January 10, 2019

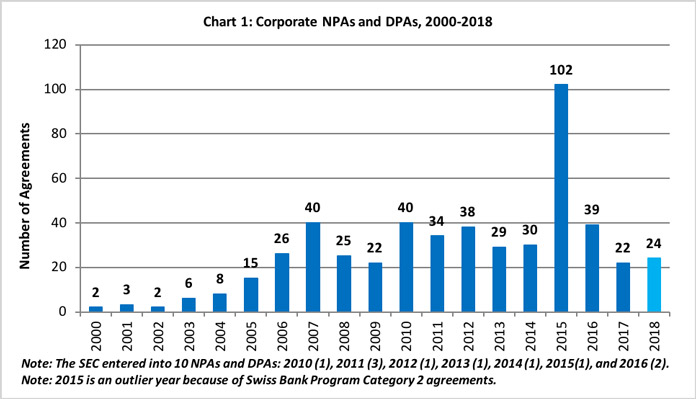

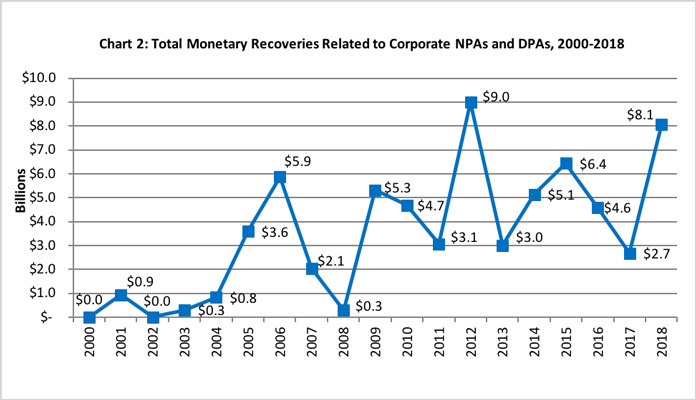

In 2018, the number of corporate non-prosecution agreements (“NPAs”) and deferred prosecution agreements (“DPAs”)[1] in the United States remained steady—2018 yielded at least 24 agreements[2]—but the monetary recoveries skyrocketed to nearly $8.1 billion.[2a] While the comparative year over year analysis has become more difficult because of a third resolution vehicle, declination with disgorgement, the Department of Justice (“DOJ” or “Department”) continues to embrace corporate NPAs and DPAs as effective tools in resolving investigations into corporate criminal misconduct.

This client alert, the twenty-first in our biannual series on NPAs and DPAs: (1) compiles statistics regarding NPAs and DPAs through 2018; (2) highlights important shifts in enforcement agency policy on corporate cooperation; (3) addresses new guidance on imposing and selecting corporate monitors; (4) identifies key provisions in NPAs and DPAs, which may vary depending on the prosecuting authority; (5) analyzes NPAs and DPAs released during the second half of the year; (6) discusses declinations to prosecute that required disgorgement in 2018; and (7) identifies developments in foreign jurisdictions’ use of DPA-style regimes.

NPAs and DPAs in 2018

DOJ entered into at least 24 agreements in 2018, of which 13 are NPAs and 11 are DPAs. The Department also entered into one NPA addendum to address additional conduct without breaching a previously entered NPA, and three declinations that required disgorgement. In contrast, the Securities and Exchange Commission (“SEC” or “Commission”), for the second year in a row, did not enter into any NPAs or DPAs. This year’s 24 agreements exceed the number of agreements in 2017 by two, but represent a decrease from 2016, when there were 39 agreements.

Of note, 14 of the 24 agreements (and the addendum) involved financial institutions, and seven of the 24 agreements resolved allegations arising under the Foreign Corrupt Practice Act (“FCPA”). In addition, two of the agreements executed during the second half of 2018 resolved immigration law allegations related to the employment of foreign workers. Although the natural ebb and flow of resolutions makes broad conclusions from these agreements difficult, we know that DOJ officials continue to emphasize the Department’s commitment to pursuing alleged corporate wrongdoers.

Chart 1 below shows all known corporate NPAs and DPAs from 2000 through 2018.

Monetary recoveries exploded to nearly $8.1 billion, which almost matched the 2012 high of $9 billion. A handful of high-value resolutions led to the large recovery amount.

Chart 2 below illustrates the total monetary recoveries related to NPAs and DPAs from 2000 through 2018.

Corporate Cooperation Redefined

Statements of U.S. Deputy Attorney General Rod J. Rosenstein

On November 29, 2018, U.S. Deputy Attorney General Rod J. Rosenstein announced changes to the Department’s approach to defining corporate cooperation when identifying culpable individuals in corporate investigations.[3] The newly articulated policy, which applies to both criminal and civil corporate cases prosecuted by DOJ, modifies the September 9, 2015 memorandum authored by former Deputy Attorney General Sally Yates (the “Yates Memorandum”). Under the Yates Memorandum, as a prerequisite for any cooperation credit whatsoever, corporations had to identify all individuals responsible for, or involved in, the underlying misconduct and provide all facts pertaining to such misconduct.[4] Under the revised policy, corporate criminal defendants must identify “every individual who was substantially involved in or responsible for the criminal conduct.”[5] Although the revised policy conditions cooperation credit on corporations identifying those who were substantially involved in wrongdoing, the policy also emphasizes that DOJ will not delay resolution of an investigation to gather information on those “whose involvement was not substantial, and who are not likely to be prosecuted.”[6]

The Deputy Attorney General detailed how the revised policy modifies cooperation requirements in the civil context. In contrast to the binary approach to cooperation in criminal matters, the revised policy contemplates a range of cooperation-based outcomes in a civil case. To qualify for maximum credit, corporate civil defendants must still identify every person who was substantially involved in, or responsible for, wrongdoing. But “some credit” is available to corporations that fall short of this standard, provided they “meaningfully assist the government’s civil investigation,”[7] and “identify all wrongdoing by senior officials, including members of senior management or the board of directors.”[8]

The revised policy better harmonizes the Yates Memorandum with directives in the Justice Manual (formerly known as the U.S. Attorney’s Manual) concerning joint-defense agreements. Under the Justice Manual, prosecutors cannot ask corporations to refrain from entering into a joint-defense agreement.[9] Parties to a joint-defense agreement are often prevented from sharing information derived from internal investigations. The Justice Manual states that corporations in joint-defense agreements may nevertheless wish to tailor their agreements to allow them to provide “some relevant facts to the government” to remain eligible for cooperation credit. But merely providing “some relevant facts” falls short of the “all relevant facts” threshold under the Yates Memorandum. By emphasizing that corporations need only identify individuals who were substantially involved in or responsible for wrongdoing, the revised policy is congruent with the “some relevant facts” standard for cooperation credit in the Justice Manual.

The History of Prosecution Policy and DOJ’s Increasing Focus on Cooperation

The new policy represents a recalibration of the Department’s approach to corporate cooperation, but it is not a wholesale reversal of the Yates Memorandum. The policy continues to focus on identifying misconduct at the managerial levels of the corporate hierarchy. The Deputy Attorney General emphasized in his speech announcing the policy that the “most important aspect” of the new policy in the civil context is that corporations “must identify all wrongdoing by senior officials, including members of senior management or the board of directors.”[10]

A natural consequence of the Department’s focus on individual accountability has been to incentivize corporate cooperation in identifying culpable individuals. In doing so, the Department has elevated the importance of cooperation credit in negotiating criminal and civil resolutions, while ostensibly reducing the significance of an effective, pre-existing compliance program as a mitigating factor. This shift in emphasis is seen in DOJ’s history of prosecution policy, which we outline below.

In 1991, Congress took the groundbreaking step of enacting the Federal Sentencing Guidelines for Organizations (“Organizational Guidelines”), which provide a detailed set of sentencing principles whose twin objectives are the prevention and detection of corporate crime. Employing a “carrot and stick” approach, the Organizational Guidelines contemplate severe fines imposed on corporations that promote or show indifference toward wrongdoing while drastically reducing fines on companies that actively seek to prevent and discourage illegal activity. The Organizational Guidelines’ “carrot” (in the form of fine reductions) to incentivize good corporate behavior could be awarded for either or both (1) “self-reporting, cooperation, or acceptance of responsibility,” or (2) “the existence of an effective compliance and ethics program.” The Organizational Guidelines are clear that credit for an effective compliance program can be awarded separate and apart from cooperation.[11]

Starting in 1999 with the Holder Memorandum authored by then-Deputy Attorney General Eric Holder, DOJ issued a series of eponymous policy memoranda attempting to guide the exercise of federal prosecutors’ considerable discretion in the pursuit of corporate actors. Consistent with the Organizational Guidelines, the Holder Memorandum emphasized both cooperation and the effectiveness of a company’s compliance program as mitigating considerations in DOJ’s charging calculus. These two mitigating factors are featured in the Thompson Memorandum (2003), the McNulty Memorandum (2007), the Morford Memorandum (2008), and the Filip Memorandum (2008), each of which pronounced new or revised prosecution guidelines. They also are required considerations in the Justice Manual as part of a prosecutor’s decision to bring charges.

The Yates Memorandum is the sixth iteration of namesake policy documents modifying prosecutors’ charging analysis. The Yates Memorandum sent waves across the defense bar by affirmatively requiring prosecutors to pursue individual defendants from the inception of a corporate investigation. Perhaps less noticed is the Yates Memorandum’s silence regarding the benefits of an effective compliance program, which was featured prominently in every preceding policy memorandum. To be sure, the Yates Memorandum was intended to expound on what gives rise to cooperation credit, so it naturally does not address what mitigating consideration DOJ affords an effective compliance program under the Justice Manual, seemingly leaving undisturbed the mitigating credit derived from an effective compliance program. Regardless, the Yates Memorandum marked the beginning of DOJ policy pronouncements that focus so heavily on cooperation that they appear to obscure and risk devaluing the status of an effective compliance program as a mitigating factor in DOJ’s charging calculus.

This phenomenon looms large in the FCPA Pilot Program, which was adopted as the FCPA Corporate Enforcement Policy in November 2017. The policy explicitly aims to incentivize companies’ behavior “once they learn of misconduct” by offering declinations or penalty reductions to those companies that self-disclose, cooperate, and remediate. In other words, a company’s compliance program, as it existed before the occurrence of any wrongdoing, is not a required consideration that favors declination or penalty reductions under the FCPA Corporate Enforcement Policy. To receive cooperation credit for voluntary self-disclosure under the policy, an organization must provide, in a fashion similar to the Yates Memorandum, “all relevant facts known to it, including all relevant facts about all individuals involved in the violation of law”—a requirement that now appears to be at odds with the Department’s recent recognition that identifying all individuals involved in wrongdoing is inefficient and needlessly delays resolutions.

Practical Implications of the Department’s Revised Policy

The Department’s revised policy defining corporate cooperation will have practical implications on corporate investigations that are likely to enhance information sharing with DOJ. Since the Filip Memorandum’s release, the Justice Manual has prohibited prosecutors from affirmatively seeking waiver of attorney-client privilege and protected work product. Nevertheless, because companies often conduct investigations with the assistance and advice of counsel, they have not always been able to furnish “all relevant facts” to DOJ absent some form of waiver. The revised policy, by more narrowly focusing on those with substantial involvement in wrongdoing, likely will reduce the number of instances companies will face dueling priorities of protecting privilege versus cooperating with DOJ.

Developments in Corporate Monitorships

A compliance monitorship is often a condition of resolving a corporate investigation or prosecution with enforcement authorities. Because monitorships can be time consuming, costly, and intrusive, it is important for companies to understand what the government considers when evaluating the necessity of a monitor, and how the government selects the individual monitor. In 2018, the government issued guidance addressing both of those points.

The Benczkowski Memorandum

On October 12, 2018, Assistant Attorney General Brian A. Benczkowski announced the publication of new guidance on the imposition and selection of monitors in conjunction with corporate resolutions in Criminal Division matters (the “Benczkowski Memorandum”).[12] The Department promulgated the Benczkowski Memorandum to supplement the 2008 guidance from then-Acting Deputy Attorney General Craig S. Morford (the “Morford Memorandum”),[13] and “to further refine the factors that go into the determination of whether a monitor is needed, as well as clarify and refine the monitor selection process.”[14] Although the Benczkowski Memorandum technically applies only to the Criminal Division, its practical effect is much broader, both because the Criminal Division is almost always involved in significant corporate resolutions and because the Criminal Division’s policies tend to serve as a bellwether for wider Department efforts.

- Imposition of a Monitor

The Benczkowski Memorandum reiterates the “foundational principle” that imposition of a corporate monitor is not meant to be punitive, but rather aims to deter future misconduct.[15] In his speech announcing the new guidance, Benczkowski noted that for the past five years, only one in three corporate resolutions involved a corporate monitorship—the majority of corporate resolutions did not require monitors.[16] The Benczkowski Memorandum reiterates the Morford Memorandum’s pronouncement that prosecutors, when considering the need for a monitor, should assess “(1) the potential benefits that employing a monitor may have for the corporation and the public, and (2) the cost of a monitor and its impact on the operations of a corporation.”[17]

The Benczkowski Memorandum articulates the following factors for consideration when evaluating the “potential benefits” of a monitor: (1) the type of misconduct (i.e., whether it involved manipulation of corporate books and records or exploitation of an inadequate system of internal controls); (2) the pervasiveness of the misconduct, and whether it was approved or facilitated by senior management; (3) the company’s investments in, and improvements to, its corporate compliance program and internal control systems; and (4) whether remedial improvements to the compliance program and internal controls have been tested to demonstrate effective deterrence.[18] In other words, a robust internal compliance system may move the needle toward a resolution without a monitor requirement. The calculus of whether to impose a monitor accounts for proactive steps taken by the company to prevent or remediate wrongdoing; therefore, maintaining an effective and well-resourced compliance department and/or retaining an independent compliance consultant as soon as wrongdoing is detected may mitigate the likelihood of a monitorship.

The ultimate decision of whether to require a monitor weighs the projected costs of the monitorship (both monetary costs and burden on the company’s operations) against the clear benefit derived from it. The explicit statement that DOJ will consider financial costs signals that DOJ is receptive to concerns voiced by corporations and the white collar bar regarding the heavy financial burden caused by monitorships. Costs of a monitor include not only professional fees, but also the operational costs of employee time devoted to working with the monitor and responding to requests for documentation. The Benczkowski Memorandum acknowledges these costs and requires consideration of them in deciding whether a monitor is appropriate. Within the Criminal Division, attorneys handling a matter must seek and obtain approval from their supervisors and obtain the concurrence of the Assistant Attorney General of the Criminal Division or his or her designee prior to imposing a monitor.

- Selection of a Monitor

In cases where a monitorship is warranted, the Benczkowski Memorandum outlines procedures for initial selection—and, if necessary, replacement—of the corporate monitor. As an initial step, the company may recommend three qualified candidates and identify one as the top choice. A “qualified candidate” is defined by his or her (1) general background, education, experience, and reputation; (2) substantive expertise in the particular area(s) at issue; (3) ability to be objective and independent; and (4) access to adequate resources to effectively discharge his or her responsibilities. Within 20 days of the execution of a qualifying agreement (e.g., NPA, DPA, or plea agreement), the company should provide a written proposal outlining each candidate’s qualifications and credentials, and certifying that the proposed candidates are not employed by or affiliated with the company and will not be employed by or affiliated with the company for at least two years following the termination of the monitorship. The written statement should also certify that the company has reviewed potential conflicts with clients of the monitor candidate and resolved conflicts where applicable. The procedures formalize the selection process, although the practice of companies recommending monitor candidates is not new.[19]

Following submission of the written statement from the company, the Criminal Division will review the candidates’ experience, credentials, and expertise in the particular matters at issue, and assess whether the candidates have sufficient resources to carry out monitorship responsibilities effectively. The attorneys will then determine which monitor candidate(s) to recommend to the Standing Committee on the Selection of Monitors (“Standing Committee”). Absent from the Benczkowski Memorandum is reference to DOJ’s “commitment to diversity and inclusion” in selecting a compliance monitor, which was—as we discussed in our 2018 Mid-Year Update—a stated consideration for selecting a monitor highlighted in the Panasonic Avionics Corporation (“PAC”) DPA. PAC had agreed to pay $280 million and to a two-year monitorship in a foreign bribery settlement with DOJ and the SEC in April 2018.[20]

The Standing Committee, as described in the Benczkowski Memorandum, includes the Deputy Assistant Attorney General with supervisory responsibility for the Fraud Section (or his or her designee), the Chief of the Fraud Section or other relevant section (or his or her designee), and the Deputy Designated Agency Ethics Official for the Criminal Division.[21] The Criminal Division attorneys handling a matter where a monitor is imposed will provide the Standing Committee with a memorandum describing the case, explaining why a monitor is required, and setting forth the proposed and recommended candidates. The Standing Committee will then review and vote on whether to accept the recommendation. Following the vote, the Office of the Deputy Attorney General will review the recommendation of the Standing Committee and determine whether to grant final approval of the proposed monitor.

The paramount goal of this robust selection process is the appointment of a highly qualified, suitable, and conflict-free monitor who will instill public confidence in the monitorship process.[22] Since the release of the Benczkowski Memorandum, no resolutions have mandated monitorships, and it is difficult to meaningfully assess the memorandum’s impact. Some view the Benczkowski Memorandum as “business-friendly” and restrictive to prosecutors; they assert that the Trump Administration has blunted enforcement tools like corporate monitorships.[23] When announcing the new guidance, Benczkowski reiterated that imposition of a monitorship should be “the exception, not the rule.”[24] Although the Benczkowski Memorandum requires weighing the potential benefits of a monitor against the financial and operational costs, the prosecutor still retains discretion when making the determination. It remains to be seen whether the guidance will, in practice, reduce the use of monitorships in corporate settlements. We will continue to track how the Benczkowski Memorandum impacts both the number of monitorships imposed in corporate resolutions and the selection of individuals as monitors.

Corporate Resolution Extensions

The conclusion and extension of corporate resolutions in 2018 highlight the challenges some corporations face even after a resolution is reached. MoneyGram International, Inc. (“MoneyGram”) extended its DPA seven times in 2018 (and once in late 2017),[25] most recently through May 10, 2021, and agreed to forfeit an additional $125 million.[26] MoneyGram’s DPA, originally signed in 2012, resolved allegations that MoneyGram failed to maintain an effective anti-money laundering (“AML”) program and that its agents were complicit in alleged consumer fraud schemes. Under the DPA, MoneyGram agreed to implement significant compliance measures, including changes to executive compensation, a remediation due diligence plan related to agents, a risk-based transaction monitoring program, and the designation of at least one AML compliance officer to each high risk country.[27]

Standard Chartered Bank (“Standard Chartered”) also extended its DPA, and the length of the related monitorship, four times.[28] Standard Chartered entered a two-year DPA in 2012 to resolve allegations of facilitating payments involving Burma, Iran, Libya, and Sudan in violation of U.S. sanctions laws.[29] Standard Chartered’s commitments in its 2012 DPA included continued “cooperation with the United States” (as defined in the agreement), as well as “full compliance” with certain AML best practices recommended by third parties.[30] Standard Chartered noted that it continues to cooperate in an ongoing sanctions-related investigation, and the company has “taken a number of steps and made significant progress” with respect to compliance, but its sanctions compliance program “has not yet reached the standard required by the DPA.”[31] Standard Chartered most recently extended the DPA term until March 31, 2019, noting that the “vast majority of the issues under investigation pre-date 2012,” and the company is “engaged in constructive discussions with relevant authorities to resolve the investigation as soon as practicable.”[32]

These DPA extensions underscore the long resolution process that can await companies after entering into a DPA. Particularly in complex areas, such as AML and sanctions compliance, companies must devote substantial resources and technical sophistication to implement the compliance enhancements required under their DPAs.

Key Provisions in Corporate Resolutions

Because DOJ has not issued a standard template for NPAs and DPAs, there is substantial variety in the salient terms of these resolution vehicles. The variety is evident across agreements signed by different divisions of DOJ and the 93 Offices of the U.S. Attorneys—core terms may vary depending on which prosecutor’s office drafts the resolution. For example, the U.S. Attorney’s Office for the Southern District of New York often mandates forfeiture of accounts in DPAs. This practice is unique from NPA and DPA structures in other U.S. Attorney’s Offices, and is followed irregularly at Main Justice. Accordingly, when negotiating terms of NPAs and DPAs, it is important to focus on the substantive elements, including the following: (1) duration of the agreement (typically ranges from 12 to 48 months); (2) entities covered by the resolution (parents, subsidiaries, affiliates, and/or joint venture partners); (3) release language (may encompass a specific, alleged crime or all disclosed conduct by the putative defendant to DOJ); (4) what constitutes breach (material violation of law, violation of the agreement, or violation of the statute underlying the resolution); (5) cure for breach (extension of the agreement, revocation of the agreement followed by a plea of guilty, or monetary liquidated damages, as seen in the Netcracker Technology Corporation NPA discussed in our 2017 Year-End Update); and (6) post-agreement reporting obligations (monitorship, self-reporting, annual self-assessment report, or nothing). The diversity of terms is illustrated in our discussion of recent NPAs and DPAs in the subsequent section.

Recent NPAs and DPAs

Since the publication of our 2018 Mid-Year Update, DOJ has announced 12 NPAs and DPAs, bringing the total to 24 agreements in 2018. The Department also issued one NPA addendum. In July, we discussed the six NPAs and six DPAs announced between January 1, 2018 and July 10, 2018. Those agreements resolved a wide range of allegations, which most prominently related to the FCPA, Racketeer Influenced and Corrupt Organizations Act, money laundering, and wire fraud. Most of the 12 agreements are in effect for terms of 12, 24, or 36 months, and a majority require self-reporting. You can find a summary of the agreements in the Appendix to this publication or read about them in detail in our 2018 Mid-Year Update.

As noted in our statistics of this year’s NPAs and DPAs, more than half of the agreements involved financial institutions, seven of which (and the addendum) were executed during the second half of 2018. Our Developments in the Defense of Financial Institutions publication discusses some of the larger settlements in detail and provides insight into the legal complexities of the industry. In addition to the government’s distinct focus on financial institutions, two of the agreements announced since July 10 resolved allegations related to the employment of foreign workers. We discuss the key provisions of each agreement announced during the second half of 2018 below.

American Media, Inc. (NPA)

On December 12, 2018, the U.S. Attorney’s Office for the Southern District of New York announced that it entered into an NPA with American Media, Inc. (“AMI”) on September 20, 2018.[33] The U.S. Attorney’s Office made the announcement in conjunction with the sentencing of Michael Cohen, who, in relevant part, violated campaign finance laws when he facilitated two payments to women to prevent the public disclosure of alleged affairs with then-presidential candidate Donald Trump.[34] Cohen allegedly used AMI to make a $150,000 payment to one of the women.[35]

In the NPA, the U.S. Attorney’s Office acknowledged AMI’s “cooperation and implementation of remedial measures” as principal factors in its decision to forgo criminal prosecution.[36] AMI agreed to cooperate with government officials and its obligations under the NPA will continue until the later of three years or “the date on which all prosecutions arising out of the conduct described in the opening paragraph of this Agreement are final.”[37] As part of its remedial duties, AMI agreed to provide employees with written standards covering federal election laws, conduct annual, mandatory training on the written standards, and work with “counsel knowledgeable in the field of federal election law” to advise on the written standards and ensure that “payments to acquire stories involving individuals running for office” comply with the written policies.[38] In addition, AMI must report to the U.S. Attorney’s Office any violations of its written standards or federal election law during the term of the agreement.[39] The NPA did not impose a monetary penalty.

Bank Lombard Odier & Co Ltd. (NPA addendum)

On July 31, 2018, Bank Lombard Odier & Co Ltd. (“Bank Lombard”) entered into an addendum to the NPA it signed on December 31, 2015, with DOJ.[40] The original NPA arose from Bank Lombard’s disclosure of its cross-border business for U.S.-related accounts as part of the Swiss Bank Program established by DOJ on August 29, 2013.[41] This addendum to an NPA is unusual; it is likely the result of the unique nature of the NPAs associated with the Swiss Bank Program.

The Swiss Bank Program provided a path for Swiss banks to resolve potential U.S. criminal liabilities related to tax evasion.[42] To enter the program, Swiss banks were required to advise DOJ by December 31, 2013, that they had reason to believe that they had committed tax-related criminal offenses in connection with undeclared U.S.-related accounts.[43] To be eligible, banks had to (1) make a complete disclosure of their cross-border activities; (2) provide detailed information on an account-by-account basis in which U.S. taxpayers had a direct or indirect interest; (3) cooperate in treaty requests for account information; (4) provide detailed information as to other banks that transferred funds into secret accounts or that accepted funds when secret accounts were closed; (5) agree to close accounts of accountholders who fail to come into compliance with U.S. reporting obligations; and (6) pay appropriate penalties.[44] Swiss banks meeting all of these requirements were eligible for an NPA.[45] Bank Lombard entered into an NPA under the Swiss Bank Program on December 31, 2015.[46]

After entering into the original NPA—which required Bank Lombard to disclose all of its U.S.-related accounts that were open at each bank between August 1, 2008 and December 31, 2014—Bank Lombard self-disclosed that it was “aware of or should have been aware of” additional U.S.-related accounts at the time it entered into the original NPA.[47] DOJ acknowledged Bank Lombard’s early self-disclosure of the additional accounts and its full cooperation under the Swiss Bank Program.[48] Under the terms of the addendum, Bank Lombard agreed to pay an additional sum of $5.3 million calculated in accordance with the terms of the Swiss Bank Program.[49] The term of Bank Lombard’s obligations under the original NPA (four years) was not extended by the addendum.[50]

Basler Kantonalbank (DPA)

On August 28, 2018, Basler Kantonalbank (“BKB”), a bank headquartered in Basel, Switzerland, entered into a three-year DPA with DOJ’s Tax Division and the U.S. Attorney’s Office for the Southern District of Florida.[51] The DPA resolved a seven-year investigation into the bank by U.S. authorities, which emerged from a U.S. crackdown on offshore tax evasion by wealthy Americans utilizing undeclared Swiss bank accounts.

As part of the DPA, BKB admitted that between 2002 and 2012 it conspired with its employees, external asset managers, and clients to: (1) defraud the United States with respect to taxes; (2) commit tax evasion; and (3) file false federal tax returns.[52] The bank assisted certain U.S. clients in concealing their offshore assets and income from U.S. tax authorities. By 2010, when BKB’s U.S.-related business was at its peak, the bank held approximately 1,144 accounts for U.S. customers, with an aggregate value of approximately $813.2 million. Many, but not all, of these accounts were undeclared and part of the conspiracy to defraud the United States.[53]

BKB agreed to pay $60.4 million in total penalties. First, BKB agreed to pay $17.2 million in restitution to the Internal Revenue Service (“IRS”), which represents the unpaid taxes resulting from BKB’s participation in the conspiracy. Second, BKB agreed to forfeit $29.7 million to the United States, which represents gross fees (not profits) that the bank earned on its undeclared accounts between 2002 and 2012. Finally, BKB agreed to pay a fine of $13.5 million.[54]

DOJ explained that the penalty amount reflected BKB’s thorough internal investigation and cooperation with the United States, as well as the bank’s extensive remedial efforts.[55] In particular, BKB demonstrated its acceptance and acknowledgment of responsibility for its conduct by, among other things: (1) advocating for a decision by the Swiss Federal Council in April 2012 to allow banks under investigation by DOJ to legally produce employee and third-party information to DOJ; (2) quickly producing such information after the Swiss Federal Council decision; (3) providing the government with the broadest scope of information permissible under Swiss law; and (4) disclosing facts, including unfavorable ones, discovered during the course of its investigation.[56] DOJ also credited BKB for waiving any potential defense of foreign sovereign immunity, which may have protected BKB as a state-guaranteed, semi-governmental organization.

Central States Capital Markets, LLC (DPA)

On December 10, 2018, Central States Capital Markets, LLC (“CSCM”) and the U.S. Attorney’s Office for the Southern District of New York entered into a DPA to resolve allegations that CSCM failed to timely file a Suspicious Activity Report in violation of the Bank Secrecy Act (“BSA”).[57] CSCM agreed to accept responsibility for the allegations and forfeited $400,000 to the United States, which “represents a substitute res” for monies processed by CSCM[58] relating to payday lending fraud executed by a customer.[59] CSCM agreed to cooperate with the government’s investigation, and self-disclose all criminal conduct related to violations of federal law.[60] As part of its remediation efforts, the DPA requires CSCM to implement and maintain an effective BSA/AML compliance program, as well as “retain an independent consultant on the terms and conditions set by the SEC.”[61] The term of the DPA is two years.[62]

Of note, this is the first criminal BSA charge brought against a U.S. broker-dealer.[63] In his announcement of the DPA, U.S. Attorney Geoffrey S. Berman stated that the charge “makes clear that all actors governed by the [BSA]—not only banks—must uphold their obligations to protect our economy from exploitation by fraudsters and thieves.”[64]

Hallman Chevrolet (DPA)

On August 31, 2018, DOJ announced that the U.S. Attorney’s Office for the Western District of Pennsylvania had entered into a four-year DPA with Hallman Chevrolet, a car dealership located in Erie, Pennsylvania.[65] The DPA resolved allegations that Hallman Chevrolet engaged in a bank fraud scheme and a conspiracy to commit bank fraud. In particular, Hallman Chevrolet engaged in a fraudulent down payment scheme by manipulating bills of sale and bank lending contracts to hide from financial institutions the true source of customer down payments and to make customers appear more credit-worthy than they actually were. As a result, Hallman Chevrolet led the financial institutions into making unsafe investment decisions by having under-collateralized assets and financially risky credit applicants.[66]

Pursuant to the DPA, Hallman Chevrolet agreed to pay a monetary penalty of $1.4 million and more than $737,000 in restitution to various lending institutions. In addition, “Hallman Chevrolet must engage in a substantial corporate compliance and ethics program and a vigorous monitoring and audit regime.”[67]

Health Management Associates, LLC (NPA)

Health Management Associates, LLC (“HMA”) entered into an NPA with the Fraud Section on September 21, 2018, to resolve criminal and civil claims relating to “a formal and aggressive plan to improperly increase overall emergency department inpatient admissions at all HMA hospitals.”[68] Specifically, DOJ alleged that HMA executives and hospital administrators pressured, coerced, and induced physicians and medical directors to meet mandatory admission rate benchmarks and admit patients who did not need inpatient treatment.[69] The NPA notes that a “relevant consideration” for entering into an NPA was that the parent company of HMA—Community Health Systems (“CHS”)—acquired HMA after the relevant behavior had occurred, and at the time of acquisition HMA was facing multiple lawsuits and was the subject of criminal and civil investigations.[70] The NPA also notes that following the acquisition of HMA, CHS “engaged in remedial measures, including (1) removing the HMA Board of Directors and senior executives; and (2) integrating the HMA hospitals into [CHS’s] compliance program and implementing certain compliance initiatives to address and remediate . . . [the] issues that were alleged in certain . . . lawsuits and were part of the criminal and civil investigations.”[71]

HMA and CHS also received credit for their cooperation with the Fraud Section, which included, among other things, making regular factual presentations; collecting, analyzing, and organizing voluminous evidence and information for the Fraud Section; and providing substantial cooperation to the U.S. Attorney’s Office for the Middle District of Florida in connection with the prosecution of a former HMA executive.[72]

Under the NPA, which has a term of three years, HMA agreed to cooperate with the investigation, report allegations or evidence of violations of federal health care offenses, ensure that its compliance and ethics program satisfies the requirements of an amended and extended Corporate Integrity Agreement, and report annually to the Fraud Section regarding remediation and implementation of compliance measures.[73] HMA also agreed to pay a monetary penalty in the amount of over $35 million.[74]

The NPA notes that HMA and CHS agreed to a global resolution of HMA’s civil and criminal liability. An indirect subsidiary of HMA, Carlisle HMA, LLC, pleaded guilty to one count of conspiracy to commit health care fraud and agreed to pay a criminal fine of over $2.5 million.[75] HMA also agreed to pay almost $75 million to resolve civil claims arising under federal and state False Claims Acts,[76] and over $148 million to settle qui tam allegations that HMA hospitals provided improper financial incentives to physicians for patient referrals.[77]

Mirelis Holding S.A. (NPA)

Mirelis Holding S.A. (“Mirelis”), a Swiss financial asset and management firm, entered into an NPA with DOJ’s Tax Division on July 24, 2018, to resolve allegations related to facilitating U.S.-based tax evasion.[78] DOJ alleged that Mirelis opened, maintained, and serviced accounts for U.S. taxpayer-clients where Mirelis knew or had reason to know that the U.S. taxpayer-clients were not complying with their U.S. tax obligations.[79] Mirelis originally submitted a Letter of Intent on December 23, 2013, to participate in DOJ’s Swiss Bank Program, but it was ultimately determined that Mirelis did not qualify due to its structure as both an asset management firm and a bank.[80] However, the NPA entered into on July 24, 2018, requires Mirelis to fully comply with the obligations imposed under the terms of the program.[81] Additionally, the NPA requires Mirelis to provide transaction information related to certain accounts, close as soon as practicable any U.S.-related dormant accounts, and pay a sum of $10.245 million.[82]

The NPA characterized the $10.245 million as $3.245 million in restitution for the approximate pecuniary loss suffered by the United States, $5 million as disgorgement of profits for the approximate amount earned by Mirelis by servicing undeclared U.S. taxpayers, and $2 million as a penalty for Mirelis’s conduct with respect to U.S.-related accounts.[83] In support of the agreement not to prosecute Mirelis, DOJ cited Mirelis’s voluntary disclosure of its conduct, cooperation with the Tax Division on the status and findings of its internal investigation, and retention of a qualified independent examiner who verified the information Mirelis disclosed, pursuant to the requirement under the Swiss Bank Program.[84] The NPA has a term of four years.[85]

Neue Privat Bank AG (NPA)

On July 18, 2018, the Tax Division announced an NPA with Neue Privat Bank AG (“NPB”), stemming from NPB’s cross-border business, which allegedly ran afoul of U.S. tax law.[86] NPB, a private Swiss bank, must pay a $5 million penalty for aiding U.S. clients in concealing assets and income from the IRS.[87] In 2009, NPB’s Board voted to allow U.S. clients to open accounts at the bank, even when the clients had been forced out of other banks.[88] NPB’s assets under management for U.S. clients subsequently jumped to 450 million Swiss Francs from 8 million Swiss Francs the previous year.[89] Most of NPB’s U.S. client accounts were managed by external asset managers and firms, and NPB had very little contact with many of its clients.[90] For some of those clients, NPB did not disclose the account owner’s identity to the IRS.[91]

NPB believed it could maintain its U.S. accounts, even if it knew or had reason to believe the accounts were to evade taxes, and indeed continued to service some of those accounts after knowledge that some owners had not declared their accounts to the IRS.[92] NPB serviced accounts that employed different strategies to conceal income from the IRS, including using numbered accounts, hold mail services, and shell companies.[93] NPB began to increase its U.S. tax compliance efforts in 2010 and 2011, requiring tax compliance evidence from external asset managers in August 2011, but it still continued to maintain undeclared accounts.[94] NPB cooperated in the investigation by disclosing the identities of account holders and making bank executives available for interview.[95] NPB must comply with periodic reporting if it fails to close dormant accounts.[96] The NPA was set for a term of four years.[97]

Petróleo Brasileiro S.A. – Petrobras (NPA)

On September 26, 2018, the Fraud Section and the U.S. Attorney’s Office for the Eastern District of Virginia announced an NPA with Petróleo Brasileiro S.A. – Petrobras (“Petrobras”), resolving allegations arising under the FCPA.[98] Petrobras, the Brazilian semi-public, state-run energy company, agreed to pay $170.64 million to U.S. authorities, with credit for $682.56 million paid to Brazilian authorities after Brazilian and U.S. investigations into the company’s internal controls, books and records, and financial statements.[99]

As discussed in greater detail in our 2018 Year-End FCPA Update, certain former Petrobras executives engaged in a corrupt scheme with politicians and Petrobras suppliers and contractors.[101] Petrobras reached settlements with both DOJ and the SEC. DOJ agreed to credit payments to the SEC and the Brazilian government to the overall penalty, such that DOJ and the SEC each receive 10% of the total penalty ($85.32 million) and the Brazilian government, which has not found wrongdoing by Petrobras, will receive the remaining 80% ($682.56 million).[102] In the related SEC settlement, the SEC will credit any amounts Petrobras pays in the shareholder derivative suit against the SEC’s order of approximately $933.473 million in disgorgement and prejudgment interest.[103]

Although Petrobras did not voluntarily disclose the underlying conduct, it fully cooperated in the investigation by conducting a thorough internal investigation, sharing findings of that investigation with the government in real time, and presenting regularly to the government.[104] Petrobras also took significant remedial measures, including replacing its Board of Directors and a number of high-level executives, completely revamping its internal governance systems, and terminating and distancing itself from any employee implicated in the alleged bribery scheme.[105] DOJ will not require an independent compliance monitor.[106] Petrobras will, however, be required to report to DOJ every 12 months on its remedial measures over the course of the agreement, including the implementation of its internal governance systems.[107] The NPA has a term of three years.[108]

Société Générale S.A. (DPA)

On November 18, 2018, Société Générale S.A. (“SocGen”) and the U.S. Attorney’s Office for the Southern District of New York entered a DPA to resolve allegations involving the Trading with the Enemy Act (“TWEA”) and the Cuban Assets Control Regulations (“Cuban Regulations”) promulgated thereunder.[109] The DPA term is three years, and it requires SocGen to pay over $1.34 billion, including $717.2 million in forfeiture to the United States.[110] The remaining portion of the monetary penalty consists of payments to be made for SocGen’s concurrent settlement of related criminal and civil actions with the New York County District Attorney’s Office, the U.S. Department of Treasury, Office of Foreign Assets Control (“OFAC”), the New York State Department of Financial Services, and the Federal Reserve Board of Governors and the Federal Reserve Bank of New York. The $1.34 billion in penalties represents the second largest penalty ever imposed on a financial institution for violations of U.S. economic sanctions.[111]

DOJ charged SocGen with violations of the TWEA and the Cuban Regulations, alleging that SocGen participated in a conspiracy, which lasted from about 2004 to 2010, to make transfers of credit and payments between, by, and through banking institutions with respect to property in which Cuba had an interest.[112] Specifically, DOJ alleged that SocGen structured U.S. dollar transactions and operated 21 credit facilities that provided significant money flow to Cuban banks, entities controlled by Cuba, and Cuban and foreign corporations for business conducted in Cuba.[113] In total, SocGen allegedly engaged in more than 2,500 transactions through U.S. financial institutions that caused those institutions to process close to $13 billion in transactions that otherwise should have been blocked for investigation pursuant to OFAC regulations.[114]

DOJ alleges that SocGen’s management and Group Compliance failed to disclose the discovered conduct to OFAC promptly.[115] Demonstrating good faith and cooperation, SocGen agreed, as part of the DPA, to implement remedial measures required by various state and federal regulators.[116] Specifically, SocGen agreed to implement or enhance its BSA/AML compliance programs and internal controls to prevent the occurrence of similar criminal conduct going forward.[117]

Waste Management of Texas (NPA)

On August 29, 2018, the U.S. Attorney’s Office for the Southern District of Texas entered into an NPA with Waste Management of Texas (“Waste Management”).[118] Between 2003 and April 2012, managers at Waste Management’s Afton, Texas, location allegedly hired individuals to work at the facility without inquiring into their work status in the United States.[119] In January 2012, after firing ten employees because they were undocumented, the managers provided the fired individuals with identification documents of other, documented people so that they could return to work at Waste Management.[120] The three managers were indicted in May 2014 for the above conduct, and Waste Management both cooperated in the criminal investigation and conducted its own internal investigation.[121] As part of the NPA, Waste Management agreed to continue its already enhanced immigration compliance procedures and forfeit over $5.5 million, which amounts to the estimated proceeds from employing undocumented workers at the Afton facility from 2003 to 2012.[122]

Wright State University (NPA)

On November 16, 2018, Wright State University (“WSU”), a public university, and the U.S. Attorney’s Office for the Southern District of Ohio entered into an NPA in connection with WSU’s admission that it engaged in a conspiracy to commit H-1B visa fraud.[123] The H-1B visa program allows companies in the United States to temporarily employ foreign workers in occupations that require highly specialized knowledge and a bachelor’s or higher degree in a specific specialty. There is a numerical cap on the number of H-1B visas that can be issued per year, but, as an institute of higher learning, WSU is “cap exempt,” unlike other types of organizations.[124]

According to the agreement, WSU employed 24 foreign employees—pursuant to sponsored research contracts with Webyoga, Inc. (“Webyoga”), a privately held software company—through H-1B visas.[125] WSU used its “cap exempt” status to apply for the visas.[126] In doing so, WSU submitted a signed employment offer letter from the university indicating each visa employee would be working for the university and under the supervision of university employees.[127]

In fact, the visa employees worked as consultants on behalf of Webyoga in various cities throughout the country, including Atlanta, Orlando, and New York City.[128] Moreover, WSU invoiced Webyoga for more than $1.8 million in fees associated with the employees’ visas, the employees’ salaries and benefits, and administrative costs for the university.[129] Between 2010 and 2015, WSU also entered into similar arrangements with other companies wherein it would apply for H-1B visas for individuals, the individuals would work on a routine basis for another company, and that company would reimburse the school.[130] WSU acknowledged that the placement of H-1B visa employees with other companies violated the terms of their visa applications, and, as a result, companies who were subject to the numerical H-1B visa limitation were able to use excess H-1B employees through their contracts with WSU.[131]

As part of the NPA, WSU will pay the federal government a $1 million fine in three installments. The NPA will remain in effect for a term of two years or until the date upon which the full monetary payment is made, whichever is later.

Zürcher Kantonalbank (DPA)

On August 7, 2018, Zürcher Kantonalbank (“ZKB”) and the U.S. Attorney’s Office for the Southern District of New York entered a DPA.[132] The U.S. Attorney’s Office announced the filing of charges against ZKB in a press release along with the DOJ Tax Division and the IRS.[133] As part of the DPA, ZKB consented to the filing of a one-count Information charging ZKB with conspiring with others, including U.S. taxpayers, in violation of 18 U.S.C. § 371 to (1) defraud the United States and the IRS; (2) file false federal income tax returns; and (3) evade federal income taxes.[134]

The DPA resolves allegations that from roughly 2002 through 2009, numerous U.S. taxpayer-clients conspired with ZKB to conceal from the IRS the existence of bank accounts held by the U.S. taxpayer-clients at ZKB and the income earned in these accounts in order to evade U.S. taxes on income generated in the undeclared accounts.[135] ZKB allegedly permitted U.S. taxpayer-clients to engage in a number of practices that helped the U.S. taxpayer-clients avoid reporting income to the IRS, including allowing U.S. taxpayer-clients to open undeclared accounts using code names, place assets in undeclared accounts held in the name of sham entities, and make structured withdrawals by checks from undeclared accounts in amounts less than $10,000.[136] DOJ asserts that these practices helped U.S. taxpayers avoid reporting to the IRS accounts and income earned therefrom by ensuring that taxpayer-clients’ names would appear on the fewest possible documents relating to their accounts, concealing the taxpayer-clients’ beneficial ownership of assets in the accounts, and minimizing the size of withdrawal transactions in order to conceal their occurrence from the U.S. authorities.[137]

As a result of this conduct, the DPA requires ZKB to make payments of over $98.5 million to the United States, of which (1) $39.142 million constitutes restitution; (2) over $24.266 million constitutes forfeiture; and (3) over $35.125 million constitutes a penalty.[138] The restitution amount represents the approximate unpaid pecuniary loss to the United States as a result of the concealment of the ZKB taxpayer-clients’ accounts and income earned therefrom. The DPA is set for a term of three years.[139]

Recent Declinations with Disgorgement

In 2018, DOJ agreed to three declinations that require disgorgement under the Department’s FCPA Corporate Enforcement Policy, which it adopted in November 2017. Companies that would otherwise receive NPAs are now entering into declination with disgorgement letters if they meet certain disclosure, cooperation, and remediation criteria. We summarize below the three declination with disgorgement letters from 2018. The agreements notably reiterate the Department’s continued commitment to hold individuals accountable for misconduct.

The Dun & Bradstreet Corporation

On April 23, 2018, the Fraud Section and the U.S. Attorney’s Office for the District of New Jersey declined to prosecute The Dun & Bradstreet Corporation (“Dun & Bradstreet”), a business data and analytics company, for alleged violations of the FCPA bribery provisions committed by the company’s subsidiaries in China.[140] DOJ declined to prosecute due to several factors, including the company’s (1) identification and voluntary disclosure of misconduct; (2) thorough investigation; (3) full cooperation, including the identification of culpable individuals, sharing all related facts, facilitating interviews of current and former employees, and translation of foreign documents; (4) enhancement of internal controls and its compliance program; (5) full remediation, including terminating and disciplining employees; and (6) disgorgement of monies to the SEC.[141]

In its parallel administrative order, the Commission ordered Dun & Bradstreet to pay more than $9 million in disgorged profits, prejudgment interest, and a civil penalty.[142] The order states that the two Chinese subsidiaries allegedly used third parties to make improper payments to obtain non-public financial and personal information in violation of Chinese law.[143] In violation of the FCPA accounting provisions, Dun & Bradstreet allegedly “failed to devise and maintain sufficient internal accounting controls to detect or prevent the improper payments,” and failed to accurately reflect the transactions in its consolidated books and records.[144]

Insurance Corporation of Barbados Limited

On August 23, 2018, the Fraud Section and the U.S. Attorney’s Office for the Eastern District of New York declined to prosecute Insurance Corporation of Barbados Limited (“ICBL”), an insurance company based in Barbados, for alleged violations of the FCPA.[145] The Fraud Section’s investigation determined that ICBL made approximately $36,000 in bribe payments to Barbadian government officials in exchange for insurance contracts.[146] The government official who received the bribes laundered the money through U.S. bank accounts.[147] DOJ declined to prosecute due to several factors, including ICBL’s (1) timely and voluntary disclosure; (2) thorough investigation; (3) cooperation, including the provision of all known, relevant facts and continued cooperation in ongoing DOJ matters; (4) disgorgement of profits related to the misconduct; (5) improvements to its compliance program and internal controls; (6) remedial actions, including termination of involved employees; and (7) DOJ’s ability to identify and charge culpable individuals.[148]

ICBL agreed to disgorge almost $94,000, which represents the profit from the illegally obtained insurance contracts.[149] The company agreed to pay the disgorgement amount to the Treasury Department.[150] The letter states that it does not protect any individuals against prosecution.[151]

Polycom, Inc.

On December 20, 2018, the Fraud Section declined to prosecute Polycom, Inc. (“Polycom”), a communications solutions provider, for alleged violations of the FCPA bribery and accounting provisions caused by the company’s subsidiaries in China.[152] Polycom’s subsidiaries allegedly used local channel partners to make improper payments via a discount scheme in exchange for business contracts.[153] DOJ declined to prosecute after considering several factors, including Polycom’s (1) identification of misconduct; (2) prompt and voluntary disclosure of wrongdoing; (3) thorough investigation; (4) full cooperation, including the provision of all related facts, facilitation of current and former employee interviews, translation of documents, identification of unrelated wrongdoing, and continued cooperation with DOJ’s ongoing investigations or prosecutions; and (5) remedial actions, including enhanced internal controls and compliance programs, employee terminations and discipline, and cutting ties with a channel partner.[154]

As part of the agreement, Polycom agreed to disgorge $30.978 million, which reflects the profit from the illegally obtained contracts.[155] The company will pay the disgorged profits to the SEC, the Treasury Department, and the Postal Inspection Service Consumer Fraud Fund.[156] The declination letter explicitly notes that the agreement does not preclude prosecution of any individuals.[157]

On December 26, 2018, the Commission issued an administrative order to resolve alleged violations of the FCPA accounting provisions by Polycom.[158] As part of the resolution, Polycom agreed to pay over $16 million in disgorged profits ($10,672,926), prejudgment interest ($1,833,410), and a civil penalty ($3,800,000).[159] The Commission settled with Polycom after considering the company’s self-disclosure, cooperation, and remediation.[160] Polycom’s resolutions with DOJ and the Commission bring the total monetary penalty to approximately $36 million.

International DPA Developments

We continue to observe a global trend of adopting and developing DPA frameworks. As we discussed in our 2018 Mid-Year Update, some jurisdictions—for example, the United Kingdom and France—have already executed DPA-like resolutions. Other countries—like Canada and Singapore—have fledgling programs that have yet to be utilized. And still others— for example, Switzerland, Australia, and Poland—are considering proposals to institute similar regimes. These DPA frameworks have all been discussed at length in our 2018 Mid-Year Update. The section below updates this prior analysis with new developments from the United Kingdom, which continues to refine its approach to corporate resolutions and completed the term of its first DPA, and Ireland, which is considering the adoption of a DPA model.

United Kingdom

The U.K. Serious Fraud Office (“SFO”) did not enter into any DPAs in 2018, keeping the total number at four since the United Kingdom established a DPA program in February 2014. Nevertheless, agency officials have made clear that they “are open for business,”[161] with a recent increase in core funding,[162] approximately seventy active investigations as of October 2018,[163] and the completion of the United Kingdom’s first DPA.

- Remarks of SFO Officials

In June 2018, the U.K. Attorney General’s Office named a new Director of the SFO, Lisa Osofsky, who officially assumed the role on August 28, 2018.[164] During her first week on the job, Osofsky delivered remarks at the Cambridge International Symposium on Economic Crime, where she highlighted the importance of “multijurisdictional . . . cooperation to achieve global settlements like Rolls-Royce,”[165] which involved coordination among authorities in the United States, Brazil, and the United Kingdom before reaching a resolution in January 2017. Osofsky has committed to “[w]orking with the newcomers to DPAs,” including France, Argentina, Canada, and Australia, to strengthen the SFO’s international relationships in anticipation of future complex, global resolutions.[166]

Osofsky underscored the importance of remediation in determining whether to offer a DPA to a company under investigation.[167] In addition to evaluating whether “the company engaged in proactive efforts to clean house and to reform” (including implementing “the right controls”), the SFO also assesses a company’s tone at the top, ensuring that the remediation efforts are “backed by demonstrable commitment at the appropriate level.”[168]

Recent remarks from Matthew Wagstaff, Joint Head of Bribery and Corruption at the SFO, echo Osofsky’s emphasis on remediation, while also highlighting the critical importance of cooperation for a company seeking a DPA: “no co-operation means no agreement.”[169] Notably, during a subsequent speech, Wagstaff stated that the SFO may ask companies that wish to cooperate to waive privilege over first-hand, factual accounts.[170] Wagstaff asserted that the SFO will not mandate waiver, but “‘the refusal to do so may well be incompatible with an assertion of a desire to cooperate.'”[171] This statement is significant when coupled with a speech made by Osofsky in which she emphasized “the importance of giving ‘first witness accounts’ to individuals who are later charged with crimes.”[172] She stated that those accounts “are sometimes the very interviews that you do in the course of your internal investigations,” and warned that investigations may result in tension between the assertion of privilege and “what a court believes MUST be provided to a criminal defendant to ensure a fair trial.”[173] She concluded that it “is not cooperation” to “blunder into this and then be distressed and offended if we seek those interviews because a court wants us . . . to provide this material to a defendant in the dock.”[174] Although the SFO does not provide formal guidance to assist companies that are looking to cooperate or self-report—and former Director David Green famously said that the SFO does not “do guidance”[175]—Osofsky has signaled that such guidance may be forthcoming to assist companies that “want to understand what cooperation would look like in the context of [the SFO’s] assessment for a DPA.”[176]

- Expiration of the Standard Bank PLC DPA

On November 30, 2018, the SFO announced that Standard Bank PLC (now ICBC Standard Bank PLC) (“Standard Bank”) had fully complied with the terms of its DPA, marking the successful completion of the SFO’s first-ever DPA.[177] The SFO entered into a DPA with Standard Bank in November 2015 to resolve allegations of an approximately $6 million payment made by a former subsidiary of Standard Bank to a local entity controlled by Tanzanian government officials.[178] Standard Bank uncovered evidence of potential wrongdoing and self-reported to the SFO in April 2013.[179] The press release announcing the end of the DPA states that the SFO will publish (on its website) a “‘Details of Compliance’ outlining how Standard Bank” met the terms of the DPA.[180]

- Review of the U.K. Bribery Act

In addition to the work conducted by the SFO, the House of Lords appointed an ad hoc Select Committee to review and report on the effectiveness of the United Kingdom’s 2010 Bribery Act (“Bribery Act Committee”), with a focus on the impact of DPAs on corporate conduct.[181] Over the last several months, a number of prominent U.K. enforcement officials have appeared before the Bribery Act Committee, including Osofsky; Max Hill QC, Director of Public Prosecutions at the Crown Prosecution Service; and Hannah von Dadelszen, Head of Fraud at the SFO.[182]

During a Bribery Act Committee session last fall, von Dadelszen provided insight into the SFO’s decision-making process behind whether to offer a DPA. Von Dadelszen reiterated the requirement of cooperation, and emphasized the importance of personnel “housekeeping” at a company looking to secure a DPA.[183] Von Dadelszen explained the necessity of “maintain[ing] the integrity of the DPA brand,” which “should not be watered down and given to companies run by those who are not truly good corporate citizens.”[184]

Ireland

On October 23, 2018, the Law Reform Commission (“LRC”) of Ireland published a report recommending that Ireland adopt a DPA regime largely resembling the U.K. DPA model.[185] Though the report is currently no more than a proposal, it invites the Irish legislature to pass a comprehensive statute to institute the recommended regime.[186]

The LRC’s recommendation draws largely on the U.K. DPA model; therefore, the proposed Irish DPA system would differ from the U.S. DPA framework in a number of key ways. For example, the LRC recommends that the Irish DPA regime be instituted by statute and be operated by the Office of the Director of Public Prosecutions (“DPP”).[187] The decision of whether to seek a DPA would remain entirely within the discretion of the DPP, but unlike DPAs in the United States, the DPP would have to obtain judicial approval in order to initiate the DPA process, to finalize a DPA, and to modify an existing DPA.[188] The DPP would need to present the terms of any proposed DPA to the High Court, which is an intermediate court that hears the most serious criminal and civil cases, as well as appeals from lower courts, for approval.[189] The LRC’s report outlines the test that the High Court would use when deciding whether to approve a DPA, recommending that the court ask whether the DPA is “in the interests of justice,” and whether its terms are “fair, reasonable, and proportionate.”[190] The LRC further recommends that the DPP only use DPAs if the company admits wrongdoing and the proposal requires that DPA terms be published, which is also distinct from DPAs in the United States.[191]

The LRC’s recommended DPA regime includes several features that would limit the availability of DPAs in Ireland. For example, the LRC recommends that DPAs only be made available to corporations and other unincorporated entities like partnerships, but not to individuals.[192] The LRC also recommends that DPAs only be made available in cases involving certain enumerated economic crimes, including conspiracy to defraud, theft, fraud, bribery, corruption, Companies Act and Competition Act offenses, revenue offenses, and market abuse offenses.[193] Both of these aspects of the Irish model also set it apart from the U.S. DPA system.

________________________________

APPENDIX: 2018 NPAs, DPAs, and Declinations with Disgorgement

The charts below summarize the agreements concluded in 2018. The complete text of each publicly available agreement is hyperlinked in the chart. If the agreement is not publicly available, the text of the DOJ press release is hyperlinked in the chart.

The figures for “Monetary Recoveries” may include amounts not strictly limited to an NPA, DPA, or declination with disgorgement, such as fines, penalties, forfeitures, and restitution requirements imposed by other regulators and enforcement agencies, as well as amounts from related settlement agreements, all of which may be part of a global resolution in connection with the agreement, paid by the named entity and/or subsidiaries. The term “Monitoring & Reporting” includes traditional compliance monitors, self-reporting arrangements, and other monitorship arrangements found in settlement agreements.

|

U.S. Non-Prosecution and Deferred Prosecution Agreements in 2018 |

||||||

| Company | Agency | Alleged Violation | Type | Monetary Recoveries | Monitoring & Reporting | Term of DPA/ NPA (months) |

| American Media, Inc. | S.D.N.Y. | Campaign Finance | NPA | N/A | Yes | 36 |

| Bank Lombard Odier & Co Ltd. | DOJ Tax | Swiss Bank Program | NPA Addendum | $5,300,000 | No | N/A |

| Basler Kantonalbank | DOJ Tax;

S.D. Fla. |

Tax Evasion; Fraud (Tax) | DPA | $60,400,000 | Yes | 36 |

| Central States Capital Markets, LLC | S.D.N.Y. | BSA | DPA | $400,000 | Yes | 24 |

| Credit Suisse (Hong Kong) Limited | DOJ Fraud; E.D.N.Y. | FCPA | NPA | $47,029,916 | Yes | 36 |

| Cultural Resource Analysts, Inc. | M.D. Tenn. |

Archaeological Resources Protection Act | DPA | $15,024 | No | Indefinite |

| Hallman Chevrolet | W.D. Pa. | Fraud (Bank Loan) | DPA | $2,137,000 | Yes | 48 |

| Health Management Associates, LLC | DOJ Fraud | Fraud (Health Care); FCA | NPA | $261,026,648 | Yes | 36 |

| HSBC Holdings plc | DOJ Fraud | Fraud (Wire Fraud) | DPA | $109,579,000 | Yes | 36 |

| Imagina Media Audiovisual SL | E.D.N.Y. | FCPA | NPA | $12,883,320 | Yes | 36 |

| Legg Mason, Inc. | E.D.N.Y. | FCPA | NPA | $64,242,000 | Yes | 36 |

| Mirelis Holding S.A. | DOJ Tax | Tax and Money-Transaction Violations | NPA | $10,245,000 | No[194] | 48 |

| Neue Privat Bank AG | DOJ Tax | Tax and Money-Transaction Violations | NPA | $5,000,000 | No[195] | 48 |

| Panasonic Avionics Corporation | DOJ Fraud | FCPA | DPA | $280,602,831 | Yes | 36 |

| Petróleo Brasileiro S.A. – Petrobras | DOJ Fraud; E.D. Va. | FCPA | NPA | $170,640,000 (U.S.) $853,200,000 (Brazil/U.S.) | Yes | 36 |

| Red Cedar Services, Inc. | S.D.N.Y. | RICO Act; Fraud (Wire Fraud); AML | NPA | $2,000,000 | No | 12 |

| Rite Aid Corporation | S.D. W. Va. |

Controlled Substances Act | NPA | $4,000,000 | No | 24 |

| Santee Financial Services, Inc. | S.D.N.Y. | RICO Act; Fraud (Wire Fraud); AML | NPA | $1,000,000 | No | 12 |

| Société Générale S.A. | DOJ Fraud; E.D.N.Y. | FCPA; Transmitting false commodities reports | DPA | $1,335,552,888 | Yes | 36 |

| Société Générale S.A. | S.D.N.Y. | Trading with the Enemy Act; Cuban Assets Control Regulations | DPA | $1,340,165,000 | Yes | 36 |

| Transport Logistics International, Inc. | DOJ Fraud; D. Md. |

FCPA | DPA | $2,000,000 | Yes | 36 |

| U.S. Bancorp | S.D.N.Y. | BSA | DPA | $613,000,000 | Yes | 24 |

| Waste Management Texas | S.D. Tex. | Immigration Violations | NPA | $5,527,091.55 | No | Indefinite |

| Wright State University | S.D. Ohio | Fraud (Visa) | NPA | $1,000,000 | Yes | 24 |

| Zürcher Kantonalbank | S.D.N.Y.; DOJ Tax | Tax Evasion; Fraud (Tax) | DPA | $98,533,560 | Yes | 36 |

|

FCPA Pilot Program Declination with Disgorgement Letters in 2018 |

||||||

| Company | Agency | Alleged Violation | Type | Monetary Recoveries | Monitoring & Reporting | Term of DPA/ NPA (months) |

| The Dun & Bradstreet Corporation | DOJ Fraud; D.N.J. | FCPA | Declination | $9,221,484 | No | N/A |

| Insurance Corporation of Barbados Limited | DOJ Fraud; E.D.N.Y. | FCPA | Declination | $93,940.19 | No | N/A |

| Polycom, Inc. | DOJ Fraud | FCPA | Declination | $36,611,410 | No | N/A |

[1] NPAs and DPAs are two kinds of voluntary, pre-trial agreements between a corporation and the government, most commonly DOJ. They are standard methods to resolve investigations into corporate criminal misconduct and are designed to avoid the severe consequences, both direct and collateral, that conviction would have on a company, its shareholders, and its employees. Though NPAs and DPAs differ procedurally—a DPA, unlike an NPA, is formally filed with a court along with charging documents—both usually require an admission of wrongdoing, payment of fines and penalties, cooperation with the government during the pendency of the agreement, and remedial efforts, such as enhancing compliance programs and—on occasion—a corporate monitorship. Although multiple agencies use NPAs and DPAs, since Gibson Dunn began tracking corporate NPAs and DPAs in 2000, we have identified approximately 509 agreements initiated by DOJ and 10 initiated by the SEC.

[2] We strive to provide the most up-to-date, accurate information; however, the government shutdown has affected the press functions of the federal government, limiting our access to agreements executed or announced in December 2018.

[2a] This amount may include amounts not strictly limited to an NPA or DPA, such as fines, penalties, forfeitures, and restitution requirements imposed by other regulators and enforcement agencies, as well as amounts from related settlement agreements, all of which may be part of a global resolution in connection with the agreement, paid by the named entity and/or subsidiaries.

[3] See Rod J. Rosenstein, Deputy Attorney General, U.S. Dep’t of Justice, Remarks at the American

[3] See Rod J. Rosenstein, Deputy Attorney General, U.S. Dep’t of Justice, Remarks at the American Conference Institute’s 35th International Conference on the Foreign Corrupt Practices Act (Nov. 29, 2018), https://www.justice.gov/opa/speech/deputy-attorney-general-rod-j-rosenstein-delivers-remarks-american-conference-institute-0 [hereinafter Rosenstein Speech].

[4] Memorandum from Sally Q. Yates, Deputy Attorney General, U.S. Dep’t of Justice, to Assistant Attorney General, Antitrust Division, et al., Individual Accountability for Corporate Wrongdoing (Sept. 9, 2015), https://www.justice.gov/archives/dag/file/769036/download.

[5] Rosenstein Speech, supra note 3.

[6] Id.

[7] Id.

[8] Id.

[9] U.S. Dep’t of Justice, Justice Manual, § 9-28 Principles of Federal Prosecution of Business Organizations, https://www.justice.gov/jm/jm-9-28000-principles-federal-prosecution-business-organizations.

[10] Rosenstein Speech, supra note 3.

[11] U.S. Sentencing Comm’n, Guidelines Manual, § 8C2.5(f), https://www.ussc.gov/sites/default/files/pdf/guidelines-manual/2018/GLMFull.pdf.

[12] Memorandum from Brian A. Benczkowski, Assistant Attorney General, U.S. Dep’t of Justice, to All Criminal Division Personnel, Selection of Monitors in Criminal Division Matters (Oct. 11, 2018), https://www.justice.gov/opa/speech/file/1100531/download [hereinafter Benczkowski Memorandum].

[13] Memorandum from Craig S. Morford, Acting Deputy Attorney General, U.S. Dep’t of Justice, to Heads of Department Components and United States Attorneys, Selection and Use of Monitors in Deferred Prosecution Agreements and Non-Prosecution Agreements with Corporations (Mar. 7, 2008), https://www.justice.gov/sites/default/files/dag/legacy/2008/03/20/morford-useofmonitorsmemo-03072008.pdf [hereinafter Morford Memorandum].

[14] See Brian A. Benczkowski, Assistant Attorney General, U.S. Dep’t of Justice, Remarks at NYU School of Law Program on Corporate Compliance and Enforcement Conference on Achieving Effective Compliance (Oct. 12, 2018), https://www.justice.gov/opa/speech/assistant-attorney-general-brian-benczkowski-delivers-remarks-nyu-school-law-program [hereinafter Benczkowski Speech].

[15] Id.

[16] Id.

[17] Morford Memorandum, supra note 13, see also Benczkowski Memorandum, supra note 12, at 2.

[18] Benczkowski Memorandum, supra note 12, at 2.

[19] See C. Ryan Barber, DOJ’s New Compliance Monitor Guidance Accounts for ‘Burdens’ on Companies, The National Law Journal (Oct. 12, 2018), https://www.law.com/nationallawjournal/2018/10/12/dojs-new-compliance-monitor-guidance-accounts-for-burdens-on-companies/.

[20] Deferred Prosecution Agreement, United States v. Panasonic Avionics Corp. (D.D.C. Apr. 30, 2018).

[21] Id.

[22] Id.

[23] Barber, supra note 19.

[24] Benczkowski Speech, supra note 14.

[25] See United States. v. MoneyGram International, Inc., 12-cr-00291 (M.D. Pa.), Dkt. 21 (extension from Nov. 8, 2017 to Feb. 6, 2018); Dkt. 23 (to Mar. 23, 2018); Dkt. 25 (to May 7, 2018); Dkt. 27 (to June 21, 2018); Dkt. 29 (to Sept. 18, 2018); Dkt. 31 (to Nov. 6, 2018); Dkt. 33 (to Nov. 9, 2018); Dkt. 34 (to May 10, 2021).

[26] Press Release, U.S. Dep’t of Justice, MoneyGram Int’l Inc. Agrees To Extend Deferred Prosecution Agreement, Forfeits $125 Million In Settlement With Justice Department And Federal Trade Commission (Nov. 9, 2018), https://www.justice.gov/usao-mdpa/pr/moneygram-international-inc-agrees-extend-deferred-prosecution-agreement-forfeits-125.

[27] Please see our 2012 Year-End Update for more details.

[28] Press Release, Standard Chartered, Extension of the U.S. Deferred Prosecution Agreements (July 27, 2018), https://www.sc.com/en/media/press-release/extension-of-the-u-s-deferred-prosecution-agreements/.

[29] Press Release, U.S. Dep’t of Justice, Standard Chartered Bank Agrees to Forfeit $227 Million for Illegal Transactions with Iran, Sudan, Libya, and Burma (Dec. 10, 2012), https://www.justice.gov/opa/pr/standard-chartered-bank-agrees-forfeit-227-million-illegal-transactions-iran-sudan-libya-and; Press Release, Standard Chartered, We Have Extended our Deferred Prosecution Agreements (Nov. 9, 2017), https://www.sc.com/en/media/press-release/we-have-extended-our-deferred-prosecution-agreements/.

[30] Deferred Prosecution Agreement, United States v. Standard Chartered, Case No. 11-cr-262, Dkt. 2 ¶ 4 (D.D.C. Dec. 10, 2012).

[31] Id.

[32] Press Release, Standard Chartered, Extension of the U.S. Deferred Prosecution Agreements (Dec. 22, 2018), https://www.sc.com/en/media/press-release/extension-of-the-us-deferred-prosecution-agreements/.

[33] Press Release, U.S. Dep’t of Justice, Michael Cohen Sentenced to 3 Years in Prison (Dec. 12, 2018), https://www.justice.gov/usao-sdny/pr/michael-cohen-sentenced-3-years-prison.

[34] Id.

[35] Id.

[36] Non-Prosecution Agreement, American Media, Inc. (Sept. 20, 2018), at 1.

[37] Id. at 2.

[38] Id.

[39] Id.

[40] Addendum to Non-Prosecution Agreement, Bank Lombard Odier & Co Ltd. (July 13, 2018), at 1 [hereinafter Bank Lombard Addendum].

[41] Id.

[42] U.S. Dep’t of Justice, Swiss Bank Program, available at https://www.justice.gov/tax/swiss-bank-program.

[43] Id.

[44] Id.

[45] Id.

[46] Bank Lombard Addendum, supra note 40, at 1.

[47] Press Release, U.S. Dep’t of Justice, Justice Department Announces Addendum to Swiss Bank Program Category 2 Non-Prosecution Agreement, Bank Lombard Odier & Co Ltd. (July 31, 2018), https://www.justice.gov/opa/pr/justice-department-announces-addendum-swiss-bank-program-category-2-non-prosecution-agreement.

[48] Bank Lombard Addendum, supra note 40, at 1.

[49] Id.

[50] Id.

[51] Deferred Prosecution Agreement, United States v. Basler Kantonalbank, No. 18-CR-60228-Bloom (Aug. 29, 2018) [hereinafter BKB DPA].

[52] Press Release, U.S. Dep’t of Justice, Justice Department Announces Deferred Prosecution Agreement With Basler Kantonalbank (Aug. 28, 2018), https://www.justice.gov/opa/pr/justice-department-announces-deferred-prosecution-agreement-basler-kantonalbank [hereinafter BKB Press Release].

[53] BKB DPA, supra note 51, at 29.

[54] Id. at 16–17.

[55] BKB Press Release, supra note 52.

[56] BKB DPA, supra note 51, at 10.

[57] Deferred Prosecution Agreement, Central States Capital Markets, LLC (Dec. 10, 2018), at 1 [hereinafter CSCM DPA].

[58] Id. at 1–2.

[59] Press Release, U.S. Dep’t of Justice, Manhattan U.S. Attorney Announces Bank Secrecy Act Charges Against Kansas Broker Dealer (Dec. 19, 2018), https://www.justice.gov/usao-sdny/pr/manhattan-us-attorney-announces-bank-secrecy-act-charges-against-kansas-broker-dealer [hereinafter CSCM Press Release].

[60] CSCM DPA, supra note 57, at 2-3.

[61] Id. at 6.

[62] Id. at 3.

[63] CSCM Press Release, supra note 59.

[64] Id.

[65] Press Release, U.S. Dep’t of Justice, Auto Dealership Agrees to Pay Penalty of $1.4 Million and Restitution of More than $730K in Bank Loan Fraud Scheme (Aug. 31, 2018), https://www.justice.gov/usao-wdpa/pr/auto-dealership-agrees-pay-penalty-14-million-and-restitution-more-730k-bank-loan-fraud.

[66] Id.

[67] Id.

[68] Press Release, U.S. Dep’t of Justice, Hospital Chain Will Pay Over $260 Million to Resolve False Billing and Kickback Allegations; One Subsidiary Agrees to Please Guilty (Sept. 25, 2018), https://www.justice.gov/opa/pr/hospital-chain-will-pay-over-260-million-resolve-false-billing-and-kickback-allegations-one [hereinafter HMA Press Release].

[69] Id.

[70] Non-Prosecution Agreement, Health Management Associates, LLC (Sept. 21, 2018), at 1 [hereinafter HMA NPA].

[71] Id.

[72] Id. at 1–2.

[73] Id. at 4.

[74] Id.

[75] Id. at 2.