March 5, 2019

2018 witnessed even more securities litigation filings than 2017, in which we saw a dramatic uptick in securities litigation as compared to previous years. This year-end update highlights what you most need to know in securities litigation developments and trends for the latter half of 2018, including:

- The Supreme Court heard oral argument in Lorenzo v. Securities and Exchange Commission, and is set to answer the question of whether a securities fraud claim premised on a false statement that was not “made” by the defendant can be pursued as a “fraudulent scheme” claim even though it would not be actionable as a Rule 10b-5(b) claim under Janus Capital Group, Inc. v. First Derivative Traders, 564 U.S. 135 (2011).

- The Supreme Court granted the petition for writ of certiorari in Emulex Corp. v. Varjabedian to consider whether Section 14(e) of the Exchange Act supports an inferred private right of action based on negligent (as opposed to knowing or reckless) misstatements or omissions made in connection with a tender offer.

- We discuss recent developments in Delaware law, including case law exploring, among other things, (1) appraisal rights, (2) the standard of review in controller transactions, (3) application of the Corwin doctrine, and (4) when a “Material Adverse Effect” permits termination of a merger agreement.

- We review case law implementing the Supreme Court’s decisions in Omnicare and Halliburton II.

- We review a decision from the Third Circuit regarding the obligation to disclose risk factors, and a decision from the Ninth Circuit regarding the utilization of judicial notice and the incorporation by reference doctrine at the motion to dismiss stage.

1. Filing and Settlement Trends

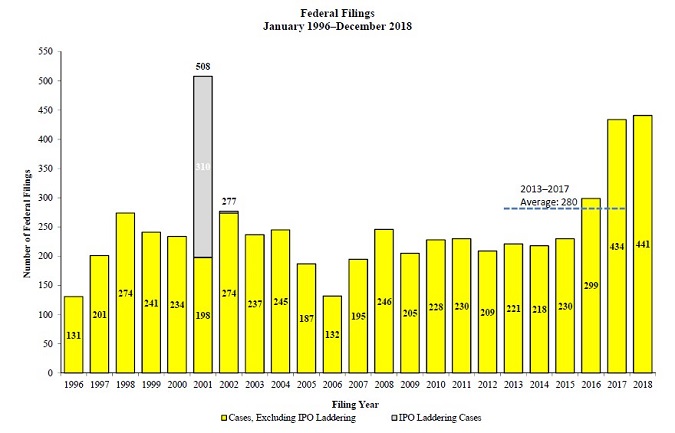

Figure 1 below reflects filing rates for 2018 (all charts courtesy of NERA). Four hundred and forty-one cases were filed this past year. This figure does not include the many class suits filed in state courts or the increasing number of state court derivative suits, including many such suits filed in the Delaware Court of Chancery. Those state court cases represent a “force multiplier” of sorts in the dynamics of securities litigation today.

Figure 1:

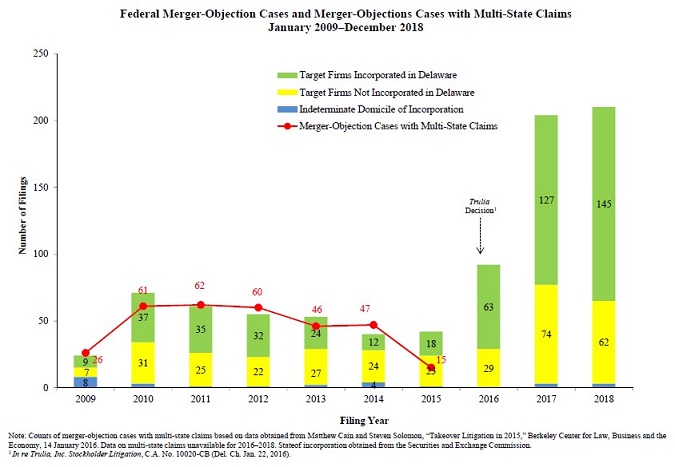

As shown in Figure 2 below, over 200 “merger objection” cases were filed in federal courts in 2018. Building off a trend from 2017, this is nearly triple the number of such cases filed in 2016, and more than quadruple the number filed in 2014 and 2015. Note that this statistic only tracks cases filed in federal courts. Historically, most M&A litigation had occurred in state court, particularly the Delaware Court of Chancery. But as we have discussed in prior updates, the Delaware Court of Chancery announced in early 2016 in In re Trulia Inc. Stockholder Litigation, 29 A.3d 884 (Del. Ch. 2016) that the much-abused practice of filing an M&A case followed shortly by an agreement on “disclosure only” settlement is effectively at an end. This is likely driving an increasing number of cases to federal court.

Figure 2:

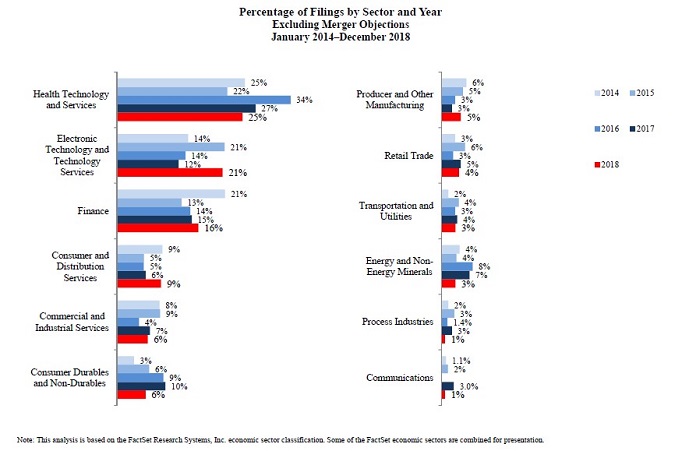

2018 saw the continuation of a decline in the percentage of cases filed against healthcare companies, following the peak of such cases in 2016. The percentage of new cases involving electronics and technology companies, meanwhile, saw a significant bump, comprising 21% of all fillings in 2018. The proportion of cases in the finance sector remained roughly consistent as compared to 2017.

Figure 3:

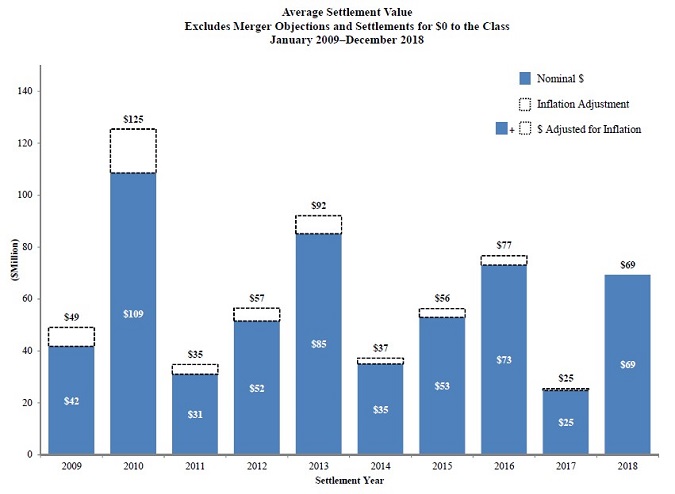

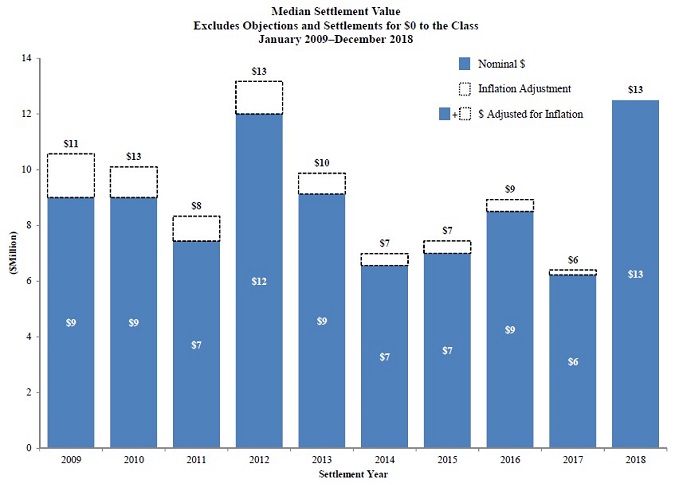

As Figure 4 shows, the average settlement value was $69 million in 2018, returning to a number comparable to the average in 2016 ($77 million) after a sharp decline to $25 million in 2017. Figure 5 reflects that the median settlement value also rose from $6 million in 2017 to $13 million in 2018. In any given year, of course, median settlement statistics also can be influenced by the timing of large settlements, any one of which can skew the numbers. The statistics are not highly predictive of the settlement value of any individual case, which is driven by a number of important factors, such as (i) the amount of D&O insurance; (ii) the presence of parallel proceedings, including government investigations and enforcement actions; (iii) the nature of the events that triggered the suit, such as the announcement of a major restatement; (iv) the range of provable damages in the case; and (v) whether the suit is brought under Section 10(b) of the Exchange Act or Section 11 of the Securities Act.

Figure 4:

Figure 5:

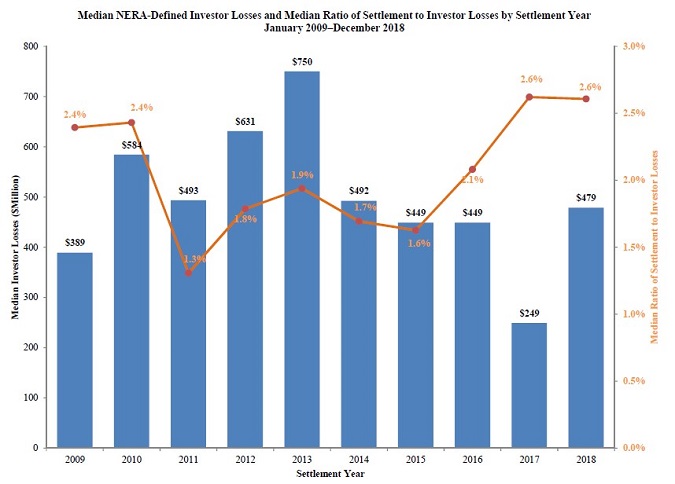

Following a decline in 2017, 2018 witnessed the return of Median NERA-Defined Investor Losses and Median Ratio of Settlement to Investor Losses by Settlement Year to $479 million, a level similar to that seen in 2015 and 2016.

Figure 6:

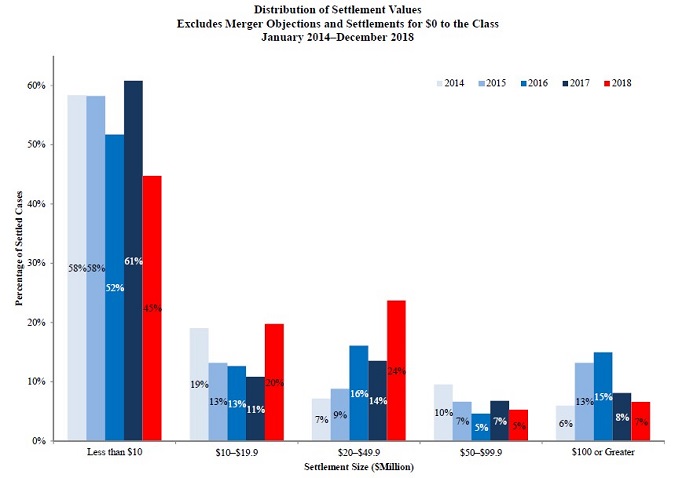

2018 also saw a greater number of settlement sizes in the $10 to $50 million range, with settlements in the $20 to $49.9 million range reaching an unprecedented 24% of all settlements.

Figure 7:

2. What to Watch for in the Supreme Court

A. Lorenzo Will Test the Reach of Janus on Who May Be Held Liable for False Statements

In our 2018 Mid-Year Securities Litigation Update, we discussed the Supreme Court’s grant of certiorari in Lorenzo v. Securities and Exchange Commission, No. 17-1077. As readers will recall, Lorenzo involves the question of whether a securities fraud claim premised on a false statement that was not “made” by the defendant can be pursued as a “fraudulent scheme” claim under Section 17(a)(1) of the Securities Act and Exchange Act Rules 10b-5(a) and 10b-5(c) even though it would not be actionable under Rule 10b-5(b) pursuant to the Court’s ruling in Janus Capital Group, Inc. v. First Derivative Traders, 564 U.S. 135 (2011). In the decision below, the D.C. Circuit held that Lorenzo’s distribution of an email that included false statements drafted by his supervisor could not form the basis for 10b-5(b) liability under Janus, but could form the basis for “scheme” liability under 10b-5(a) and (c). Lorenzo v. Sec. & Exch. Comm’n, 872 F.3d 578, 580, 592 (D.C. Cir. 2017). Then-Judge Kavanaugh dissented from the panel opinion.

In the merits brief, Petitioner (a securities broker) argued that allowing scheme liability would permit an end-run around the Court’s decision in Janus, which held that only the “maker” of a statement can face primary liability for securities fraud. Brief for Petitioner at 24. Petitioner specifically contended that the D.C. Circuit’s ruling would effectively nullify Janus, and would allow the SEC to impose liability for conduct under 10b-5(a) and (c) that is not actionable under 10b-5(b). Id. at 27-28. Petitioner also argued that the scheme liability theory adopted by the D.C. Circuit is functionally no different than aiding-and-abetting liability—a theory of liability under Section 10(b) of the Exchange Act that the Supreme Court rejected in Central Bank of Denver v. First Interstate Bank of Denver, 511 U.S. 164, 177 (1994). Id. at 36.

In its responsive brief on the merits, Respondent (the SEC) argued that neither Janus nor Central Bank purport to extend their holdings to claims made pursuant to Rules 10b-5(a) and (c). Brief for Respondent at 23-26, 31-33. On behalf of the SEC, the U.S. Solicitor General also argued that because the messages that contained the false statements were sent by Lorenzo, and because the transmission of the messages was necessary to the scheme, Lorenzo’s actions fall squarely within the provisions imposing scheme liability. Id. at 15-18.

At oral argument on December 3, 2018, several Justices seemed troubled by Lorenzo’s argument because Janus relied on statutory text that prohibited the “making” of a false statement, but the statutory provisions under which the SEC charged Lorenzo do not include any references to the “making” of statements. Justice Alito repeatedly pressed Lorenzo’s counsel to explain why the alleged conduct did not “fall squarely within the language” of the statute. Tr. at 11. Justice Kagan expressed skepticism of Lorenzo’s theory that the various provisions of the anti-fraud statutes are “mutually exclusive,” such that misstatements can be sanctioned only under the provisions directed specifically at misstatements. Tr. at 25. Justice Gorsuch, however, appeared more accepting of Petitioner’s arguments, and pressed the government’s lawyer on how scheme liability could apply when the only fraud is the making of a false statement (a fraud claim barred by Janus on these facts). Tr. at 32-36. Justice Kavanaugh was recused because he participated in the decision below.

We expect a decision in Lorenzo by the end of the 2018 Supreme Court Term in June 2019. We will continue to monitor developments in this area and report on any updates in our 2019 Mid-Year Securities Litigation Update.

B. In Emulex, the Court Will Address whether Liability May Be Imposed under Section 14(e) for Negligent Conduct

On January 4, 2019, the Supreme Court granted certiorari in Emulex Corp. v. Varjabedian, No. 18-459, to consider whether Section 14(e) of the Exchange Act supports an inferred private right of action based on negligent misstatements or omissions made in connection with a tender offer. The case arises out of the Ninth Circuit, which split with five of its sister circuits in holding that plaintiffs seeking to recover under Section 14(e) of the Exchange Act need only plead and prove negligence, not scienter. 888 F.3d 399, 405 (9th Cir. 2018).

This case involves a joint press release announcing a merger between Avago Technologies Wireless Manufacturing, Inc. and Emulex Corp. The press release announced that Avago would pay a premium for Emulex stock. Documents filed with the SEC in support of the offer omitted a one-page “Premium Analysis” showing that while the premium fell within the normal range of merger premiums in comparable transactions, it was below average. A class of former Emulex shareholders filed a putative class action and alleged defendants had violated Section 14(e) by failing to summarize the Premium Analysis and to disclose that the premium was below the average for premiums in similar mergers. The district court dismissed the Section 14(e) claim for failure to plead that the misstatement or omission was made intentionally or with deliberate recklessness.

The Ninth Circuit reversed the district court, noting that Section 14(e) contains two separate clauses, which each proscribe different conduct: (1) making or omitting an untrue statement of material fact and (2) engaging in fraudulent, deceptive or manipulative acts or practices. The Ninth Circuit reasoned that the first clause, on its face, does not include a scienter requirement. Although the Ninth Circuit acknowledged that five other circuits (the Second, Third, Fifth, Sixth, and Eleventh) have held that Section 14(e) requires that plaintiffs plead scienter, the Ninth Circuit believes those circuits ignored or misread Supreme Court precedent to import Rule 10b-5’s scienter requirement to Section 14(e) claims. Id. at 405. According to the Ninth Circuit, Ernst & Ernst v. Hochfelder, 425 U.S. 185, 193 (1976), found that Rule 10b-5 requires a showing of scienter because it was promulgated by the SEC, which only has the authority to regulate manipulative or deceptive devices that necessarily entail scienter. Varjabedian, 888 F. Supp. at 406. The Ninth Circuit also reasoned that the text of Section 14(e) is similar to that of Section 17(a)(2) of the Securities Act, which the Supreme Court held in Aaron v. SEC, 446 U.S. 680, 696-97 (1980), does not require a showing of scienter. Varjabedian, 888 F. Supp. at 406. The Ninth Circuit distinguished the contrary rulings in the other circuits by noting that they were either decided before Ernst & Ernst and Aaron or that they failed to follow the reasoning of those decisions and acknowledge the distinction between Rule 10b-5 and Section 14(e). Id. at 405.

Emulex filed a petition for a writ of certiorari on October 11, 2018. Emulex argued that the Ninth Circuit’s decision “upset[] the statutory scheme enacted by Congress.” Petition for Writ of Certiorari at 15. Emulex further contended that the Supreme Court has not previously recognized a private right of action under Section 14(e) and declined to do so in Piper v. Chris-Craft Industries Inc., 430 U.S. 1, 24 (1977). While lower courts have inferred a private right of action, they have declined to create private rights of action for negligent conduct. Petition for Writ of Certiorari at 18-19. Emulex also argued that the circuit split “blew up” the consensus among circuit courts which had held that Section 14(e) does not support a private right of action or remedy based on mere negligence. Id. at 14. The Ninth Circuit’s decision, according to Petitioner, “creat[es] an expansive new regime at odds with the uniform view in the rest of the country.” Id. at 15.

As noted, the Supreme Court granted certiorari in January 2019. We expect that the parties will submit their briefing to the Supreme Court in the spring of 2018, with oral argument to follow in the coming months. We will continue to monitor this appeal and provide an update in our 2019 Mid-Year Securities Litigation Update.

C. Pending Certiorari Petitions

There are two notable securities cases in which petitions for certiorari are pending. The first is Toshiba Corp. v. Automotive Industries Pension Trust Fund, No. 18-486, which also involves a circuit split created by the Ninth Circuit. The Ninth Circuit split from the Second Circuit in holding that the Supreme Court’s landmark decision in Morrison v. National Australia Bank Ltd., 561 U.S. 247 (2010), which held that U.S. securities laws do not apply extraterritorially, does not bar suits arising out of domestic transactions in the securities of a foreign issuer even when the foreign issuer has no role in facilitating the transaction. Also pending is First Solar Inc. v. Mineworkers’ Pension Scheme, No. 18-164, which we discussed in the 2018 Mid-Year Securities Litigation Update. Readers will recall that, in that case, the Ninth Circuit issued a per curiam opinion holding that loss causation can be established even when the corrective disclosure did not reveal the fraud on which the securities fraud claim is based.

In both Toshiba and First Solar, the Supreme Court has entered orders requesting the Solicitor General to file briefs expressing the views of the United States. The government has not yet filed its brief in either case. We will continue to monitor these petitions and provide an update in our 2019 Mid-Year Securities Litigation Update if the Supreme Court grants certiorari.

3. Delaware Law Developments

A. Contractual Waiver of Appraisal Rights Enforceable under Delaware Law

In our 2018 Mid-Year Securities Litigation Update, we reported on two Court of Chancery decisions interpreting and applying new Delaware appraisal law set forth in Dell, Inc. v. Magnetar Global Event Driven Master Fund Ltd., 177 A.3d 1 (Del. 2017). In the second half of 2018, the Court of Chancery continued implementing the Delaware Supreme Court’s directive by looking first—and primarily—to market factors to determine the fair value of a company’s stock when supported by appropriate facts. See Blueblade Capital Opportunities LLC v. Norcraft Cos., 2018 WL 3602940 (Del. Ch. July 27, 2018) (giving deal price no weight where stock thinly traded and sales process significantly flawed); In re Appraisal of Solera Holdings, Inc., 2018 WL 3625644 (Del. Ch. July 30, 2018) (giving deal price “dispositive” weight where sales process was “characterized by many objective indicia of reliability” and company’s actively traded stock had “a deep base of public stockholders”).

Delaware courts also looked at appraisal mechanics in other contexts. In Manti Holdings, LLC v. Authentix Acquisition Co., the Court of Chancery enforced a provision in a stockholder agreement waiving stockholders’ right to pursue statutory appraisal for certain transactions. 2018 WL 4698255 (Del. Ch. Oct. 1, 2018). Stockholder-petitioners who had entered into the stockholder agreement lost their shares via merger. Id. at *1. Under the stockholder agreement, they had agreed “to refrain from the exercise of appraisal rights” if “a Company Sale [was] approved by the Board.” Id. at *2. That a “Company Sale” occurred was not disputed.

In reaching its conclusion that the waiver was enforceable, the Court rejected as nonsensical the Petitioners’ argument that the waiver terminated upon consummation of the deal. Id. at *3. Importantly, the Court rejected the Petitioners’ argument that enforcing the Agreement “would impermissibly . . . impose a limitation on classes of stock by contract” in violation of DGCL Section 151(a), which, according to the Petitioners, requires such limits to derive from the corporate charter. Id. at *4. Reasoning that the Company entered into the agreement to “entice investment” and that the stockholders simply “took on contractual responsibilities in exchange for consideration,” the Court held that enforcing the stockholder agreement was “not the equivalent of imposing limitations on a class of stock under Section 151(a).” Id.

B. Courts Clarify MFW’s “Ab Initio” Requirement

In the second half of 2018, both the Delaware Supreme Court and the Court of Chancery clarified when the “ab initio” requirement is satisfied under Kahn v. M & F Worldwide Corp. (“MFW”), 88 A.3d 635, 644 (Del. 2014). Under MFW, a conflicted-controller transaction earns business judgment review when six elements are satisfied: (i) the procession of the transaction is conditioned ab initio on the approval of both a special committee and a majority of the minority stockholders (the “dual protections”); (ii) the special committee is independent; (iii) the special committee is empowered to freely select its own advisors and to say no definitively; (iv) the special committee meets its duty of care in negotiating a fair price; (v) the vote of the minority stockholders is informed; and (vi) there is no coercion of the minority stockholders. Id. at 645.

In Olenik v. Lodzinski, the Court of Chancery held that the ab initio requirement was satisfied because the controller’s first offer, although extended after nine months of discussions, announced MFW’s dual protections “‘before any negotiations took place.’” 2018 WL 3493092, at *15 (Del. Ch. July 20, 2018) (quoting Swomley v. Schlecht, 2014 WL 4470947, at *21 (Del. Ch. 2014), aff’d, 128 A.3d 992 (Del. 2015) (TABLE)). The Court relied on settled Delaware law distinguishing between “discussions,” which were extensive in Olenik, and “negotiations,” which began only with the controller’s first offer. Id. at *16; see also Colonial Sch. Bd. v. Colonial Affiliate, NCCEA/DSEA/NEA, 449 A.2d 243, 247 (Del. 1982) (distinguishing between “negotiate,” which “means to bargain toward a desired contractual end,” and “discuss,” which “means merely to exchange thoughts and points of views on matters of mutual interest”).

The Delaware Supreme Court weighed in three months later, holding in Flood v. Synutra International, Inc. that the ab initio element “require[s] the controller to self-disable before the start of substantive economic negotiations, and to have both the controller and Special Committee bargain under the pressures exerted on both of them by these protections.” 195 A.3d 754, 763 (Del. 2018). In particular, the Supreme Court affirmed the trial court’s conclusion that the controller satisfied the ab initio element by conditioning the transaction on MFW’s dual protections in “the Follow-up Letter [sent] just over two weeks after [it] first proposed the Merger, before the Special Committee ever convened and before any negotiations ever took place.” Id. at 764.

Although these decisions are based on notably different facts—for example, nine months elapsed between the initial communication and the first offer in Olenik, and only two weeks passed between the initial communication and “the Follow-up Letter” in Synutra—they appear to create one rule: MFW’s “ab initio” requirement will be satisfied as long as the controller commits to MFW’s dual protections before substantive economic negotiations occur. Olenik is on appeal to the Delaware Supreme Court, which may further clarify matters.

C. Inadequate Disclosures Preclude Cleansing under Corwin

In two recent cases, the Court of Chancery concluded the Corwin doctrine did not apply. In re Xura, Inc. S’holder Litig., 2018 WL 6498677 (Del. Ch. Dec. 10, 2018) (denying Corwin motion based on seven alleged material omissions); In re Tangoe, Inc. S’holder Litig., 2018 WL 6074435 (Del. Ch. Nov. 20, 2018) (holding stockholders were not adequately informed for Corwin purposes where audited financials and the facts underlying a restatement were not disclosed). Under Corwin, the business judgment rule applies to judicial review of transactions that are not otherwise subject to the entire fairness standard so long as the transaction was “approved by a fully informed, uncoerced vote of the disinterested stockholders.” See id. at *9 (quoting Corwin v. KKR Fin. Hldgs. LLC, 125 A.3d 304, 309 (Del. 2015)).

Initially an appraisal proceeding, Xura morphed into a plenary action after appraisal discovery revealed questionable conduct primarily by a seller’s CEO. Xura, 2018 WL 6498677, at *1. The CEO, it was alleged, steered his company into a transaction with an interest that differed from other stockholders: self-preservation. Id. at *11. He stood to lose his job and a $25 million payout if the company was not sold. Id. at *13. The proxy statement for the deal failed to disclose the CEO’s actions relating to the sales process, leaving stockholders “entirely ignorant” of his influence over the transaction and “his possible self-interested motivation for pushing an allegedly undervalued [t]ransaction on the [c]ompany and its stockholders.” Id. Vice Chancellor Slights held that Corwin-cleansing was unavailable because the “stockholders could not have cleansed conduct about which they did not know.” Id. at *12.

The stockholders in Tangoe similarly were found to be uninformed. Thirteen months before the transaction at issue, the SEC notified Tangoe that it would need to restate almost three years of its financials. Tangoe, 2018 WL 6074435, at *1. Tangoe took so long to do so that NASDAQ delisted its stock and the SEC threatened to deregister it. Id. at *2. After an activist stockholder increased its stake in the company and signaled to the board that “a proxy contest was coming,” the board began shifting its focus from restating the financials to selling the company. Id. at *1, 4-6. While it did so, it also altered its own compensation so that its members collectively would receive nearly $5 million in the event of a change of control. Id. at *5, 12-13.

Throughout the sales process, the board failed to provide stockholders with audited financial statements. Although the Court pointed out that audited financial statements are not per se material, when combined with the misstatements in the company’s financial statements, among other things, the stockholders were left in an “information vacuum.” Id. at *10. The Court also found it significant that the board failed to disclose information related to the process of restating the company’s financials. Id. at *11. Accordingly, the Court held that Corwin-cleansing was unavailable because a reasonable inference could be drawn that the stockholders were not fully informed when they approved the transactions. Id. at *10-12.

D. Delaware Supreme Court Affirms MAE Ruling

On December 7, 2018, the Delaware Supreme Court affirmed the Court of Chancery’s recent post-trial ruling that a “Material Adverse Effect” (or “MAE”) permitted a buyer to terminate a merger agreement. Akorn, Inc. v. Fresenius Kabi AG, 2018 WL 4719347 (Del. Ch. Oct. 1, 2018), aff’d, — A.3d —-, 2018 WL 6427137 (Del. Dec. 7, 2018). Several factors contributed to the Court of Chancery’s finding that Akorn suffered an MAE. First, after Fresenius agreed to acquire Akorn, Akorn’s business “fell off a cliff”: in three consecutive quarters, it announced year-over-year declines in quarterly revenues of 29%, 29%, and 34%; in operating income of 84%, 89%, and 292%; and in earnings per share of 96%, 105%, and 300%. Id. at *21, 24, 35. Second, whistleblower letters prompted an investigation into Akorn’s product development and quality control process. Id. at *26. This investigation revealed many flaws, including falsification of laboratory data submitted to the FDA. Id. at *30-31. Third, Akorn failed to operate its business in the ordinary course post-signing, fundamentally changing its quality control and information technology functions without Fresenius’s consent. Id. at *88. On appeal, the Delaware Supreme Court held that the record “adequately support[ed]” the Court of Chancery’s determination. Akorn, Inc., — A.3d —-, 2018 WL 6427137 (Del. Dec. 7, 2018).

E. N.Y. First Department Reverses Xerox, Dissolves Injunction

As we reported in our 2018 Mid-Year Securities Litigation Update, in April 2018, the New York Supreme Court enjoined a multi-billion dollar merger of Xerox Corp. and Fujifilm Holdings Corp. (“Fujifilm”) because Xerox’s CEO, who negotiated the deal, and a majority of Xerox’s board were conflicted or lacked independence because they expected to continue serving the combined entity. In re Xerox Corp. Consolidated Shareholder Litigation, 2018 WL 2054280, at *7 (N.Y. Sup. Apr. 27, 2018). Xerox and Fujifilm appealed.

In October 2018, the First Department reversed the decision unanimously “on the law and the facts,” holding that the business judgment rule applied and that the plaintiffs had failed to show a likelihood of success on their breach of fiduciary duty and fraud claims. Deason v. Fujifilm Holdings Corp., 165 A.D.3d 501 (1st Dep’t 2018). In particular, the plaintiffs “failed to show bad faith or a disabling interest on the part of the majority of the directors of Xerox” because “the possibility that any one of the directors would be named to [the combined] board alone was not a material benefit such that it was a disabling interest;” any potential conflict created by Xerox’s CEO continuing as the future CEO of the new company was acknowledged by the board; and the board “engaged outside advisers,” “discussed the proposed transaction on numerous occasions,” and the deal was not “unreasonable on its face.” Id. at 501-02. As a result, the First Department dismissed the complaints against Fujifilm and dissolved the injunctions enjoining the deal. Id.

On February 21, 2019, the First Department denied the class plaintiffs’ motion for reargument or, in the alternative, leave to appeal to the Court of Appeals.

4. Falsity of Opinions – Omnicare Update

As discussed in our prior securities litigation updates, courts continue to define the boundaries of Omnicare, Inc. v. Laborers District Council Construction Industry Pension Fund, 135 S. Ct. 1318 (2015). The Supreme Court’s Omnicare decision addressed the scope of liability for false opinion statements under Section 11 of the Securities Act. The Court held that “a sincere statement of pure opinion is not an ‘untrue statement of material fact,’ regardless whether an investor can ultimately prove the belief wrong.” Id. at 1327. An opinion statement can give rise to liability only when the speaker does not “actually hold[] the stated belief,” or when the opinion statement contains “embedded statements of fact” that are untrue. Id. at 1326–27. But in the heavily debated “omission” part of the opinion, the Court held that a factual omission from a statement of opinion gives rise to liability when the omitted facts “conflict with what a reasonable investor would take from the statement itself.” Id. at 1329.

The plaintiffs’ bar predicted that this omission theory of falsity would give rise to a wave of securities litigation complaints poised to survive the pleadings phase. While the theory has indeed become commonplace in complaints, it has fared little to no better in the last half of 2018 against the exacting pleading standards generally applicable to all theories of liability under the securities laws. See, e.g., Hering v. Rite Aid Corp., 331 F. Supp. 3d 412, 427 (M.D. Pa. 2018) (finding that “Plaintiff has failed to meet the exacting pleading standard of the PSLRA” where reasonable investors would understand the statements to be estimates). One district court recently emphasized that “a general allegation that ‘Defendants had knowledge of, or recklessly disregarded, omitted facts’” is insufficient. In re Under Armour Sec. Litig., 342 F. Supp. 3d 658, 676 (D. Md. 2018) (citation omitted). Another court rejected plaintiff’s claim that defendants should have conducted an inquiry into the facts underlying their opinion, finding that “[a] blanket conclusory assertion that no investigation occurred, without more, is insufficient.” Pension Tr. v. J. Jill, Inc., 2018 WL 6704751, at *8 (D. Mass. Dec. 20, 2018).

Courts have specifically grappled with whether plaintiffs met the pleading standard in cases involving a company’s general opinions on its financial condition. In Frankfurt-Tr. Inv. Luxemburg AG v. United Technologies Corp., the Southern District of New York held that “omitting even significant, directly contradictory information from opinion statements is not misleading, ‘especially’ when there are countervailing disclosures.” 336 F. Supp. 3d 196, 230–31 (S.D.N.Y. 2018). Relying on Tongue v. Sanofi, 816 F.3d 199 (2d Cir. 2016) and Martin v. Quartermain, 732 F. App’x 37 (2d Cir. 2018), the court found that statements about the company’s business and projected earnings per share were not misleading even where they failed to disclose specifics regarding a “slowdown of commercial aftermarket sales” and other potentially negative factors. Id. at 230. Plaintiff’s allegations—unlike the highly detailed allegations about test data in Sanofi and Martin—were “too scant in detail and scope” and “at a high level,” meaning that they failed to show that the alleged omissions would have a meaningful impact on a reasonable investor’s understanding of the company. Id. On the other hand, the District of Delaware found that plaintiffs met their pleading burden where they alleged that particular information omitted from a proxy statement, which recommended that shareholders vote in favor of a merger, made other specific statements about the fairness of the merger misleading. Laborers’ Local #231 Pension Fund v. Cowan, 2018 WL 3243975, at *10–12 (D. Del. July 2, 2018), reargument denied, 2018 WL 3468216 (D. Del. July 18, 2018). Because the board cited a fairness opinion in its decision to approve the merger, the court held that a reasonable investor may have thought that the company “placed confidence” in the fairness opinion and believed that it “accurately analyzed [the company’s] potential financial growth,” which “conflict[ed] with undisclosed facts or knowledge held by the board,” namely that the fairness opinion “did not incorporate acquisition based growth into its projections.” Id. at *10–11.

Several courts also provided guidance for companies making opinion statements about legal and compliance risks, again highlighting the importance of context. For example, the Northern District of Illinois concluded that statements about legal compliance that were accompanied by disclosures concerning an ongoing IRS investigation would not be misleading to reasonable investors “unless they ignore[d] those disclosures.” Societe Generale Sec. Servs., GbmH v. Caterpillar, Inc., 2018 WL 4616356, at *4–5 (N.D. Ill. Sept. 26, 2018). Likewise, in Jaroslawicz v. M&T Bank Corp., the Third Circuit found that a company’s statements about its due diligence, which allegedly omitted deficiencies in its anti-money laundering compliance program, were not misleading. 912 F.3d 96, 113–14 (3d Cir. 2018). Paying close attention to the context, the court held that the statements were accompanied by sufficient facts that the company conducted a shorter period of diligence than investors may have otherwise expected. See id. at 114. In addition, the plaintiffs alleged both general negligence—insufficient to plead a violation under Omnicare—as well as that “a reasonable investor would have expected the banks to conduct a sampling of customer accounts” as part of their due diligence process. Id. The court found that a single allegation that the bank could have conducted a sampling was too weak to defeat the motion to dismiss. See id. In contrast, a Southern District of New York court found that a company’s statements regarding careful management and compliance with laws regarding its credit portfolio could be misleading because plaintiffs alleged that company was aware of particular facts suggesting the falsity of those statements. See In re Signet Jewelers Ltd. Sec. Litig., 2018 WL 6167889, at *12–13 (S.D.N.Y. Nov. 26, 2018). Noting that the pleading burden is “no small task,” the court held that plaintiffs nevertheless met their burden because they alleged “particularized and material[] facts” based on the testimony of former employees who provided information to the plaintiffs. Id. at *13. In particular, specific allegations that the company was “aware that a substantial and growing portion of its credit portfolio contained subprime loans and chose to disregard internal warnings about that fact” rendered the complaint sufficient to survive a motion to dismiss. Id.

In the latter half of the year, courts also dealt with the circumstances in which a pharmaceutical company’s opinions on the safety of a drug undergoing clinical trials may give rise to liability under Omnicare. In Hirtenstein v. Cempra, Inc., the court held that the company’s statements that it believed a drug was safe was an inactionable opinion. 2018 WL 5312783, at *17–18 (M.D.N.C. Oct. 26, 2018). Plaintiffs claimed that because the company’s chief executive officer “elected to speak about [the drug’s] purportedly ‘compelling’ clinical data . . . [she] had a duty to disclose that . . . safety data showed a significant and genuine signal for liver toxicity and liver injury.” Id. at *17. The court held that the company did not have a “duty to disclose adverse events, particularly where the statements [were] couched as opinion and [did] not constitute affirmative statements that there are no safety concerns associated with the drug.” Id. at *18. These types of opinions could not be actionable, where they were “little more than vague optimistic statements regarding the safety profile of the drug.” Id. at *19. On the other hand, in SEB Inv. Mgmt. AB v. Endo International, PLC, the court found that plaintiff stated a Section 11 claim where it alleged that the company had specific knowledge of “an increasing number of serious adverse events linked to injection” of the drug at issue. 2018 WL 6444237, at *21–22 (E.D. Pa. Dec. 10, 2018). Despite the fact that the company allegedly knew about the “increased rate in injection use, [it] failed to disclose to investors that it faced a serious risk of regulatory action, including removal of the drug from the market,” forming the basis for an actionable Section 11 claim. Id.

5. Courts Continue to Shape “Price Impact” Analysis at the Class Certification Stage

Courts across the country continue to grapple with implementing the Supreme Court’s landmark ruling in Halliburton Co. v. Erica P. John Fund, Inc., 134 S. Ct. 2398 (2014) (“Halliburton II”), although the second half of 2018 did not bring any new decisions from the federal circuit courts of appeal. In Halliburton II, the Supreme Court preserved the “fraud-on-the-market” presumption—a presumption enabling plaintiffs to maintain the common proof of reliance that is essential to class certification in a Rule 10b-5 case—but made room for defendants to rebut that presumption at the class certification stage with evidence that the alleged misrepresentation had no impact on the price of the issuer’s stock. Two key questions continue to recur. First, how should courts reconcile the Supreme Court’s explicit ruling in Halliburton II that direct and indirect evidence of price impact must be considered at the class certification stage, Halliburton II, 123 S. Ct. at 2417, with its previous decisions holding that plaintiffs need not prove loss causation or materiality until the merits stage? See Erica P. John Fund, Inc. v. Halliburton Co., 563 U.S. 804 (2011) (“Halliburton I”); Amgen Inc. v. Conn. Ret. Plans & Trust Funds, 568 U.S. 455 (2013). Second, what standard of proof must defendants meet to rebut the presumption with evidence of no price impact?

As we have previously reported, the Second Circuit has addressed both of these key questions in Waggoner v. Barclays PLC, 875 F.3d 79 (2d Cir. 2017) (“Barclays”) and Arkansas Teachers Retirement System v. Goldman Sachs, 879 F.3d 474 (2d Cir. 2018) (“Goldman Sachs”). Those decisions remain the most substantive interpretations of Halliburton II. Barclays addressed the standard of proof necessary to rebut the presumption of reliance and held that after a plaintiff establishes the presumption of reliance applies, defendant bears the burden of persuasion to rebut the presumption by a preponderance of the evidence. As we have previously noted, this puts the Second Circuit at odds with the Eighth Circuit, which cited Rule 301 of the Federal Rules of Evidence when reversing a trial court’s certification order on price impact grounds, see IBEW Local 98 Pension Fund v. Best Buy Co., 818 F.3d 775, 782 (8th Cir. 2016), because Rule 301 assigns only the burden of production—i.e., producing some evidence—to the party seeking to rebut a presumption, but “does not shift the burden of persuasion, which remains on the party who had it originally.” Fed. R. Evid. 301. That inconsistency, however, was not enough to persuade the Supreme Court to review the Second Circuit’s decision. Barclays PLC v. Waggoner, 138 S.Ct. 1702 (Mem) (2018) (denying writ of certiorari).

In Goldman Sachs, the Second Circuit vacated the trial court’s ruling certifying a class and remanded the action, directing that price impact evidence must be analyzed prior to certification, even if price impact “touches” on the issue of materiality. Goldman Sachs, 879 F.3d at 486. Following the Second Circuit’s decision, the district court held an evidentiary hearing and heard oral argument. In re Goldman Sachs Grp. Sec. Litig., 2018 WL 3854757, at *1-2 (Aug. 14, 2018). The court, again, certified the class. Id. On remand, plaintiffs argued that because the company’s stock price declined following the announcement of three regulatory actions related to the company’s conflicts of interest, previous misstatements about its conflicts had inflated the company’s stock price. See id. at * 2. Defendants argued the alleged misstatements could not have caused the stock price drops for two reasons, and offered expert testimony to support each. Id. at *3. First, they argued that the company’s stock price had not reacted to thirty-six prior reports commenting on company conflicts, and, therefore, the identified stock price drops could not be linked to the alleged misstatements. Id. at *3. Second, they argued that news of enforcement activities (and not a correction of earlier statements regarding conflicts and business practices) caused the identified stock price drops. Id. The court found plaintiff’s expert’s “link between the news of Goldman’s conflicts and the subsequent stock price declines . . . sufficient.” Id. at *4. The court was persuaded that the first allegedly corrective disclosure revealed new information about the conflicts, see id., and held that defendants’ expert testimony regarding alternative explanations for the stock price decline (i.e., the nature of the enforcement actions rather than the subject matter) was not sufficient to “sever” that link. Id. at *5-6. The Second Circuit has agreed to review Goldman Sachs for a second time and has ordered an expedited briefing schedule. See Order, Ark. Teachers Ret. System v. Goldman Sachs, Case No. 18-3667 (2d Cir. Jan. 31, 2019).

The Third Circuit is also poised to substantively address price impact analysis at the class certification stage in the coming months in its review of Li v. Aeterna Zentaris, Inc., 324 F.R.D. 331 (D.N.J. 2018) (“Aeterna”). See Order, Vizirgianakis v. Aeterna Zentaris, Inc., No. 18-8021 (3d Cir. Mar. 30, 2018). Substantive briefing is completed in Aeterna, which invites the Third Circuit to clarify the type of evidence defendants must present, including the burden of proof they must meet to rebut the presumption of reliance and whether statistical evidence rebutting the presumption must meet a 95% confidence threshold. In certifying the class, the district court described defendants’ burden as “producing [enough] evidence . . . ‘to withstand a motion for summary judgment or judgment as a matter of law,’” Aeterna, 324 F.R.D. at 344 (quoting Lupyan v. Corinthian Colleges, Inc., 761 F.3d 314, 320 (3d Cir. 2014) and citing Best Buy, 818 F.3d at 782 and Fed. R. Evid. 301), but then observed defendants failed to prove lack of price impact with “‘scientific certainty,’” see id. at 345 (quoting Carpenters Pension Trust Fund of St. Louis v. Barclays PLC, 310 F.R.D. 69, 95 (S.D.N.Y. 2015)). The district court rejected defendants’ argument that plaintiff’s event study, which did not attribute a statistically significant price movement to the alleged misstatement, rebutted the presumption and criticized defendants for not offering their own event study. See id. at 345.

We will continue to monitor developments in these and other cases.

6. The Third Circuit Explores the Requirement to Disclose Risk Factors

In late December 2018, the Third Circuit issued a decision in the latest case to address the scope of disclosure requirements for proxy solicitations under Section 14(a) of the Securities Exchange Act of 1934. In Jaroslawicz v. M&T Bank Corp., 912 F.3d 96 (3d Cir. 2018), former shareholders of Hudson City Bancorp filed suit against Hudson and M&T Bank, alleging the joint proxy soliciting votes for the merger between the two entities was materially misleading because (1) it failed to disclose certain practices that did not comply with relevant regulatory requirements, which posed significant risk factors facing the merger, as required under Item 503(c) of Regulation S-K (the “Regulatory Risk Disclosures”); and (2) these omissions rendered opinion statements regarding M&T Bank’s compliance with laws materially false and misleading (the “Legal Compliance Disclosures”). Specifically, as to the Regulatory Risk Disclosures, the proxy statement was alleged to be misleading because it did not discuss M&T Bank’s past consumer violations involving switching no-fee checking accounts to fee-based accounts. As to Legal Compliance Disclosures, the proxy statement was alleged to be misleading because M&T Bank had failed to discuss deficiencies in its Bank Secrecy Act/anti-money laundering (“BSA/AML”) compliance program until it filed a supplemental disclosure six days before the shareholder vote, when it disclosed for the first time that it was the subject of a Federal Reserve Board investigation on these programs.

In interpreting the scope of disclosure under Item 503(c), which requires proxy issuers to discuss “the most significant factors that make the offering speculative or risky,” the Court explained that risk disclosures, such as the Regulatory Risk Disclosures at issue, must be “company-specific” in order to insulate an issuer from liability. Jaroslawicz, 912 F.3d at 106–08. Thus, “generic disclosures which could apply across an industry are insufficient” to protect a company in the event that a risk falling under a “boilerplate” disclosure later transpires. Id. at 108, 111. For this reason, the Court concluded that M&T Bank’s generic references to being subject to regulatory oversight were not “company-specific” risk factors that would “communicate anything meaningful” to stockholders. Id. at 111. Thus, even though the bank had ceased its alleged consumer violations, the Court found it plausible that the undisclosed “high volume of past violations made the upcoming merger vulnerable to regulatory delay.” Id. at 107.

With respect to the plaintiffs’ allegations regarding BSA/AML deficiencies, the Court held that the supplemental proxy statement’s disclosure that the bank was the subject of an investigation regarding these practices, which “would likely result in delay of regulatory approval,” was “likely adequate” under Section 14(a). However, because the supplemental disclosures were issued a mere six days before the stockholder vote on the transaction, the Court concluded that the plaintiffs had adequately alleged that a reasonable investor did not have enough time to digest this relevant information. Id. at 112.

Further, although the Court declined to expressly decide whether a heightened standard for pleading falsity applied to the Legal Compliance Disclosures and other claims brought under Section 14(a) of the Exchange Act, it found that the stockholders failed to allege a claim under their “misleading opinion” theory. Id. at 113. In dismissing plaintiffs’ Omnicare claims alleging that the Legal Compliance Disclosures were actionably misleading, the Court reiterated the longstanding principle that an opinion statement is not rendered misleading simply because it later “proved to be false.” Id. Crucially, the Court explained that the Legal Compliance Disclosures in the proxy statement were not plausibly alleged to be misleading because the bank adequately divulged the basis for its opinion. In particular, the proxy statement made clear that the bank had concluded it was in compliance with applicable laws based on a brief period of due diligence conducted in connection with the transaction. Id. at 114.

7. The Ninth Circuit Clarifies when Courts May Consider Documents Outside of the Pleadings on Motions to Dismiss Securities Claims

On August 13, 2018, the Ninth Circuit revisited the extent to which a court can properly consider materials outside of the four corners of the complaint in ruling on a motion to dismiss a securities claim. Khoja v. Orexigen Therapeutics, Inc., 899 F.3d 988, 994 (9th Cir. 2018).

It is well settled that courts must not only accept all factual allegations in a complaint as true for purposes of deciding a motion to dismiss, but also consider “other sources courts ordinarily examine when ruling on Rule 12(b)(6) motions to dismiss, in particular, [1] documents incorporated into the complaint by reference, and [2] matters of which a court may take judicial notice.” Tellabs, Inc. v. Makor Issues & Rights, Ltd., 551 U.S. 308, 322 (2007). In the Ninth Circuit, a defendant can seek to treat a document as incorporated into the complaint “if the plaintiff refers extensively to the document or the document forms the basis of the plaintiff’s claim.” United States v. Ritchie, 342 F.3d 903, 907 (9th Cir. 2003). The incorporation by reference doctrine allows courts to treat documents as if they are part of the complaint in their entirety, which “prevents plaintiffs from selecting only portions of documents that support their claims, while omitting portions of those very documents that weaken—or doom—their claims.” Khoja, 899 F.3d at 1002. Judicial notice, on the other hand, is explicitly permitted by Federal Rule of Evidence 201, and allows a court to take notice of an adjudicative fact if it is “not subject to reasonable dispute.” Fed. R. Evid. 201(b).

In Khoja, the Ninth Circuit noted the “concerning pattern” of courts improperly using these procedures in securities cases “to defeat what would otherwise constitute adequately stated claims at the pleading stage,” and “aim[ed] to clarify when it is proper to take judicial notice of facts in documents, or to incorporate by reference documents into a complaint.” 899 F.3d at 998, 999. The district court in Khoja considered twenty-one documents quoted or referenced by the complaint, and granted the defendant’s motion to dismiss the claims plaintiff filed under Sections 10 and 20 of the Exchange Act. Id. at 997. On appeal, the Ninth Circuit reversed in part, holding that the district court had abused its discretion in taking judicial notice of at least one document and in treating at least seven documents as incorporated by reference. Id. at 1018.

Regarding judicial notice under FRE 201, the Court explained that just because a document is subject to judicial notice “does not mean that every assertion of fact within that document is judicially noticeable for its truth.” Id. “‘[A] court may take judicial notice of matters of public record without converting a motion to dismiss into a motion for summary judgment,’” but “‘cannot take judicial notice of disputed facts contained in such public records.’” Id. (quoting Lee v. City of Los Angeles, 250 F.3d 668, 689 (9th Cir. 2001)). For example, in Khoja, the district court had judicially noticed a September 11, 2014 investors’ conference call transcript that was submitted with the defendant’s SEC filings. Khoja, 899 F.3d at 999. The Ninth Circuit explained that the district court could take judicial notice of the existence of the call, but could not take judicial notice of the statements in the transcript, as “the substance of the transcript ‘is subject to varying interpretations, and there is a reasonable dispute as to what the [transcript] establishes.’” Id. at 999-1000 (quoting Reina-Rodriguez v. United States, 655 F.3d 1182, 1193 (9th Cir. 2011)).

Regarding incorporation by reference, the Ninth Circuit explained that a document that “merely creates a defense to the well-pled allegations in the complaint” should not automatically be incorporated by reference. Khoja, 899 F.3d at 1002. A contrary result would enable defendants to “insert their own version of events into the complaint to defeat otherwise cognizable claims.” Id. Applying these principles, the Ninth Circuit held that the district court abused its discretion by incorporating a Wall Street Journal blog post, as the complaint had quoted the post only once in a two-sentence footnote, and the quote conveyed only basic historical facts. Id. at 1003-04. The Khoja court explained that, under its prior precedent in Ritchie, a reference is not “extensive” enough to warrant incorporation by reference when the document is only referenced once, unless that “single reference is relatively lengthy.” Id. The Ninth Circuit held that the mere mention of the Wall Street Journal blog post was insufficient, especially as the document did not form the basis of any claim in the complaint. Id. at 1003. Ultimately, the Ninth Circuit held that the district court abused its discretion by incorporating by reference at least seven documents. Id. at 1018.

It remains to be seen what impact Khoja will have in the Ninth Circuit, as Khoja did not eliminate a defendant’s ability to rely on documents outside the complaint at the motion to dismiss stage. 899 F.3d at 1018 (affirming district court with respect to half of the documents challenged on appeal). Nonetheless, the case may prompt other federal courts to revisit their practices of incorporation by reference and judicial notice, particularly in securities cases where such practices are common.

The following Gibson Dunn lawyers assisted in the preparation of this client update: Jefferson Bell, Monica Loseman, Brian Lutz, Mark Perry, Shireen Barday, Lissa Percopo, Michael Kahn, Emily Riff, Mark Mixon, Jason Hilborn, Alisha Siqueira, Andrew Bernstein, and Kaylie Springer.

Gibson Dunn lawyers are available to assist in addressing any questions you may have regarding these developments. Please contact the Gibson Dunn lawyer with whom you usually work, or any of the following members of the Securities Litigation Practice Group Steering Committee:

Brian M. Lutz – Co-Chair, San Francisco/New York (+1 415-393-8379/+1 212-351-3881, [email protected])

Robert F. Serio – Co-Chair, New York (+1 212-351-3917, [email protected])

Meryl L. Young – Co-Chair, Orange County (+1 949-451-4229, [email protected])

Jefferson Bell – New York (+1 212-351-2395, [email protected])

Jennifer L. Conn – New York (+1 212-351-4086, [email protected])

Thad A. Davis – San Francisco (+1 415-393-8251, [email protected])

Ethan Dettmer – San Francisco (+1 415-393-8292, [email protected])

Barry R. Goldsmith – New York (+1 212-351-2440, [email protected])

Mark A. Kirsch – New York (+1 212-351-2662, [email protected])

Gabrielle Levin – New York (+1 212-351-3901, [email protected])

Monica K. Loseman – Denver (+1 303-298-5784, [email protected])

Jason J. Mendro – Washington, D.C. (+1 202-887-3726, [email protected])

Alex Mircheff – Los Angeles (+1 213-229-7307, [email protected])

Robert C. Walters – Dallas (+1 214-698-3114, [email protected])

Aric H. Wu – New York (+1 212-351-3820, [email protected])

© 2019 Gibson, Dunn & Crutcher LLP

Attorney Advertising: The enclosed materials have been prepared for general informational purposes only and are not intended as legal advice.