.

The 1962 Uniform Act defined certain threshold requirements for recognition and outlined certain mandatory and discretionary grounds for non-recognition. For example, the recognizing U.S. court was directed to consider, inter alia, whether the judgment was rendered under a judicial system that provides for impartial tribunals and procedures compatible with due process; whether the foreign court had personal and subject matter jurisdiction; whether the defendant received sufficient notice of the proceedings to mount a defense; whether the judgment was obtained by fraud; and whether the cause of action or claim for relief on which the judgment is based is repugnant to the public policy of the recognizing state.

In 2005, the Uniform Law Commission issued the 2005 Uniform Act.[4] Its purpose was to update and clarify the 1962 Uniform Act and “to correct problems created by the interpretation of the provisions of that Act by the courts over the years since its promulgation” while maintaining “the basic rules or approach.”[5] In particular, the 2005 Uniform Act created new discretionary bases for non-recognition, updated and clarified the definitions section, clarified the procedure for seeking (and resisting) recognition of a foreign judgment, expressly allocated the burden of proof, and established a statute of limitations for recognition actions.[6]

Since 2007, a growing number of U.S. states have enacted the modernized 2005 Uniform Act (see map below). As of June 2021, 27 states and the District of Columbia have adopted the 2005 Uniform Act, while one state has introduced this legislation.[7] Another 11 states and the U.S. Virgin Islands currently still apply the 1962 Uniform Act.[8] In the remaining 12 states, the recognition of judgments remains primarily a matter of common law or unique statutory provisions.

Law on Recognition of Foreign Judgments in the United States

Data Source: Uniform Law Commission

II. Overview of Recognition of Foreign Judgments in New York

New York adopted the 1962 Uniform Act as CPLR Article 53 in 1970. Traditionally in New York, once the judgment creditor had made the initial showing that the foreign judgment falls within the scope of New York’s recognition statute, the judgment debtor had to establish a basis for non-recognition if it wished to avoid recognition. As in most U.S. states, New York’s 1970 Recognition Act set out both mandatory grounds for non-recognition—under which the court is prohibited from granting recognition—and discretionary bases on which a court may decline recognition.

With the enactment of the 2021 Recognition Act, New York largely leaves intact the legal framework established by the 1970 Recognition Act while adopting the key updates from the 2005 Uniform Law:

- New Proceeding-Specific Discretionary Criteria. There are two new discretionary criteria for non-recognition, providing that a court may decline recognition where (i) “the judgment was rendered in circumstances that raise substantial doubt about the integrity of the rendering courts with respect to the judgment,”[9] or (ii) “the specific proceeding in the foreign court leading to the judgment was not compatible with the requirement of due process of law.”[10] These two new grounds are significant because they are proceeding-specific—i.e., the judgment debtor can challenge recognition based on a lack of due process or impartial tribunals in the specific proceedings that gave rise to the foreign judgment, regardless of the fairness or procedural safeguards available in the foreign country’s judicial system overall. Under the 1970 Recognition Act, by contrast, complaints about the particular proceeding against the judgment debtor were generally insufficient. To avoid recognition, by statute, a judgment debtor had to establish that the foreign country’s judicial system as a whole lacked impartial tribunals or due process—a high bar in state courts that may be loath to condemn the entire judicial system of a foreign country. Nonetheless, as the Uniform Law Commission noted in its letter of support of the bill, a number of U.S. courts applying the 1962 Uniform Act were either ignoring the “system” language in the governing statute or else “stretching” that language to import proceeding-specific considerations.[11] Such interpretative issues were sufficiently significant to warrant the Uniform Law Commission’s revision of the 1962 Uniform Act.[12]

- Updated Grounds for Non-Recognition. The 2021 Recognition Act also expands the mandatory and discretionary grounds for non-recognition available to a judgment debtor seeking to resist recognition. For example, whereas a lack of subject matter jurisdiction was a discretionary basis for non-recognition under the 1970 Recognition Act, it is mandatory under the 2021 Recognition Act, meaning that a New York court must refuse recognition where the foreign court lacked subject matter jurisdiction over the underlying dispute.[13] Further, the 2021 Recognition Act expands the scope of the (discretionary) public policy non-recognition ground, providing that a court may consider either whether the foreign judgment or the cause of action on which the judgment is based is “repugnant to the public policy of New York or of the United States.”[14] Under the 1970 Recognition Act, this ground was limited to cases where the underlying cause of action—and not the foreign judgment itself—was repugnant to New York’s public policy.

- Burden of Proof. The 2021 Recognition Act clarifies and makes explicit that the party seeking recognition of a foreign judgment bears the burden of establishing that the judgment is subject to the act,[15] while the party resisting recognition has the burden of establishing that a specific ground for non-recognition applies.[16]

- Procedure. The Act clarifies that when recognition is sought as an original matter, the party seeking recognition must file an action on the judgment (or a motion for summary judgment in lieu of complaint) to obtain recognition,[17] but when recognition is sought in a pending action, it may be filed as a counter-claim, cross-claim, or affirmative defense.[18]

- Statute of Limitations. The 2021 Recognition Act establishes a limitations period, providing that a New York court may only enforce a foreign judgment that is still “effective in the foreign country.”[19] If there is no limitation on enforcement in the country of origin, recognition must be sought within 20 years of the date that the judgment became effective in the foreign country.[20]

As with the 1970 Recognition Act, the 2021 Recognition Act applies to any foreign judgment that is “final, conclusive and enforceable” where rendered.[21] It does not apply to a foreign judgment for taxes, a fine or penalty, and it further clarifies that it does not apply to a “judgment for divorce, support or maintenance, or other judgment rendered in connection with domestic relations.”[22] Within those defined limits, the 2021 Recognition Act will apply to all recognition actions commenced on or after the effective date of the act (i.e., June 11, 2021)[23] even if the relevant transactions or proceedings in the foreign country took place before then.

III. Implications of New York’s 2021 Recognition Act

As noted above, the 2021 Recognition Act provides certain definitional, procedural, and substantive changes that will impact judgment creditors and debtors litigating recognition in New York courts.

Many of these revisions will benefit both parties by providing greater clarity and precision about the procedural mechanisms and substantive arguments they can plausibly invoke in a recognition proceeding. Some of the revisions, like the statute of limitations, reduce the incentive to forum-shop where foreign law provides for a shorter effectiveness period than New York law.

The most immediate effect of the 2021 Recognition Act will be felt on the scope and complexity of litigation. As the Sponsor Memo noted, the 2021 Recognition Act “revises the grounds for denying recognition of foreign country money judgements to better reflect the even more varied forms of judicial process on the modern global stage.”[24] Notably, the 2021 Recognition Act will permit judgment debtors to challenge foreign judgments based on proceeding-specific concerns so as to ensure the foreign judgment being recognized has adhered to fundamental principles of due process that the New York courts have a vested interest in protecting. This was previously more difficult to do where only systemic (as opposed to proceeding-specific) due process considerations could be considered in denying recognition.[25] The inclusion of proceeding-specific grounds, which will inevitably expand the range of arguments a judgment debtor can now raise, will likely increase the number of foreign judgments denied recognition in New York courts.

These additional defenses will require greater sophistication by both judgment creditors and debtors in recognition actions in terms of what kinds of foreign legal and expert evidence to marshal. At the same time, these defenses give the New York courts additional bases to ensure that they only recognize judgments that result from a fair and impartial proceeding.

______________________________

[1] The bill was signed into law (Chapter 127) on June 11, 2021. See Senate Bill S523A, N.Y. State Senate (last visited June 21, 2021), https://www.nysenate.gov/legislation/bills/2021/s523.

[2] S.B. S523A (N.Y. 2021) (“An act to amend [New York’s] civil practice law and rules, in relation to revising and clarifying the uniform foreign country money-judgments recognition act.”).

[3] See Uniform Law Comm’n, Uniform Foreign Money-Judgments Recognition Act (with Prefatory Note and Comments) (1962).

[4] See Uniform Law Comm’n, Uniform Foreign-Country Money Judgments Recognition Act (with Prefatory Note and Comments) (2005).

[5] Id., Prefatory Note, at 1.

[7] Foreign-Country Money Judgments Recognition Act 2005, Uniform Law Comm’n (last visited June 22, 2021), https://www.uniformlaws.org/committees/community-home?CommunityKey=ae280c30-094a-4d8f-b722-8dcd614a8f3e.

[8] Foreign-Country Money Judgments Recognition Act 1962, Uniform Law Comm’n (last visited June 22, 2021), https://www.uniformlaws.org/committees/community-home?CommunityKey=9c11b007-83b2-4bf2-a08e-74f642c840bc.

[9] N.Y. CPLR § 5304(a)(7) (McKinney 2021).

[11] See Letter from the Uniform Law Commission to the Chairmen of the New York Assembly Judiciary Committee, dated March 11, 2021, at 2.

[13] N.Y. CPLR § 5304(a)(3) (McKinney 2021).

[24] Sponsor’s Mem., S.B. S523A (N.Y. 2021), https://www.nysenate.gov/legislation/bills/2021/s523.

[25] See, e.g., Shanghai Yongrun Inv. Management Co., Ltd. v. Kashi Galaxy Venture Capital Co., Ltd., No. 156328/2020, 2021 WL 1716424 (N.Y. Sup. Ct. Apr. 30, 2021); Chevron Corp. v. Donziger, 974 F. Supp. 2d 362 (S.D.N.Y. 2014), aff’d, 833 F.3d 74 (2d Cir. 2016); Bridgeway Corp. v. Citibank, 45 F. Supp. 2d 276 (S.D.N.Y. 1999), aff’d, 201 F.3d 134 (2d Cir. 2000). See also Osorio v. Dole Food Co., 665 F. Supp. 2d 1307 (S.D. Fla. 2009), aff’d sub nom. Osorio v. Dow Chem. Co., 635 F.3d 1277 (11th Cir. 2011); Bank Melli Iran v. Pahlavi, 58 F.3d 1406 (9th Cir. 1995).

The following Gibson Dunn lawyers prepared this client alert: Rahim Moloo, Lindsey D. Schmidt, Maria L. Banda, and Peter M. Wade.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding these issues. Please contact the Gibson Dunn lawyer with whom you usually work, any member of the firm’s International Arbitration, Judgment and Arbitral Award Enforcement or Transnational Litigation practice groups, or the following:

Rahim Moloo – New York (+1 212-351-2413, rmoloo@gibsondunn.com)

Lindsey D. Schmidt – New York (+1 212-351-5395, lschmidt@gibsondunn.com)

Anne M. Champion – New York (+1 212-351-5361, achampion@gibsondunn.com)

Maria L. Banda – Washington, D.C. (+1 202-887-3678, mbanda@gibsondunn.com)

Please also feel free to contact the following practice group leaders:

International Arbitration Group:

Cyrus Benson – London (+44 (0) 20 7071 4239, cbenson@gibsondunn.com)

Penny Madden QC – London (+44 (0) 20 7071 4226, pmadden@gibsondunn.com)

Judgment and Arbitral Award Enforcement Group:

Matthew D. McGill – Washington, D.C. (+1 202-887-3680, mmcgill@gibsondunn.com)

Robert L. Weigel – New York (+1 212-351-3845, rweigel@gibsondunn.com)

Transnational Litigation Group:

Susy Bullock – London (+44 (0) 20 7071 4283, sbullock@gibsondunn.com)

Perlette Michèle Jura – Los Angeles (+1 213-229-7121, pjura@gibsondunn.com)

Andrea E. Neuman – New York (+1 212-351-3883, aneuman@gibsondunn.com)

William E. Thomson – Los Angeles (+1 213-229-7891, wthomson@gibsondunn.com)

© 2021 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.

Decided June 21, 2021

United States v. Arthrex, Inc., No. 19-1434; Smith & Nephew, Inc. v. Arthrex, Inc., No. 19-1452; Arthrex, Inc. v. Smith & Nephew, Inc., No. 19-1458

Today, the Supreme Court held 5-4 that the absence of Executive Branch review of decisions rendered by Administrative Patent Judges (APJs) of the Patent Trial and Appeal Board (PTAB) violates the Appointments Clause, and that the proper remedy is to sever a statutory provision so that the Director of the Patent and Trademark Office may review PTAB decisions.

Background:

The Constitution’s Appointments Clause, art. II, § 2, cl. 2, requires principal Officers of the United States to be appointed by the President with the advice and consent of the Senate, but permits inferior Officers to be appointed by a department head such as the Secretary of Commerce. Under the Patent Act, the Secretary appoints APJs to preside over adjudicatory proceedings such as inter partes review (IPR) and may fire them for cause. The Director of the Patent and Trademark Office supervises APJs in various ways, but cannot unilaterally review their patentability decisions. Smith & Nephew petitioned for IPR of Arthrex’s patent claims and a panel of APJs decided the claims were unpatentable. On appeal, Arthrex argued that APJs are unconstitutionally appointed principal Officers because they are insufficiently supervised by others. The Federal Circuit agreed that APJs’ appointment violated the Appointments Clause. As a remedy, it severed APJs’ for-cause removal protections to render them inferior Officers, and remanded Arthrex’s IPR to a new panel of APJs.

Issue:

Does the Appointments Clause require administrative review of PTAB decisions?

Court’s Holding:

Yes. The Appointments Clause does not permit APJs to exercise executive power unreviewed by any Executive Branch official. Accordingly, the Director has the authority to unilaterally review any PTAB decision, and a contrary statutory provision (35 U.S.C. § 6(c)) is unenforceable as applied to the Director.

“The structure of the PTO and the governing constitutional principles chart a clear course: decisions by APJs must be subject to review by the director.”

Chief Justice Roberts, writing for the majority

Gibson Dunn represented the petitioners: Smith & Nephew, Inc. and ArthroCare Corp.

What It Means:

- The Court’s 5-4 decision holding that the Patent Act provided for constitutionally inadequate supervision of APJs may make it easier for future challengers to raise Appointments Clause objections to other administrative adjudicators.

- By a 7-2 vote, the Court rejected calls by critics of the PTAB to invalidate the entire system. Although the Court’s decision allows the PTAB to continue operating, the Director now will be able to review final PTAB decisions and, upon review, may issue decisions on behalf of the Board.

- The Court clarified that its opinion concerns only the Director’s ability to supervise APJs in adjudicating petitions for IPR. The opinion does not address the Director’s supervision over other PTAB adjudications, such as the examination process.

- The Court held that because “the source of the constitutional violation is the restraint on the review authority of the Director, rather than the appointment of APJs by the Secretary,” the appropriate remedy is a limited remand to the Acting Director to decide whether to rehear Smith & Nephew’s IPR petition, rather than a hearing before a new panel of APJs.

The Court’s opinion is available here.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding developments at the Supreme Court. Please feel free to contact the following practice leaders:

Appellate and Constitutional Law Practice

| Allyson N. Ho +1 214.698.3233 aho@gibsondunn.com | Mark A. Perry +1 202.887.3667 mperry@gibsondunn.com | Lucas C. Townsend +1 202.887.3731 ltownsend@gibsondunn.com |

| Bradley J. Hamburger +1 213.229.7658 bhamburger@gibsondunn.com |

Related Practice: Intellectual Property

| Kate Dominguez +1 212.351.2338 kdominguez@gibsondunn.com | Y. Ernest Hsin +1 415.393.8224 ehsin@gibsondunn.com | Josh Krevitt – New York +1 212.351.4000 jkrevitt@gibsondunn.com |

| Jane M. Love, Ph.D. +1 212.351.3922 jlove@gibsondunn.com |

Decided June 21, 2021

Nat’l Collegiate Athletic Ass’n v. Alston, No. 20-512; and Am. Athletic Conf. v. Alston, No. 20-520

Today, the Supreme Court unanimously held that the NCAA’s current limits on education-related benefits for student-athletes violate the Sherman Act.

Background:

The NCAA imposes eligibility rules fixing the compensation and benefits that member schools can offer student-athletes. The NCAA maintains that its rules, including its restrictions on certain education-related benefits, are necessary to preserve amateurism in college athletics, which is what distinguishes its product from professional sports.

Several student-athletes brought class-action suits against the NCAA and its member conferences, arguing that the restrictions on compensation and benefits run afoul of the Sherman Act. After a bench trial, the district court enjoined the NCAA’s restrictions on education-related benefits after ruling that they violated the Sherman Act. The court ordered the NCAA to allow its member schools to offer athletes education-related benefits such as academic incentive awards and paid, post-eligibility internships. The court did not, however, enjoin NCAA rules that restrict benefits unrelated to education.

The Ninth Circuit affirmed, holding that the NCAA’s limits on education-related benefits violate the Sherman Act, and that allowing student-athletes to receive certain education-related benefits beyond the cost of college attendance, such as paid post-eligibility internships, would not eliminate the distinction between college athletics and professional sports.

Issue:

Whether the NCAA’s restrictions on education-related benefits for student-athletes violate the Sherman Act.

Court’s Holding:

Yes. The NCAA’s restrictions on education-related benefits violate Section 1 of the Sherman Act. Substantially less restrictive rules that permit student-athletes to receive certain limited education-related benefits would adequately preserve the distinction between college athletics and professional sports.

The district court’s injunction “does not float on a sea of doubt but stands on firm ground—an exhaustive factual record, a thoughtful legal analysis consistent with established antitrust principles, and a healthy dose of judicial humility.”

Justice Gorsuch, writing for the Court

Gibson Dunn submitted an amicus brief on behalf of the Players Associations of the NFL, NBA, WNBA, and National Women’s Soccer League, and the National Collegiate Players Association, in support of respondents: Shawne Alston, et al.

What It Means:

- Today’s decision rejects the NCAA’s argument that it is effectively immune from antitrust scrutiny because its rules should receive abbreviated, deferential review, and instead holds that the NCAA’s restrictions are subject to review under the “rule of reason.”

- The Court confirmed that antitrust law does not require businesses “to use anything like the least restrictive means of achieving legitimate business purposes,” but upheld the district court’s conclusion that restrictions on education-related benefits were not necessary to preserve consumer demand for college athletics, in light of the record evidence establishing that the immense popularity of college sports is largely unrelated to education-related benefits paid to student-athletes and given the existence of substantially less restrictive alternatives.

- The Court’s decision permits student-athletes to receive a variety of education-related benefits that go beyond the cost of college attendance, such as academic and graduation incentive awards, graduate-school scholarships, and paid, post-eligibility internships. That said, there is nothing that requires member schools to offer such benefits, nor are individual conferences prohibited from imposing their own restrictions.

- The continued viability of the NCAA’s restrictions on benefits unrelated to education remains an open question. The student-athletes did not press their challenge to these rules—which the Ninth Circuit upheld—before the Court. Justice Kavanaugh wrote a separate concurrence “to underscore” his view that those rules “raise serious questions under the antitrust laws.” He indicated that the NCAA may lack a valid procompetitive justification for its remaining compensation rules because its argument—“that colleges may decline to pay student athletes because the defining feature of college sports . . . is that the student athletes are not paid”—“is circular and unpersuasive.”

- Nothing in the Court’s decision prevents states or Congress from devising different rules to govern the compensation and benefits available to college athletes. Many states have adopted or are considering proposals to loosen restrictions on such benefits. Congress is considering similar proposals, as well as a bill, the “Fairness in Collegiate Athletics Act” (S. 4004), which would arguably give the NCAA the antitrust immunity it sought in this case.

The Court’s opinion is available here.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding developments at the Supreme Court. Please feel free to contact the following practice leaders:

Appellate and Constitutional Law Practice

| Allyson N. Ho +1 214.698.3233 aho@gibsondunn.com | Mark A. Perry +1 202.887.3667 mperry@gibsondunn.com | Lucas C. Townsend +1 202.887.3731 ltownsend@gibsondunn.com |

| Bradley J. Hamburger +1 213.229.7658 bhamburger@gibsondunn.com | Kristen C. Limarzi +1 202.887.3518 klimarzi@gibsondunn.com |

Related Practice: Antitrust and Competition

| Rachel S. Brass +1 415.393.8293 rbrass@gibsondunn.com | Stephen Weissman +1 202.955.8678 sweissman@gibsondunn.com |

Related Practice: Sports Law

| Richard J. Birns +1 212.351.4032 rbirns@gibsondunn.com | Maurice M. Suh +1 213.229.7260 msuh@gibsondunn.com |

Decided June 21, 2021

Goldman Sachs Group Inc. v. Arkansas Teacher Retirement System, No. 20-222

Today, the Supreme Court held 8-1 that the Second Circuit must clarify its reasoning in its certification of a securities class action against Goldman Sachs, and held 6-3 that the defendant bears the burden of persuasion when attempting to rebut the “fraud on the market” presumption.

Background:

Goldman Sachs was sued under the securities laws for making statements suggesting that it did not have any conflicts of interest in the management of its mortgage business. The plaintiffs sought to certify a class of investors in Goldman stock and invoked the “fraud on the market” presumption, recognized in Basic Inc. v. Levinson, 485 U.S. 224 (1988), to show that every class member relied on Goldman’s alleged misrepresentations in buying or selling at the market price. Goldman tried to rebut this presumption of reliance by pointing to the generic nature of its challenged statements (e.g., “Integrity and honesty are at the heart of our business”). As Goldman saw it, no investors could have truly relied on such statements in buying their shares because the statements were too generic to impact the stock’s price. The district court rejected that argument and certified the class.

The Second Circuit initially reversed the class-certification order and remanded, after which the district court recertified the class; the Second Circuit then affirmed that second certification order. The Second Circuit held that the generic nature of the statements was irrelevant at the class-certification stage, and instead should be litigated at trial.

Issues:

Can a defendant in a securities class action rebut the presumption of classwide reliance recognized in Basic by arguing that the statements were too generic to have had any impact on the price of the security?

Does a defendant seeking to rebut the Basic presumption with evidence of a lack of price impact bear only the burden of production or also the ultimate burden of persuasion?

Court’s Holdings:

A court should consider the generic nature of the statements at the class certification stage, and the Second Circuit must clarify on remand whether it in fact did so here.

The defendant bears the ultimate burden of persuasion when attempting to rebut the Basic presumption.

“The generic nature of a misrepresentation often will be important evidence of a lack of price impact, particularly in cases proceeding under the inflation maintenance theory.”

Justice Barrett, writing for the Court

What It Means:

- Today’s decision is the first time the Supreme Court has discussed the “inflation-maintenance” theory of securities fraud, although the Court expressly noted that it was taking no view on the “validity” or “ contours” of that theory. Under the inflation-maintenance theory, a misrepresentation causes a stock price to remain inflated by preventing inflation from dissipating from the price. The theory, which has become increasingly common in securities class actions, often depends on an inference that a negative disclosure about the company corrected an earlier misrepresentation, and that a drop in the stock price associated with the disclosure is equal to the amount of inflation maintained by the earlier misrepresentation.

- The Court’s decision suggests important limitations on the theory. The Court explained that the inference that the back-end price drop equals front-end inflation “starts to break down when there is a mismatch between the contents of the misrepresentation and the corrective disclosure,” and this occurs “when the earlier misrepresentation is generic . . . and the later corrective disclosure is specific.”

- The decision thus holds that defendants in securities class action suits may rebut the Basic presumption by arguing that the allegedly fraudulent statements are too generic to have impacted the price of the security, even if those arguments overlap with the ultimate merits of the case.

- The Court also clarified that its prior decisions in Basic and Erica P. John Fund, Inc. v. Halliburton Co., 563 U. S. 804, 813 (2011), established that securities-fraud defendants bear the ultimate burden of persuading the court that the Basic presumption does not apply. The Court’s decision thus underscores the importance of defendants offering factual and expert evidence at the class certification stage to rebut the Basic presumption.

The Court’s opinion is available here.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding developments at the Supreme Court. Please feel free to contact the following practice leaders:

Appellate and Constitutional Law Practice

| Allyson N. Ho +1 214.698.3233 aho@gibsondunn.com | Mark A. Perry +1 202.887.3667 mperry@gibsondunn.com | Lucas C. Townsend +1 202.887.3731 ltownsend@gibsondunn.com |

| Bradley J. Hamburger +1 213.229.7658 bhamburger@gibsondunn.com |

Securities Litigation Practice

| Monica K. Loseman +1 303.298.5784 mloseman@gibsondunn.com | Brian M. Lutz +1 415.393.8379 blutz@gibsondunn.com | Craig Varnen +1 213.229.7922 cvarnen@gibsondunn.com |

On June 11, 2021, the Securities and Exchange Commission released Chair Gary Gensler’s Spring 2021 Unified Agenda of Regulatory and Deregulatory Actions (the “Reg Flex Agenda”). This agenda reflects Chair Gensler’s willingness to reopen and perhaps even undo certain rulemakings that were completed in the last two years of former Chair Jay Clayton’s leadership and adopted by the Commission over the dissent of the Democrat Commissioners. Shortly after the Reg Flex Agenda was issued, Republican Commissioners Hester Peirce and Elad Roisman issued a public statement criticizing Chair Gensler for “reopening large swathes of work that was just completed without new evidence to warrant reopening” and thereby, in their view, “undermin[ing] the Commission’s reputation as a steady regulatory hand.”[1]

In this Client Alert, we summarize the key and noteworthy aspects of the Reg Flex Agenda that potentially impact public companies. It should be noted that the items listed in the agenda reflect only the priorities of Chair Gensler and do not necessarily reflect the views and priorities of any other Commissioner. In addition, the agenda does not contain much substantive information, only a brief “abstract” describing each rulemaking item. Nevertheless, just the appearance of an item on the agenda can be informative.[2]

As the Gensler Commission begins to appoint senior staff and to implement this agenda, it will be important for public companies and market participants to pay attention to the development and execution of Gensler’s agenda. While no one expected the Gensler Commission to continue Clayton’s policy initiatives, at the same time, the extent to which Chair Gensler appears willing to undo or unwind the Clayton Commission’s previously adopted rulemakings is surprising, in part because, as a general matter, the SEC Staff tasked with doing the actual work of drafting the releases do not change. What Gensler’s Reg Flex Agenda makes clear is that rulemakings that were adopted exclusively along party-line votes are particularly vulnerable to being “revisited,” and the roadmap for any future actions can be discerned from past dissenting statements the Democrat Commissioners issued when the rules were adopted.[3]

Proxy Reform

On June 1, 2021, Chair Gensler issued a public statement in which he directed the Division of Corporation Finance to revisit the Commission’s recent amendments regarding the application of the proxy rules to proxy advisory firms.[4] These amendments, adopted in July 2020, codified the Commission’s view (which has also been the Staff’s longstanding view) that proxy voting advice generally constitutes a “solicitation” as defined in Exchange Act Rule 14a-1; added new conditions to the exemptions in Rule 14a-2(b)(9) from the proxy rules’ information and filing requirements that are used by proxy advisory firms; and amended the Note to Rule 14a-9 to include specific examples of material misstatements or omissions related to proxy voting advice. These rule amendments took effect on November 2, 2020, and the proxy advisory firms are required to comply with the new conditions as of December 1, 2021.

Consistent with Chair Gensler’s June 1 statement, the Reg Flex Agenda lists “Proxy Voting Advice” as a new item and indicates that it is at the “proposed rule stage” as opposed to the “prerule stage.”[5] In addition, also on June 1, 2021, the Division announced that it would not enforce the Commission’s 2019 interpretation and guidance or the 2020 rule amendments during the period in which the Commission is considering further regulatory action in this area.[6] This development does not affect the ability of private parties to file suit under the proxy rules, as amended; and the parties subject to the rule amendments technically must continue to comply with the provisions that have become effective.

The agenda also includes “Rule 14a-8 Amendments” as a new item in the “proposed rule stage,” thereby putting into question whether the September 2020 amendments to the procedural requirements and resubmission thresholds in Rule 14a-8 will remain in effect by the time of the peak 2021/2022 shareholder proposal season.[7] Although they became effective on January 4, 2021, the September 2020 amendments only apply to proposals submitted for an annual or special meeting to be held on or after January 1, 2022, and there is an even longer transition period for the new share ownership thresholds, which need not be satisfied for meetings held before January 1, 2023.

The Reg Flex Agenda continues to list “Universal Proxy” as a “final rule stage” item, which is the last step in the rulemaking process in which the Commission responds to public comment on the proposed rule and makes appropriate revisions before publishing the final rule in the Federal Register. Although the proposing release for this rulemaking was issued in October 2016 under Chair Mary Jo White’s leadership, it was first included in Chair Clayton’s Reg Flex Agenda in Spring 2020.

Exempt Offerings

One of the last rulemaking projects completed by the Clayton Commission was amending the accredited investor definition in August 2020[8] and simplifying the Securities Act integration framework in November 2020, as part of a larger effort to harmonize the exempt offering framework.[9]

Given the scope of these amendments, it was not generally expected that exempt offerings would be a priority for the Gensler Commission. Nevertheless, the Reg Flex Agenda lists “Exempt Offerings” as a new “prerule stage” item and describes the rulemaking project with greater specificity as compared to other items, as follows:

“The Division is considering recommending that the Commission seek public comment on ways to further update the Commission’s rules related to exempt offerings to more effectively promote investor protection, including updating the financial thresholds in the accredited investor definition, ensuring appropriate access to and enhancing the information available regarding Regulation D offerings, and amendments related to the integration framework for registered and exempt offerings.”

ESG Disclosure

As expected, the Reg Flex Agenda lists a number of items relating to Environmental/Social/Governance disclosures, all of which are “proposed rule stage” items:[10]

- “Climate Change Disclosure” – whether to “propose rule amendments to enhance registrant disclosures regarding issuers’ climate-related risks and opportunities”;[11]

- “Human Capital Management Disclosure” – whether to “propose rule amendments to enhance registrant disclosures regarding human capital management”;

- “Cybersecurity Risk Governance” – whether to “propose rule amendments to enhance issuer disclosures regarding cybersecurity risk governance”; and

- “Corporate Board Diversity” – whether to “propose rule amendments to enhance registrant disclosures about the diversity of board members and nominees.”

On March 15, 2021, then-Acting Chair Allison Herren Lee solicited public input on climate change disclosures by publishing 15 questions for comment.[12] The informal comment period for this solicitation of input ended on June 13, 2021.

Rule 10b5-1 Plans and Share Buybacks

As early as 2007, then-Director of Enforcement Linda Chatman Thomsen gave a speech in which she expressed concern about possible abuse of Rule 10b5-1 plans, which were first authorized in 2000.[13] She noted that “[r]ecent academic studies suggest that Rule 10b5-1 may be being abused. The academic data shows that executives who trade within a 10b5-1 plan outperform their peers who trade outside of a plan by nearly 6%.” As a result, “[t]his raises the possibility that plans are being abused essentially to facilitate trading on inside information. So we’re looking…. If executives are in fact trading on inside information and using a plan for cover, the plan will provide no defense.”

Although the Commission has brought only a handful of enforcement actions involving the alleged abuse of a Rule 10b5-1 plan,[14] Chair Gensler recently stated that, “[i]n my view, these plans have led to real cracks. Thus, I’ve asked staff to make recommendations for the Commission’s consideration on how we might freshen up Rule 10b5-1.”[15] Gensler cited four areas of concern. First, there is no cooling off period required before an insider can make his or her first trade under the plan. He noted that cooling-off periods of four to six months have received bipartisan support. Second, he noted that there is currently no limitation on when Rule 10b5-1 plans can be cancelled. In his view, “canceling a plan may be as economically significant as carrying out an actual transaction.” Third, there are no mandatory disclosure requirements regarding Rule 10b5-1 plans. Fourth, there are no limits on the number of 10b5-1 plans that insiders can adopt. Finally, Gensler noted that he is interested in Rule 10b5-1’s “intersection with share buybacks.”

Consistent with these statements, the Reg Flex Agenda lists “Rule 10b5-1” as a new “proposed rule stage” item regarding whether to “propose amendments to address concerns about the use of the affirmative defense provisions of Exchange Act Rule 10b5-1.” The agenda also lists “Share Repurchases Disclosure Modernization” as a new “proposed rule stage” item regarding whether to “propose amendments to modernize disclosure of share repurchases, including Item 703 of Regulation S-K.” Currently, share repurchase information (total number of shares purchased each month and the average price paid per share for that month) is required to be included in periodic reports, with footnote disclosure indicating whether purchases have been made pursuant to publicly announced plans or programs or outside of any such plans or programs.

Beneficial Ownership Reporting and Swaps

The Reg Flex Agenda notes that the Division is “considering recommending that the Commission propose amendments to enhance market transparency, including disclosure related beneficial ownership or interests in security-based swaps.” This new “proposed rule stage” item is likely related to the recent blow-up at Archegos Capital, a family office with extensive security-based swap and derivative positions that resulted in significant losses at several major investment banks.[16] The magnitude of the losses emanating from this unregulated entity attracted much attention among legislators and the Commission, so it comes as no surprise that the Commission is considering whether to propose new rules seeking to enhance the transparency of significant holdings of swaps by market participants. What is surprising is the absence of any mention of rulemaking that would potentially accelerate the current 10-calendar day deadline for filing initial Schedule 13D beneficial ownership reports – a generous filing deadline that has been of keen interest to public companies, legal practitioners, market participants and academics alike for decades.[17]

SPACs

Given the recent and significant volume of SPAC filings, it is not surprising that the Reg Flex Agenda lists, as a new “proposed rule stage” item, “Special Purpose Acquisition Companies.” As the abstract indicates only that the Division is considering whether to recommend that the Commission propose rule amendments “related to special purpose acquisition companies,” it is not possible to discern the nature or objective of this rulemaking project based on the Reg Flex Agenda.

Dodd-Frank Items Added Back to the Reg Flex Agenda

The Fall 2020 Reg Flex Agenda, the last one issued under the Clayton Commission, did not include certain Dodd-Frank-mandated rulemakings; these have now been added back to the Spring 2021 Reg Flex Agenda. Specifically, these are “Listing Standards for Recovery of Erroneously Awarded Compensation,” which is to implement Section 954 of Dodd-Frank and is now in the “proposed rule stage” (i.e., it is being reproposed); “Incentive-Based Compensation Arrangements,” which is to implement Section 956 of Dodd-Frank and is also being reproposed; and “Pay Versus Performance,” which is to implement Section 953(a) of Dodd-Frank and is listed (alarmingly, given the critical comments that were submitted on the initial rule proposal) as a “final rule stage” item.

Dropped from the Reg Flex Agenda

In July 2018, the Commission published a concept release on “Compensatory Securities Offerings and Sales,” which solicited comment on Securities Act Rule 701, which exempts from registration offers and sales of securities issued by non-reporting companies pursuant to compensatory arrangements, as well as on Form S-8, which is the registration statement for compensatory offerings by reporting companies. Noting that “[s]ignificant evolution has taken place both in the types of compensatory offerings issuers make and the composition of the workforce since the Commission last substantively amended these regulation,” the Commission sought comment on “possible ways to modernize the exemption and the relationship between and Form S-8, consistent with investor attention.”

This concept release then served as the basis for an item in the Fall 2020 Reg Flex Agenda, “Amendments to Rule 701/Form S-8.” Also listed in the Fall 2020 Reg Flex Agenda was a new “proposed rule stage” item, “Temporary Rules to Include Certain ‘Platform Workers’ in Compensatory Offerings Under Rule 701 and Form S-8,” which Commissioners Peirce and Roisman described in their June 14, 2021 statement as “allow[ing] companies to compensate gig workers with equity.” Both of these items have been dropped from the Spring 2021 Reg Flex Agenda.

Conclusion

Not unlike what is happening elsewhere in the Executive Branch, it now appears that part of the agenda of the Gensler Commission will be undoing the work of the Trump Administration. In particular, in the last year of the Clayton Commission, many significant rulemakings were adopted over the dissent of the Democrat Commissioners. Rereading now the “Statement on Departure of Chairman Jay Clayton” by Commissioners Allison Herren Lee and Caroline A. Crenshaw, their use of the possessive pronoun takes on more meaning: “In addition to advancing his policy priorities, Chairman Clayton has led the agency through difficult times for the markets and our staff” (emphasis added).[18]

________________________

[1] Commissioner Hester M. Peirce and Commissioner Elad L. Roisman, “Moving Forward or Falling Back? Statement on Chair Gensler’s Regulatory Agenda,” June 14, 2021, available at: https://www.sec.gov/news/public-statement/moving-forward-or-falling-back-statement-chair-genslers-regulatory-agenda.

[2] It should also be noted that the requirement to provide a bi-annual reg flex agenda stems from the Regulatory Flexibility Act, which was enacted in 1980 to require agencies to consider the impact of their rules on small entities and to consider less burdensome alternatives. A reg flex agenda provides notice to the public about what future rulemaking is under consideration and is not binding upon an agency in any way.

[3] In a June 17, 2021 newsletter, the Council of Institutional Investors (CII) stated, “The SEC on June 11 released a Spring 2021 rulemaking agenda that closely aligns with most of the priorities that CII set out for this year.”

[4] Chair Gary Gensler, “Statement on the application of the proxy rules to proxy voting advice,” June 1, 2021, available at: https://www.sec.gov/news/public-statement/gensler-proxy-2021-06-01. Chair Gensler’s statement also referred to the Commission’s guidance and interpretation issued in 2019 relating to proxy advisory firms, which have effectively been superseded by the 2020 rule amendments. This guidance and interpretation addressed two questions: first, whether proxy voting advice constitutes a “solicitation”; and second, whether proxy voting advice is subject to the antifraud rule, Exchange Act Rule 14a-9. In October 2019, Institutional Shareholder Services, Inc. filed suit in the U.S. District Court for the District of Columbia to challenge the 2019 interpretation and guidance. On June 1, 2021, the Commission filed an unopposed motion to hold the case in abeyance, noting that “[f]urther regulatory action on the items Chair Gensler has directed staff to consider revisiting could substantially narrow or moot some or all of ISS’s claims.”

[5] A “prerule” means that the Commission will solicit public comment on whether or not, or how best, to initiate a rulemaking. In contrast, a “proposed rule” means that the Commission is at the stage in which it will propose to add to or change its existing regulations and will solicit public comment on a rule proposal.

[6] Division of Corporation Finance, “Statement on Compliance with the Commission’s 2019 Interpretation and Guidance Regarding the Applicability of the Proxy Rules to Proxy Voting Advice and Amended Rules 14a-1(1), 14a-2(b), 14a-9,” June 1, 2021, available at: https://www.sec.gov/news/public-statement/corp-fin-proxy-rules-2021-06-01.

[7] Release No. 34-89964, Procedural Requirements and Resubmission Thresholds under Exchange Act Rule 14a-8, Sept. 23, 2020, available at: https://www.sec.gov/rules/final/2020/34-89964.pdf. On June 15, 2021, a group of investors led by the Interfaith Center on Corporate Responsibility filed suit against the Commission in U.S. District Court in the District of Columbia to vacate these rule amendments. Interfaith Center on Corporate Responsibility et al. v. SEC, U.S. District Court, District of Columbia, No. 21-01620 (June 15, 2021).

[8] Accredited Investor Definition, Release No. 33-10824 (Aug. 26, 2020) [85 FR 63726]

[9] Facilitating Capital Formation and Expanding Investment Opportunities by Improving Access to Capital in Private Markets, Release No. 33-10884 (Nov. 2, 2020) [86 FR 3496].

[10] The first three items are new; the last is a continuation from the Fall 2020 Reg Flex Agenda.

[11] On June 16, 2021, the U.S. House of Representatives passed a bill, the Corporate Governance Improvement and Investor Protection Act, H.R. 1187, that would direct the Commission to issue rules within two years requiring every public company to disclose climate-specific metrics in financial statements.

[12] Acting Chair Allison Herren Lee, “Public Input Welcomed on Climate Change Disclosures,” March 15, 2021, available at: https://www.sec.gov/news/public-statement/lee-climate-change-disclosures.

[13] Linda Chatman Thomsen, “Opening Remarks Before the 15th Annual NASPP Conference,” Oct. 10, 2007, available at: https://www.sec.gov/news/speech/2007/spch101007lct.htm.the

[14] See, for example, the SEC’s Enforcement action in 2010 against Angelo Mozilo, the former head of Countrywide Financial. The SEC’s complaint alleged that, “During the course of this fraud, Mozilo engaged in insider trading in Countrywide’s securities. Mozilo established four sales plans pursuant to Rule 10b5-1 of the Securities Exchange Act in October, November, and December 2006 while in possession of material, non-public information concerning Countrywide’s increasing credit risk and the risk that the poor expected performance of Countrywide-originated loans would prevent Countrywide from continuing its business model of selling the majority of the loans it originated into the secondary mortgage market.”

[15] Gary Gensler, “Prepared Remarks at the Meeting of SEC Investor Advisory Committee,” June 10, 2021, available at: https://www.sec.gov/news/public-statement/gensler-iac-2021-06-10?utm_medium=email&utm_source=govdelivery.

[16] See Alexis Goldstein, These Invisible Whales Could Sink the Economy, N.Y. Times, May 18, 2021, available here: https://www.nytimes.com/2021/05/18/opinion/archegos-bill-hwang-gary-gensler.html

[17] See, e.g., Wachtell, Lipton, Rosen & Katz rulemaking petition on Schedule 13D filing deadlines (Mar. 7, 2011) available here: https://www.sec.gov/rules/petitions/2011/petn4-624.pdf.

[18] Commissioners Allison Herren Lee and Caroline A. Crenshaw, “Statement on Departure of Chairman Jay Clayton,” Nov. 16, 2020, available at: https://www.sec.gov/news/public-statement/lee-crenshaw-statement-departure-chairman-jay-clayton.

The following Gibson Dunn attorneys assisted in preparing this client update: Thomas J. Kim, Hillary H. Holmes, Elizabeth A. Ising, Brian J. Lane, James J. Moloney, Ronald O. Mueller and Lori Zyskowski.

Gibson Dunn’s lawyers are available to assist in addressing any questions you may have regarding these developments. Please contact the Gibson Dunn lawyer with whom you usually work, any of member of the firm’s Securities Regulation and Corporate Governance, Capital Markets or ESG practice groups, or the following:

Securities Regulation and Corporate Governance Group:

Elizabeth Ising – Washington, D.C. (+1 202-955-8287, eising@gibsondunn.com)

James J. Moloney – Orange County, CA (+ 949-451-4343, jmoloney@gibsondunn.com)

Lori Zyskowski – New York (+1 212-351-2309, lzyskowski@gibsondunn.com)

Brian J. Lane – Washington, D.C. (+1 202-887-3646, blane@gibsondunn.com)

Ronald O. Mueller – Washington, D.C. (+1 202-955-8671, rmueller@gibsondunn.com)

Thomas J. Kim – Washington, D.C. (+1 202-887-3550, tkim@gibsondunn.com)

Michael A. Titera – Orange County, CA (+1 949-451-4365, mtitera@gibsondunn.com)

Capital Markets Group:

Andrew L. Fabens – New York (+1 212-351-4034, afabens@gibsondunn.com)

Hillary H. Holmes – Houston (+1 346-718-6602, hholmes@gibsondunn.com)